Thankful for Endless Cards News - CardsFTW #10

Good Cards, Bad Cards, Corn Cards, Cavs Cards

Every week when I finish writing this newsletter, I think to myself: "What if nothing happens worth covering next week?" So far, this is not a problem; there is an endless stream of news about cards. Let's dive into what happened over the past two weeks.

Bad Cards (Or Perhaps OK Cards?)

In Issue #9, I mentioned UK-based Lanistar, a company building a hybrid of Curve and Dynamics card functionality. Since their announcement and related marketing, the U.K. Financial Conduct Authority, which regulates financial services in the country, issued a warning that Lanistar appeared to be offering services without authorization. In a surprise turnaround a few days later, the FCA revoked its notice as the company is in pre-launch and agreed to add specific disclaimers to its site.

Financial services startups are hard. You want to share what you're building and build buzz, but at the same time, you need to follow the law. (OK, maybe hard is the wrong word here.) Many waitlists and other promises from startups don't turn out to be accurate, and the protections aren't what they seem. For example, many startups point to FDIC insurance to give users confidence. FDIC insurance covers a bank failure, not the failure of a startup that works with a bank.

Startups like Lanistar frustrate me because they make consumers cautious of other emerging companies, even when we're playing by the rules. You can usually tell whether a company has been through compliance or partnered with a bank by looking at the footer of their website. If they had a regulator or regulated partner, there will be license information or a statement about the bank partner. Consumers and investors should continue to be wary of a startup's claims and dig in on the compliance side, even though it is not as much fun.

Instant Cards

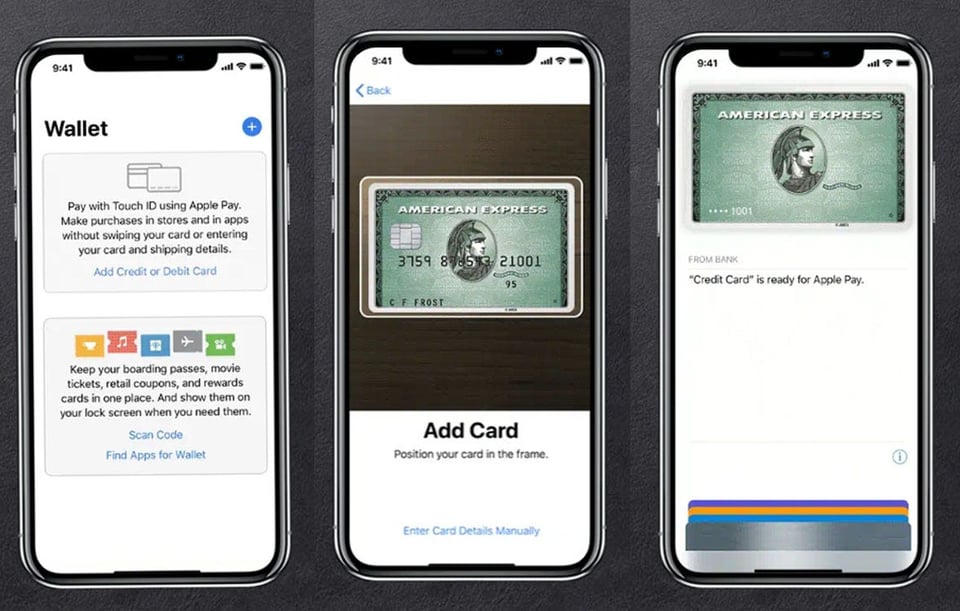

One of the best features of Apple Pay and Google Pay is the ability to provision a virtual card directly into the mobile wallet. The traditional credit card process requires a user to apply for a card, receive approval (which itself can take a few days), and then wait for a card to be personalized and mailed to them (usually another 7-10 days). In the past, some issuers, like American Express and Comenity, made it possible for users to receive their account numbers over the web. Sharing the account number before the card arrives enables users to enter that card number into a form and immediately pay for purchases. American Express announced that it can now instant provision a new credit card directly into a digital wallet upon approval. Apple's card, issued by Goldman Sachs, debuted with this powerful feature, and it is exciting to see it come to additional issuers. Enabling real-time applications, approvals, and provisioning will create new capabilities for commerce.

Cards, No Cash

Sponsorship of athletics by credit card companies has long been a huge area of marketing investment. Visa is taking it a step further, working with the National Football League to make the Super Bowl cashless. Going cashless requires Visa to host a reverse ATM that will turn cash into prepaid cards, as you must have a card to buy anything at the stadium. I'm skeptical that a Super Bowl will happen at all this year, but this is a bold move. Cashless environments present certain risks, mainly the exclusion of the financially underserved, but let's be honest, the Super Bowl is a rich person's event anyway, so this really only restricts millionaires from rolling out their wad of cash to show off.

Cavs Cards

Speaking of athletics and credit cards, Silicon Valley startup Cardless announced a new round of funding and that they would be launching their first product with the Cleveland Cavaliers. Most athletic leagues have existing partnerships (MLB is with Bank of America, NFL with Barclaycard, NHL with Discover), but the NBA does not, creating an interesting opening here. These sports cards do not have a reputation for strong financial performance, due to both the demographics of the users attracted to the cards and the high licensing cost. That said, I love affinity-based products, and this could be a strong draw for Cavs fanatics.

Corn Cards

The most enjoyable news of the week might be the announcement that UBS will launch a card made from corn. There have been many attempts to make credit cards more environmentally friendly, such as making cards from recycled plastic (this has been very hard to do) and even wood. The UBS Optimus Foundation Eco Credit Card will also donate a portion of revenues to various good causes.

Cash Cards

Several studies recently highlighted the pandemic focus on cashback for card rewards. The Futurist Group notes in their Designing a Successful Cash Back Card report: "Since March of 2020, more than 20 new credit card offers have been launched in the U.S. In the same time frame, more than 50% of established cashback offers underwent modular changes to their value propositions (i.e., rewards and benefits)." While I can't afford the report, I was able to find a screenshot that showed the top five cards:

- U.S. Bank Cash+ Visa

- Chase Freedom Unlimited

- Amazon Rewards Visa

- Capital One Quicksilver

- Citi Double Cash Card

I was surprised to see that U.S. Bank Card in the number one position. It's a bit of a lesser-known product from a bank that doesn't do as much advertising outside its home area. That made me a bit suspicious of all the results; in the past decade of marketing cards, this U.S. Bank Card doesn't typically come out of the top (more due to awareness than product features).

This focus on cashback aligns with PYMNTS and Novae's study that showed 45-48% of consumers prefer a form of cashback to points (38%). This same report highlighted that approximately one-third of consumers are open to switching financial institutions for rewards and that 40% of cardholders feel like they are not offered enough reward options. The study reinforces that there is a lot of room for growth and innovation.

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you're looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.