Installments Everywhere - CardsFTW #32

Plus, The Real L Walker, Credit Building, DDA Conversions, and Bitcoin Cards

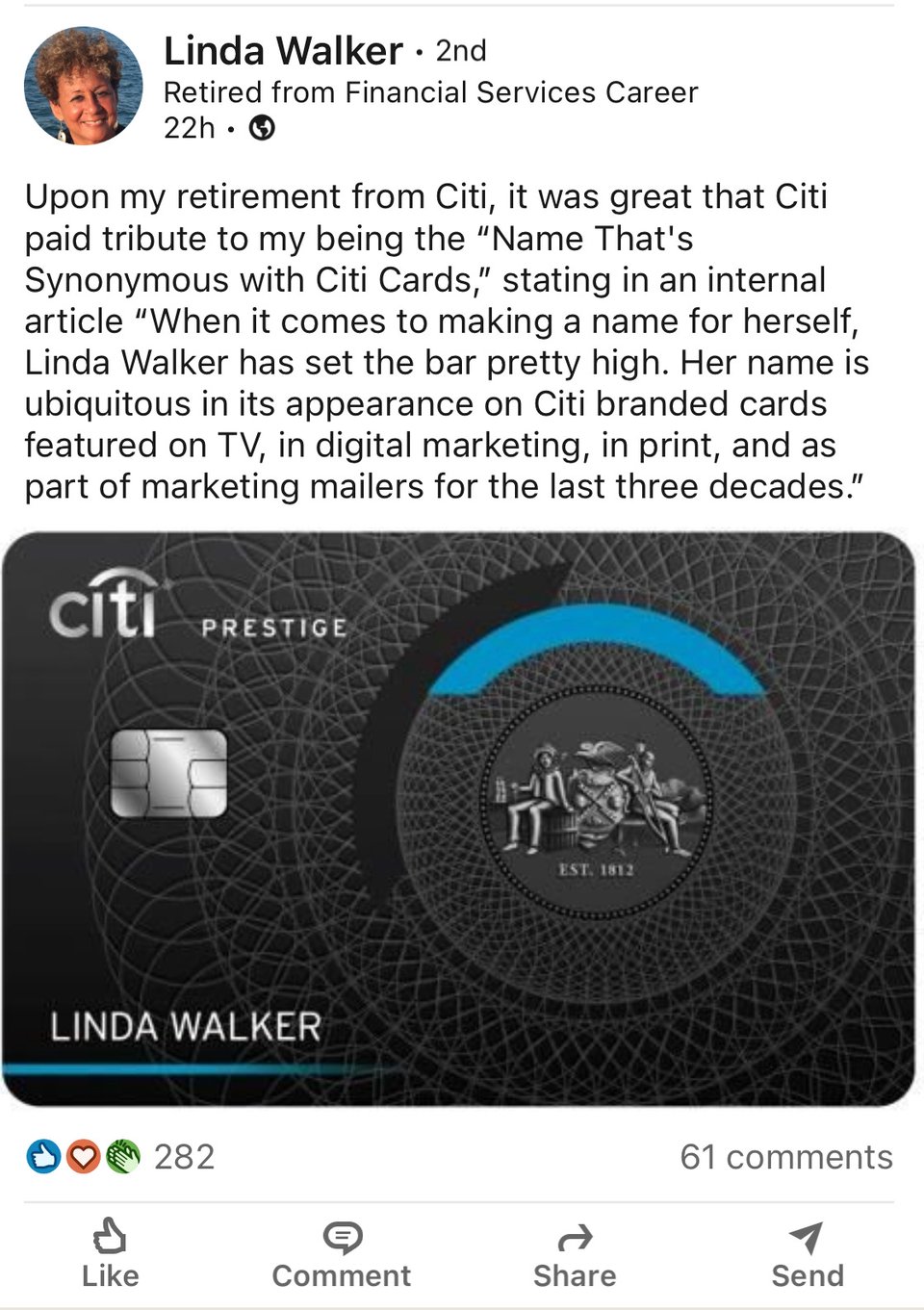

Enjoy Retirement, Linda Walker

Long-time readers will know I love thinking about the sample name on card marketing. For the past three decades, Citibank has used “Linda Walker” for all of its cards. In what is the most interesting thing I have learned from LinkedIn: Linda Walker is a real person.

Linda Walker retired from her role as head of Global AML Policy at Citi earlier this year. Previously, Linda was an associate general counsel for cards from 1989 to 1997 at Citi. Congratulations, Linda!

Installments Everywhere

The reopening of the economy continues to provide opportunities to accelerate recent innovations in everyday consumer financial products. I’ve discussed several times the overlapping nature of revolving consumer credit cards and buy now/pay later products like Klarna, Affirm, and Afterpay. Now, Visa Canada is launching an installment option that builds buy now/pay later into every consumer credit card in the country.

Consumers want to pay for some products right now, and they want to finance others. When credit cards were first introduced, they operated both as a method of payment when you didn’t have cash on hand and as a method of financing. That hasn’t changed. What we’ve seen is an additional layer of granularity on cards with BNPL later schemes like Chase Blueprint or Amex Pay it Plan it. These products and the introduction of Visa Canada’s BNPL products (and many others from many other credit card issuers) enable consumers to select on a transaction-by-transaction basis whether to pay now or pay later.

Consumers have also self-selected this behavior by trading between a debit card (pay today) and a credit card (pay later). The advantage of the new BNPL schemes is a clear pay-down schedule and clarity of cost (whether 0% like some merchant-funded Affirm programs or just a fixed fee). The scary part of credit cards for most consumers is the compounding interest and how small everyday purchases add to this.

In the past, issuers have attempted other ways to bring debit and credit together, such as the Fifth Third Duo Card (no longer available), which used your checking account with a PIN debit entry or your credit line with a signature swipe. We also had products like Dynamics’ powered physical card, which could swap card numbers on the magstripe by pushing a button (say between debit/credit or multiple credit accounts).

The all-in-one card idea continues from issuers, like Hong Kong’s Mox which just launched a combined card you switch via an app. We’ve seen the rise and fall of other hardware solutions like Coin, Fuze, and Stratos. UK customers can use Curve to swap accounts on a single plastic as well.

Ultimately, the after-the-fact capabilities of BNPL on a credit line are a very easy way to manage this without fancy cards or fumbling with apps at the point of sale. I predict most cards will carry an installment capability within the next 12 months, and the simplicity of a purchase-by-purchase conversion to a fixed repayment will win out.

Bakkt Debit Card

Bakkt is a bitcoin and loyalty app that is backed by major financial player Intercontinental Exchange. Users can manage various real and digital currencies via the Bakkt app. Now they can easily spend bitcoin and cash via a new virtual debit card offering. There is an explosion in debit cards that access bitcoin balances, which go along with traditional brokerages’ cash access debit cards. The primary value here is quicker access (sell an asset, spend on card vs. having to transfer via ACH to your core debit account). We’re going to see every consumer cryptocurrency provider have to provide a debit card for access as a standard type of requirement.

A New Credit Builder

Credit Sesame, which provides access to free credit scores and offers a credit card marketplace, expanded its direct offerings from a debit card to include a credit builder service. Like rival Credit Karma, these services need customers with good enough credit to get approved by traditional bank issuers to make money. Both companies have expanded into cash accounts, which they can do without competing with their biggest revenue sources.

Credit Sesame claims this new product is a unique way of building credit with a debit card, but frankly, I don’t understand it. The product description reminds me of SelfLender, which allows people to make a cash deposit into an account and use that deposit to establish a secured account reported to the credit bureaus.

To quote Credit Sesame:

“We’ll tally up some of your monthly debit purchases and report them to the bureaus as on-time payments to keep building your credit history!”

Credit Sesame even says they will pay you when you increase your score.

I’m surprised this is allowed by the bureaus. Lending yourself money doesn’t establish your ability to repay a creditor. I suppose you can game the system and raise your score, but does it really help people to manage their credit better? Will it make them more appropriate for other products?

O.G. Neobank Card Upgrades

I started in fintech in 2006 as a product manager at Green Dot. I was fortunate to work on a major product launch of the Walmart MoneyCard, a Visa prepaid card. This co-branded reloadable debit card allowed Walmart to offer banking-like services to unbanked and low credit consumers through a retail package. You could walk into any Walmart, many open 24/7, and acquire a Visa card at the register by handing over a cash deposit and a small fee. Consumers with the card could depend on security for their money and the ability to shop online, with no credit check required.

The Walmart MoneyCard program has continued to grow over the years and remains an essential product for Green Dot and Walmart. While it sounds like a technical designation, it is interesting news to see that Green Dot has changed the MoneyCard program for a reloadable prepaid debit card product to a demand deposit account.

According to the companies, this will allow the companies to reduce the monthly spend requirement to waive the fee (to $500) and provide overdraft services (as well as other unnamed benefits).

The fee reduction sounds good, but why is Walmart getting into overdrafts? There is a $15 overdraft fee. At the same time, competitors like Chime and even more traditional banks like Ally are operating in a no overdraft environment. I find it odd to introduce this feature. One of the top reasons consumers liked the original MoneyCard was that it had very clear fees (simply purchase, monthly, and out-of-network ATM) and no penalty fees like overdrafts. When you were out of money, your card would not work, but you would not be charged. An overdraft fee is the opposite of the approach we had those many years ago.

Walmart's merchandising and brand power is not to be ignored, but the new features are a bug. As the latest generation of neobank debit card providers create increasingly consumer-friendly options, products cannot afford to move backwards into fee-driven territory.

If anyone knows the value of the DDA conversion, please let me know, and I’ll share it with everyone. I, for one, am lost on the shift.

Quick Notes

A few quick notes on the way out:

- Cardless announced a Florida Marlins card

- The Financial Times put together a great article on credit card lending recovery

- BlockFi launched their long-anticipated bitcoin credit card

- Neobank Oxygen launched a complicated, tiered rewards program.

CardsFTW

Thanks for reading CardsFTW, a weekly-ish newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.