More Challenger Cards - CardsFTW #45

Plus, rewards for electricity

Challenger Cards Grow in Number and Size

Over the past two years, the number of credit card products launched by startups or tech companies has grown dramatically. Four years ago, only a handful of challenger cards were in the market. Today, new cards are being launched or announced every few weeks. In addition, several of the challenger cards are really taking off, such as:

When you look at the common aspects of these products, two things stand out to me: First, many cards target consumers with low scores or thin files. Second, many feature bitcoin or crypto rewards.

There is always a huge demand for new products for people whose applications are denied by other card issuers. Last week Avant announced they had surpassed 1 million cardholders.

Crypto people love crypto: 1.5% cashback is just 1.5%, except when it’s 1.5% in crypto. Then, 1.5% feels like a lot more to a group of users. On Friday, BlockFi shared that they had paid out more than 315 bitcoins worth of rewards on their card, which rough math and cost averaging would say is well more than 1 billion in total payment volume on the card.

Hot on the heels of these cards are many more announcements or new cards. Will we see net new innovations or more of the same?

Prosper, a personal loans provider, follows fellow lenders Upgrade and SoFi in introducing a Prosper Card. The new card competes in the low credit and no credit space, with Prosper choosing to stack up against Capital One Platinum and Merrick Bank’s secured card. The Prosper card is not secured and includes no ATM cash withdrawal fees, rare in this space. The card does carry a $39 annual fee (waived for the first year with auto payment) and a very high 23.99% minimum APR. The ATM cash withdrawal won’t have a fee, but you will pay 29.99% for those cash advances (with no grace period, of course). This fintech card is issued by Coastal Community Bank, an emerging player in the credit card sponsorship space.

Meanwhile, on the other end of the spectrum, neobank Point announced its upcoming launch of a charge card: PointCard Titan. The card will carry a $399 annual fee and promises premium rewards. American Express cards are charge cards, and most consumers aren’t paying attention to the difference between charge and credit. (Charge cards do not allow for consumers to carry balances.) Charge cards had largely fallen by the wayside. The focus on the Platinum Card-like “no spending limit” marketing line is an interesting take.

Consumers will be able to select accelerated rewards categories. Cardholders choose two 5x categories (rideshare, food delivery, subscriptions, fitness, or EV charging) and two 3x categories (travel, dining, groceries, entertainment, or fashion). They will earn also earn 1x everywhere else.

Urban millennials’ hearts be still. At least we know whom Point is targeting.

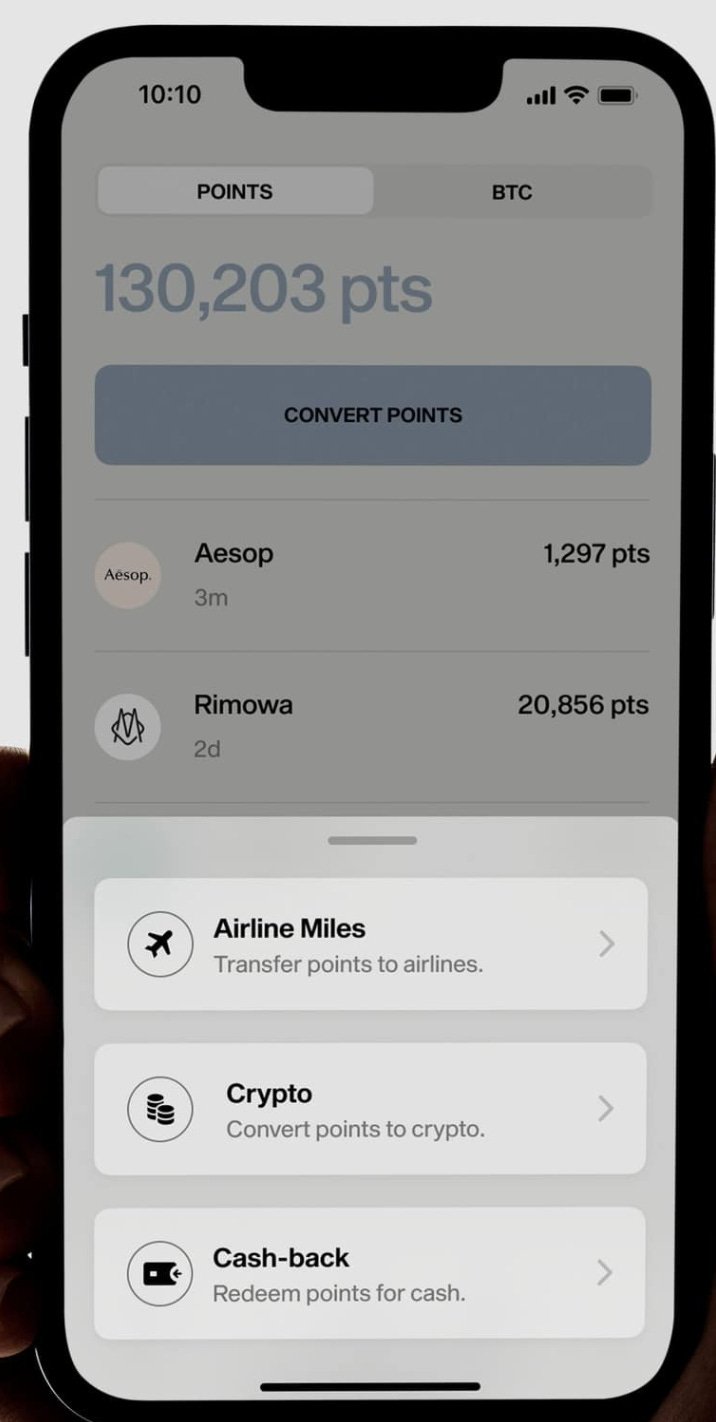

The exact value of points transfers is unclear, although points are pegged at one cent in value. The card will include transferable points to airlines in each of the major alliances (SkyTeam, Oneworld, and Star Alliance), plus JetBlue, Lufthansa, and others. You will also be able to choose cashback or crypto rewards.

👆I don’t agree with this, though: “cash-back”? It’s clearly either cashback or “cash back.”

Other features include a metal card, virtual cards, etc. Point’s existing debit card product is issued by Column, N.A., the tech-focused rebrand and reboot of Northern California National Bank in Chico, CA. It’s unclear if Point’s credit product will be issued by the same.

The card is aimed right at Chase Sapphire Reserve consumers, and all-in looks compelling when considered against similar travel cards. Get on the waitlist here. (or is wait-list? 😜)

EVs: The New Gas

Meanwhile, traditional issuers continue to improve on their products. U.S. Bank launched their new Altitude Connect Visa Signature credit card. The product has a $95 annual fee (waived the first year) and offers 5x points on hotel and rental cars booked through U.S. Bank, 4x points on travel, gas, and EV charging, plus 2x points at grocery, dining, and streaming, with 1x everywhere else. Those are strong rewards. I usually discount the higher bonuses for booking with the card company, but 4x travel and 2x grocery and dining at $95 per year is a good offer. A $30 annual streaming offset credit reduces the annual fee to an effective $65. Points are worth 1 cent each.

I haven’t seen electronic vehicle charging as a bonus category until this week, with the upcoming PointCard Titan and this US Bank card offering it. Now that I have an EV, I’ll have to rethink my strategy (not really, I seem to mostly charge at home).

CardsFTW

Thanks for reading CardsFTW, a weekly-ish newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Chief Product Officer at Apto Payments. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.