Card Trends in 2021 - CardsFTW #13

Here's to brighter days

Well, 2021 is here and so far, it isn’t much different than 2020. We continue to trudge along through the fog of the pandemic. There are glimmers of light on the horizon, but I think it will be well into the second half of the year before any sense of normalcy returns.

I finished out the past couple of weeks with an attempt (not fully successful) to disconnect and refresh. I did pile a few of the 2020 trends into my personal list: I made sourdough bread and deep dish pizza from scratch, and we added a new dog to the family (replacing our beloved old one who passed this summer).

Cards news continues to come at a high pace and I am looking forward to all of the news to come.

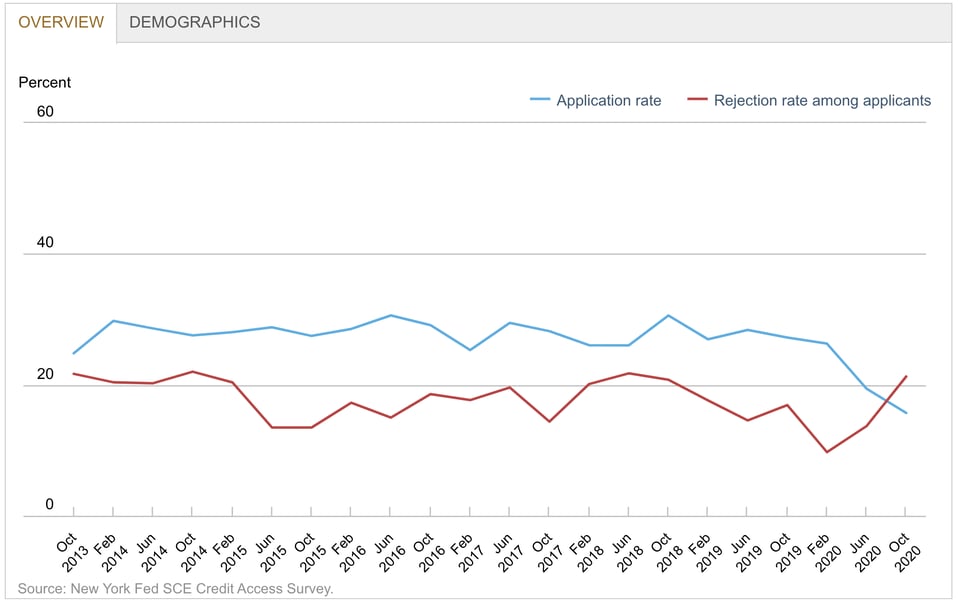

At the end of 2020, the Federal Reserve Bank of New York reported in their SCE Credit Access Survey that the percentage of households applying for a new credit card in the past 12 months dropped to 15.7% in October 2020, from 27.2% a year prior (a 43% decrease). At the same time, the rejection rate rose 26% from 16.9% to 21.3%. For further context, survey data starts in 2013 and the last time the rejection rate was this high was October 2014. The application rate has never been that low.

Not a great time to launch a challenger credit card company, I suppose (they say timing is everything!).

This is the bottom, though. Consumers will continue to seek credit and credit cards continue to be popular and convenient. There is pressure both from a challenging economy and the rise of buy now/pay later options, but credit cards are the main transactional tool of many Americans.

Travel & Cards

I’ve discussed a number of times in this newsletter that travel rewards have been less meaningful in 2020. That’s been true and I continue to believe very strongly that consumers will demand non-travel rewards options. However, there is pent up demand for travel from the forced isolation of the pandemic.

Major travel cards have been increasing signup bonuses over the past few months as banks have seen manageable losses on their portfolios and a decline in applications. New cards continue to be launched. The final new card announcement of the year that stood out to me was again travel-related ,with Chase and Air Canada announcing a new Air Canada Mastercard to be issued in late 2021.

This one surprised me and my whole extended family is Canadian!

Air Canada has long had a dominant (though shrinking) position in Canadian air travel and their Aeroplan rewards scheme was ubiquitous. Air Canada then separated from Aeroplan and created a new rewards program. It’s confusing as we Americans haven’t seen a major airline here separate from its loyalty program, but this new program is like American Airlines spinning out AAdvantage and then, years later, announcing that AAdvantage isn’t the way to earn or spend miles on American anymore.

Although Air Canada is large in Canada, it seemed small for Chase here. On digging in a bit further, the new Air Canada loyalty program includes transferable miles which enable consumers to earn on one airline or card and then use those points elsewhere. These transferable miles are one of the hallmarks of the complex but lucrative (if you can stand the work) rewards program here in the United States. Chase is a huge player in this game with their flagship Ultimate Rewards program which had transferable points. The extreme travel crowd may well go in big on this card if the numbers are right and points can transfer. With signup bonuses, credit card gaming, and manufactured spend, cardholders may be able to redeem points for a flight to somewhere other than Canada, without ever taking an Air Canada flight, but by acquiring the Air Canada card. If you want to know more, I am sure dozens of travel blogs will explain soon.

Speaking of big moves for 2021 from Chase, news came out on December 28th that Chase is acquiring cxLoyalty, a major backend provider of the credit cards rewards business. Chase used to work with cxLoyalty and switched to working with Expedia for travel booking. I assume they will be switching back. CxLoyalty serves other major banks like Citibank and Capital One. To what extent those banks are now looking for new providers is unclear, but I have to imagine that they loath Chase owning the platform they use. This is a huge bet on travel and another sign that the banks are lining up their strategies to accommodate an explosion in travel in the post-pandemic era.

Cards for Lending

Cards for travel are positioned as rewards and loyalty products, not as revolving loans, but many consumers still use credit cards. Last year saw updates on the product line at Petal, the launch of TomoCard, and of Chime’s credit builder product. We also finally got details at the end of the year about SoFi’s new credit card, which is a loan product by targeting, but offers up to 2% cash back (when you use rewards to fund an account or pay down a loan at SoFi).

While some have done well (or at least OK) during the pandemic, many millions have suffered economically. Those consumers will need access to credit following bankruptcy, foreclosure, and evictions. Options after the last financial crisis were poor, but the rise of fintech options have led to more friendly and fair revolving credit options today. We are going to see more new options and see what fintech lenders are wiped out when a once in a century pandemic hits their untested lending algorithms.

A different way to think about cash back

Traditionally, cards have earned 1% cash back or sometimes an accelerator like 2, 3 or even 5% in certain categories. Over the past decade this base-level earning was paired with card-linked offers, which are like coupons at certain merchants, offering anywhere from 5-15% cashback. Several providers like Petal in the US or Neo in Canada have positioned card-linked offers as the cashback. This new take on marketing emphasizes the higher ultimate earnings potential against traditional offerings. It sounds good, although I am skeptical that it’s a better deal for the consumer. New providers, like Fidel from the UK, make building card-linked offers easier and Google’s new Pay app includes Fidel functionality. Card-linked offers already suffer from being available in overlapping ways (there are only so many underlying providers of the merchant offers like Cardlytics or Dosh) and I think this will add to consumer confusion. People do love a good deal, though.

Staged Wallets Come to the US

In 2012 I founded my last startup, Wallaby, which aimed to build a smart digital wallet in the cloud that was accessed via a physical card product. Now called a staged or over the top wallet, the idea was you could carry a single piece of plastic, swipe and have the transaction routed to the underlying card of your choice. It was a really good idea, but we couldn’t make it work, as the major networks shut us out. A number of startups raised (and spent) more than $100MM building physical versions of one card to rule them all.

In the UK, startup Curve built this product and, thanks to the EU open banking rules, was able to make it come to life. Curve started a US waitlist earlier this year and, as an end of year tease, shared that they expect to ship Curve cards by May. While I wish that card had a different logo on it, I’m excited to see this come to life. I think this may finally be the year.

Lots of New Cards

Finally, I think 2021 will see the launch of a number of new credit cards. We’ve mentioned many card startups like Sequin, Paceline, Tiv, X1, Klutch, and others. None of these cards launched in 2020, but they are working hard towards a new product in 2021. They won’t all be able to raise the right funding, find the right partners, and launch, but some of them will. I’m excited for each of them. We shouldn’t just leave the credit card game to the current issuers and 2021 will be a great year for experimentation and innovation.

Cheers!

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.