Card-Linked Offers - CardsFTW #5

Neobanks for everybody, CardCon Discount, and more

This week, we welcome our first guest column from my friend and former colleague Maria Schriber. Maria was an early employee at Wallaby leading our community and credit card data management. Today, Maria is a Member Experience Manager at PayPal’s Honey. We’re excited to share Maria’s take on the week in credit cards.

Card-Linked Offers: A replacement for loyalty cards?

With the country moving closer to a cashless economy and credit cards competing for your business, card-linked offers (CLOs) are both booming and evolving. Originally touted as a way to bridge the gap between online marketing and in-store sales, CLOs can clinch the deal on something you’re already buying. They might even push you into splurging on something you didn’t know you needed. You want those special-edition Madewell jeans? Select Chase cardholders can earn $25 back on their $100 purchase. Add the offer to your card, use that card to pay, and boom: You’ll receive a statement credit back to your card! It feels like you’re somehow beating the system, even if the system is enticing you to make the purchase in the first place.

CLOs aren’t going anywhere anytime soon. They’ve been wildly successful for brands and consumers alike. According to this 2018 Cardlinx survey, 62% of brands that use CLOs saw transaction volume more than double over the past year. Restaurants, grocery stores, and department stores were once the top players of these CLOs, but now beauty services, eyeglasses, meal delivery kits, and even travel are included. If you have to book a hotel room this holiday season, you’ll see myriad offers at merchant partners like Hilton, DoubleTree, Intercontinental, and the like.

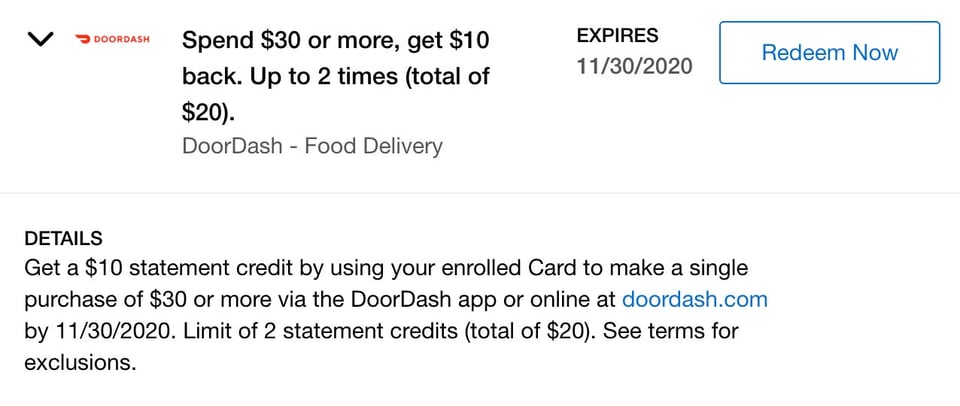

In the age of the pandemic, we’ve also seen an increasing focus on getting CLO deals to shoppers who aren’t stepping into a physical store or restaurant. Just the other day, I checked my Amex Offers - which I recommend you do for all your credit cards at a regular cadence to see what deals circulate - and found an offer from DoorDash that was a no-brainer. This offer required a minimum of $30 spend at DoorDash to get $10 off. It could be redeemed twice for two $10 statement credits.

I like to eat good food (loosely defined – sometimes you need the comfort of late night Taco Bell), so it wasn’t hard to hit these thresholds and get $20 back in just a couple weekends. I was more than happy to take the 33% discount by swapping out my card of choice for two transactions.

Even if it’s not exactly “free” money, it feels good to know you scored a deal or a discount. It’s a win-win for all involved: consumers save a little cash and merchants do not have to pay for advertising impressions, print mailers, or coupons. They only pay a small fee each time someone makes a purchase.

CLOs have come a long way since the 1990s when credit card companies began to experiment with integrating rewards and loyalty into their consumer cards. CLO targeting still has room to grow in the areas of accuracy and real-time rewards. I often get offers for Gayle’s Chocolates and Teleflora, scrolling over them without interest. However, in the few years I’ve actively checked my offers, I noticed a dramatic improvement on ones that pique my interest. Using the increasing accuracy of data science, CLOs continue to improve with targeted detail. Also, instead of having to wait for rewards to accrue on a rolling or monthly basis, the instant gratification received from real-time offers is an awesome feature. As predictive modeling expands and more consumer insight is gleaned, CLOs will only get better and will benefit all participants in this ecosystem: consumers, banks, and retailers.

Retailers traditionally have large promotional budgets, and this is data-drive new avenue for exploring ways to drive customer engagement. Financial institutions benefit from cardholder engagement and can take delivering value to cardholders. It’s unclear if the revenue for banks is meaningful, but the additional logins and cross-marketing opportunities are meaningful.

Some cards, such as last week’s featured Petal Cards, are using card-linked offers in their marketing as replacement for traditional rewards. The ability to tout cashback up to 10% is a meaningful marketing hook. More analysis on card-linked offers to come in future issues.

Killer Mike’s Killer Waitlist

Michael Santiago Render, better known as Killer Mike, announced he, along with several business partners, announced the launch of neobank Greenwood which is for “Black and Latinx communities and anyone else who wants to support Black-owned businesses.” Celebrity launches can drive consumer adoption tremendously (as we noted last week with Step’s TikTok influencer approach) and Greenwood reported more than 100,000 members on its waitlist in the first week.

There are a growing number of neobanks focused on specific consumer groups such as other people of color, the LGBTQ community, and more. Mocafi, a 5-year-old neobank has an impressive product feature set aimed at underserved Black Americans, including credit monitoring and reporting rent payments to bureaus. Being a great neobank is going to require more than a replacement checking/demand deposit account.

Neobanks, and prepaid cards before them, have long served the financially underserved and this added focus should continue to help bring the underbanked into more mainstream products.

A plastic that isn’t plastic

That piece of plastic in your wallet that is the subject of this newsletter wasn’t always plastic. The original cards for Diners Club were paper. Over the years, PVC became the dominant materials for cards. Luxury cards have moved into metal cores and coatings, from steel to gold. Recent years have seen significant investment in more environmentally friendly plastics cards, which are a challenge due to the requirements for durability, stiffness, etc. Ecosia, a European search engine with an environmental focus, announced its partnership with TreeCard. The TreeCard is powered by Synapse and promises a 100% wooden (Cherry) card. Join the waitlist (and get a tree planted for doing so) via my referral link.

The best of times, the worst of times

I don’t think anyone would vote for 2020 as the best of times and unemployment remains stubbornly high. Yet, as bank earnings came in, banks reported feeling comfortable with overall loan loss provisions and with rising income from card payments. In a related trend, FICO reported that American FICO scores are at an all-time high. The Wall Street Journal spoke with a number of consumers that used the shock of COVID-19 and the government stimulus checks to pay down debt and improve their financial situation, which helped lead to higher scores. Scores are sensitive to credit utilization, so a decrease in debt can have a significant positive impact.

Beyond the continued pressure, and lack of stimulus, that might rapidly turn around the economic situation, banks are considering closing unused lines or reducing overall credit availability to further trim risk. Most consumers are unaware that a bank can and will unilaterally reduce open-to-buy credit lines on payment cards. With limited employment prospects, this could further reduce consumer flexibility.

CardConExpo 2020

CardConExpo is a small conference dedicated to credit cards and credit card media run by Jason Steele, a longtime credit card journalist, now Director of Credit Card Content for Money.com. The all-virtual 2020 edition is a few hours daily November 16-19th and is a must-attend for everyone interested in credit cards, affiliate marketing, and consumer credit.

I will be on a panel on Thursday, November 19th focusing on startups in the credit card space, along with moderator Melissa Long of MaxRewards and two other entrepreneurs: Kristy Kim, CEO of TomoCredit and Vrinda Gupta, CEO of Sequin Card.

CardsFTW readers get a 25% discount with the code “Goldman2020” Register via Eventbrite.

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder and CEO at Vertical Finance, a challenger credit card startup. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman