Imprint’s new HEB Card - CardsFTW #56

Plus, Apple’s savings account and peer-to-peer payments

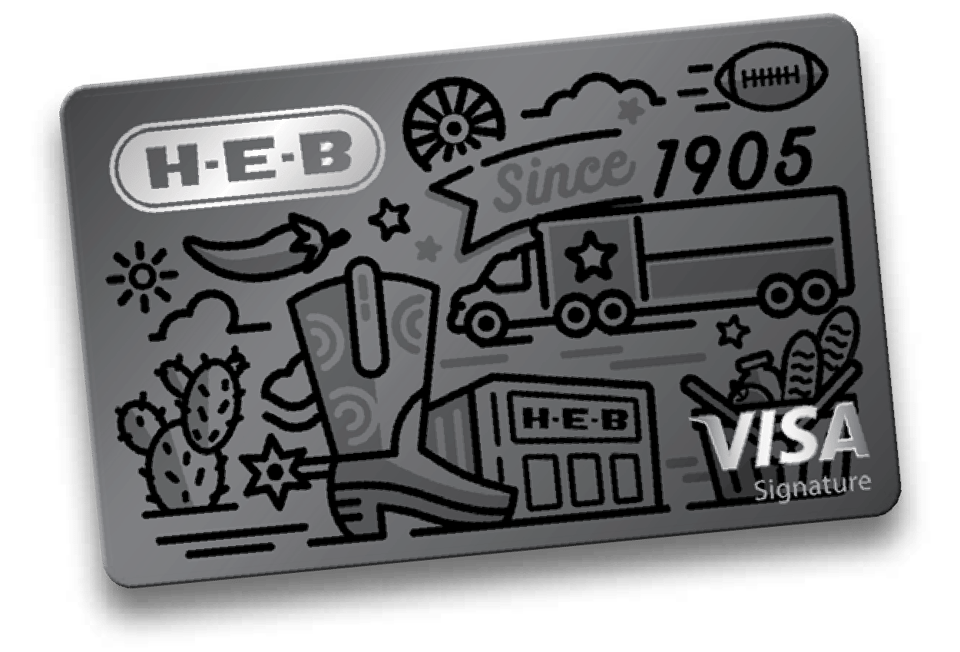

H-E-B Visa Cards Debut

H-E-B, a 340-store supermarket retailer based in San Antonio, announced their new Visa card products last week. The details of the credit card offers are:

5% cash back on eligible H-E-B brand products at H-E-B Sites

1.5% cash back everywhere else

No annual fee

A limited-edition metal card (for the first 20,000 applicants)

Standard Visa Signature benefits

I would not pass up the opportunity to write “Howard E. Butts” on this card

This card reads like a competitive checklist with other brands. There are a lot of 1.5% cashback cards out there (Chase Freedom Flex, Capital One Quicksilver, Discover, etc.) and 5% cards (Chase Freedom Unlimited, Discover). The combination 5% / 1.5% is more rewarding, but the card doesn’t offer any unique benefits related to H-E-B. Target’s Red Card Visa includes free shipping on online orders.

Calling out the fine print here: the 5% cash back is on H-E-B brands at H-E-B stores, not on everything you buy at H-E-B. Other cards like Target’s or Amazon’s are 5% back on all goods purchased at those retailers.

I’m writing about this card because Imprint, a credit card fintech program manager, offers it. I wrote a credit cards-as-a-service overview with Cokie Hasiotis for FTT two years ago. At the time, Imprint was not yet on the market. The landscape has changed tremendously, with new entrants like Imprint and Power (recently acquired by Marqeta) and some early players like Railsr exiting the market and experiencing liquidation.

Imprint has launched a few programs, with H-E-B or Westgate Resorts as two of its higher-profile customers. Imprint and its close competitor, Cardless*, offer a modern fintech approach to co-brand card issuing to compete with traditional co-brand bank issuers, including Synchrony, Bread Financial (fka Alliance Data/Comenity Bank), Chase, and others. Unlike some of the more developer-centric banking-as-a-service companies, Cardless and Imprint do not focus on providing their customers an Application Programming Interface (API) layer but instead white label a hosted solution for the brand. (For example, the HEB card application page is at https://heb.imprint.co/)

Many brands want co-branded credit cards and believe that a co-brand credit will help them to extend their brand, engender loyalty, and gain valuable insights (among other benefits). However, the traditional big issuers (Synchrony, Bread) have very high standards for launching programs. To garner the interest of a Synchrony or Chase, you need to be quite large as a brand, with the real possibility of having more than one million cardholders in just a few years. If your existing customer base is less than 20 or 30 million, you cannot make the case you’ll meet this minimum requirement.

Imprint, Cardless, and others are making a bet that they can out-innovate some of the larger issuers and use smaller, more efficient technologies and teams to support and grow a larger number of customers with smaller programs. As usual, no inside information here: it is possible Chase offered H-E-B a card and Imprint’s offering and terms won, but I think that’s unlikely compared to the H-E-B program simply being too small for a top ten issuer.

There are thousands of brands with loyal and devoted customers. Way back in my time at Green Dot, I worked with H-E-B to launch the Green Dot prepaid card there, and I learned about the store and its many loyal customers in Texas. With a market-competitive offering, H-E-B can achieve its goals without a top-ten issuer on a smaller scale than one would require. Overall, more competition in the space is a good thing for consumers, brands, and providers.

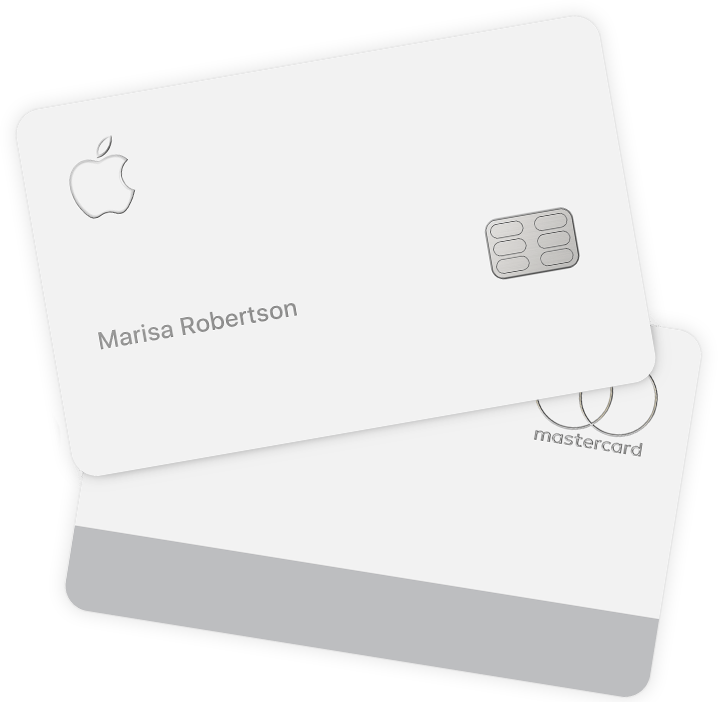

Apple’s New Savings Account

Unless you were off-grid last week, I’m sure you heard that Apple launched a savings account with a strong yield of 4.15%. The savings account is exclusively available to cardholders of the Apple Card issued by Goldman Sachs. (To the prior section, this co-brand is entirely API-drive, with Apple hosting all of the customer-facing experiences.)

I can’t recall a bank or brand requiring you to have their credit card to open a savings account. Some institutions, like credit unions, require you to open a savings or checking account first to be eligible for a loan product, but this works the other way around.

The Apple Card is a cashback card (3% at Apple and select retailers like T-Mobile and Walgreens; 2% with Apple Pay; 1% everywhere else). Without the savings account, cashback is deposited to an Apple Cash Card, which is an account issued by Green Dot Bank. The Apple Cash Card is a typical neo-bank style offering that few people use as a core bank account (as far as I can tell).

Now, you can open an Apple Savings account and move your funds from your card rewards to the savings account and earn interest. The motivation is unclear to me, but perhaps it’s because everyone with an Apple card was behaving like me and simply transferring their cash out of the system once a month to their regular checking account. The new savings account will help you keep the cash in the Goldman Sachs/Apple ecosystem.

The experience of opening and looking at the account is not great and disappointing, given it’s from Apple, the leader in design. I look forward to future iterations of the Apple Card management app that are better and where important things aren’t buried.

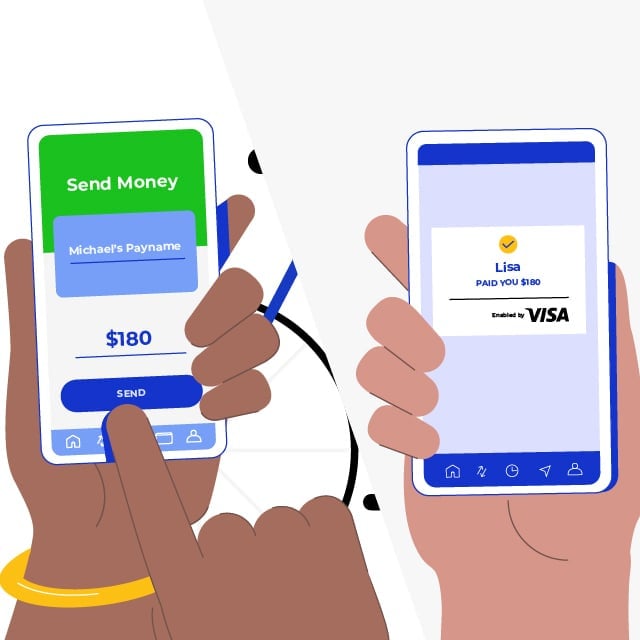

Visa’s New Peer-to-Peer Payments

Visa announced the launch of Visa+, a new peer-to-peer payments system that initially is notable for allowing users to send money between PayPal and PayPal-owned Venmo. Did PayPal need Visa to connect their two platforms, or is this a PR stunt? You can already use Visa Direct (or its equivalent, Mastercard Send) to send money between two different debit cards or Zelle to send money between two people’s bank accounts.

Visa says that Visa+ will launch to consumers in late 2023. It would be useful if you could transfer between peer-to-peer systems and not maintain a bunch of apps. I use Cash App with some friends, Venmo with others, and Zelle with a third group. Not maintaining three apps would be good, but I think all the platforms will have to play nice for this to work. I’m not sure they are incentivized to do so - on-us transactions inside Square Cash App or Venmo will be more economically efficient for the platform.

Visa says Visa+ won’t require a Visa Card, which is weird. Meanwhile, risk teams everything are groaning about the new approaches to fraud this might enable.

I look forward to trying this out later in the year. Feel free to try it by sending me some cash when it launches!

CardsFTW

Thanks for reading CardsFTW, an occasional newsletter about debit and credit. It's written by Matthew Goldman, founder of Totavi, LLC, a boutique startup product and consulting firm. Learn more about him on LinkedIn and visit totavi.com. Contact me for 20 years of experience in building your next product.

*Indicates a company with whom Matthew Goldman or Totavi, LLC has a current or prior financial relationship.