Notes from the Fed’s Payments Study - CardsFTW #58

Plus, Mastercard and The Sherman Act; TD Bank’s New Cards

Notes from the Fed’s Triennial Payments Study, 2022 Edition

Frequent readers won’t be surprised that I love to read the Federal Reserve Board’s Payments study. It’s one of the most comprehensive views of how we pay for things in the United States and how that changes over time. While people know the Fed for interest rate policy and bank regulation, some of the most exciting research and work comes from the payments center.

You can read the report and review key findings on the Fed’s website. I’ll highlight below what stood out most to me. There is a strong theme around the continuing shift to electronic payments. This shift is both a long-term secular trend and a short-term boosted trend from the COVID-19 pandemic.

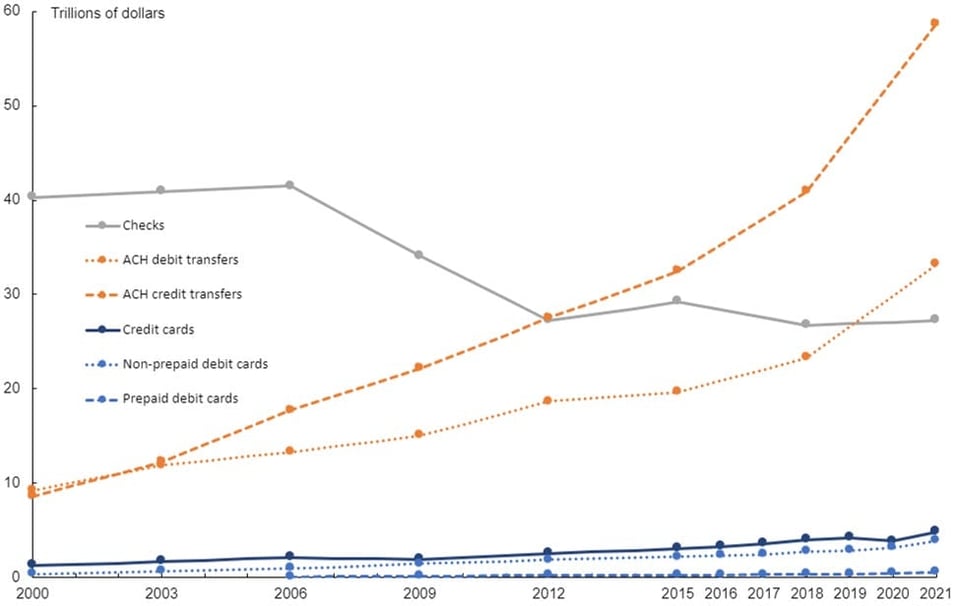

- Noncash payments grew 9.5% per year between 2018 and 2021

- Automated Clearing House (ACH) is driving this–with more than 90% of the rise coming from ACH.

- More noncash payments move by ACH than anything else. ACH is 72% of core noncash payments and almost 92 trillion dollars annually.

- We’re writing fewer checks, but they are bigger: The average check is now $2,430, but the number of checks has declined 7.2% per year since 2018.

- Card payments grew faster than previously measured by the Fed, rising 10% per year to more than $9 trillion (approximately 7% of noncash payments). The room to continue to grow here is enormous (see ACH volume above).

- Debit cards continue to grow rapidly (13.7% CAGR 2018-2021 in volume.)**

- While ACH payments are the largest by volume, card payments are the largest by transaction count–with more than 84% of all noncash payments taking place on a card, some 157 billion payments in 2021, representing 77% of all noncash payments.

- As people use less cash, they don’t need to visit the ATM. ATM cash withdrawals declined both in number (by 10.1% to 3.7 billion), but also in total value. We are taking out more money per withdrawal, with an average withdrawal of $198 in 2021.

Specific to my favorite topic: credit card volume grew 7.0% annually over the 2018-2021 period to $4.88 trillion. The average credit card transaction increased a small amount to $96 per transaction, up from $91 in 2015. Credit card growth is slowing: volume grew at an annual rate of 9.3% in the last triennial survey (2015-2018). The number of non-prepaid debit card payments increased the most of all card types.

Over the past few years, the shift to online commerce and online work has accelerated most trends in moving payments to noncash and electronic payments. I expect this trend to continue. The next survey will also need to include the direct impact of real-time payments from systems like FedNow and Zelle.

While this newsletter may be called CardsFTW, I am a fan of all electronic payments, including ACH. I am not surprised to see the acceleration in growth across payment types, although there is a warning here for credit card companies. Buy-now, pay-later has shifted some card payments to ACH effectively (the payments are account-to-account, just split apart and taking place over time), and cards have a well-deserved reputation as a confusing financial product.

The growth in debit card payments is partly due to the simplicity of the good-funds model: I can only spend money already in my account. Good-funds is the electronic equivalent of cash: I can only spend what I have in hand. We can expect to continue to see debit growth. Suppose card companies want to continue to grow their share of payments: In that case, they will need to make substantial inroads into large dollar transactions and commercial payments (which also sort of go together). I will cover some recent corporate and commercial card innovations in an upcoming edition of CardsFTW.

Mastercard’s Anti-Trust Disclosure

Mastercard is no stranger to lawsuits (neither is Visa). A quick review of their recent 10-Q has pages of lawsuits to disclose. One that stood out to me was this disclosure:

In March 2023, Mastercard received a Civil Investigative Demand (“CID”) from the U.S. Department of Justice Antitrust Division (“DOJ”) seeking documents and information regarding a potential violation of Sections 1 or 2 of the Sherman Act. The CID focuses on Mastercard’s U.S. debit program and competition with other payment networks and technologies. Mastercard is cooperating with the DOJ in connection with the CID.

While many past lawsuits have focused on areas regarding credit card interchange fees and the rules preventing merchants from implementing credit acceptance surcharges, this brief notice indicates potentially new problems specific to debit card business agreements. My suspicion here is that debit card routing activities may be under scrutiny. Cards in the US are required to enable alternative debit routing onto networks not owned by the same brand that processes the card’s signature transitions (e.g., using Pulse or Accel on a Mastercard, not just Mastercard’s own Maestro network).

The Sherman Act was passed in 1890 and was used to break up AT&T. Section 1 simply states that “Every contract, combination in the form of trust or otherwise, or conspiracy, in restraint of trade or commerce among the several States, or with foreign nations, is declared to be illegal.” while Section 2’s key language includes “Every person who shall monopolize, or attempt to monopolize, or combine or conspire with any other person or persons, to monopolize any part of the trade or commerce among the several States, or with foreign nations, shall be deemed guilty of a felony….”

Networks have many characteristics of monopoly businesses, although I don’t think Mastercard is a monopoly, nor can it be without cooperation from Visa. That doesn’t prohibit them from attempting to monopolize trade. There is little in the disclosures, so my wild guessing will focus on routing, but this will be a situation to watch.

TD Bank Introduces new credit cards

It’s been an exciting week for TD Bank1 Regulators this week blocked the American banking arm of Canadian giant Toronto Dominion (the Canadians love the word “dominion”) from acquiring First Horizon Bank, primarily citing failures in TD’s anti-money laundering compliance. (Note: Why are big banks so bad at AML?)

Meanwhile, TD introduced an innovative, new suite of credit cards. TD does not have a large national credit card business. It has traditionally acted as many other regional banks do: primarily offering cards to its existing customers in its home geography. This locals-only approach limits risk by the bank but is a challenging path to growth when the top credit card issuers are showering consumers with rewards in their national offerings.

The new TD Clear card is something different, and I can’t wait to see if it’s successful. (It doesn’t appear to be an actually clear plastic card, though, because the 1990s are over). The TD Clear is a subscription-based credit card with no interest charges. Consumers only pay a flat monthly fee (no foreign transaction fees, no annual fees, no cash advance fees, no over-the-limit fees, no returned payment fees, and no interest charges.) Consumers can choose between two products: a $10 monthly fee for a $1,000 credit limit or a $20 monthly fee for a $2,000 credit limit.

The bank also introduced TD FlexPay. The TD FlexPay card focuses on flexibility for cardholders with a few interesting features:

- The option to skip a payment once a year (available after the first six months of account opening)

- Cardholders will also automatically have their first late fee refunded every twelve billing cycles.

These first two cards have features designed for users with balances or lower credit capabilities. The bank also revised its prime rewards card offers.

The bank made a few strategic changes to the TD Double Up card, reducing complications and restrictions on the rewards. The revised card earns a flat 2% on all purchases every day. The biggest competitor in the space is Citi’s Double Cash and Wells Fargo’s Active Cash Card. These generous cards often top “best of lists,” I am curious to see if a regional (albeit a very large regional) bank can break into these lists.

The TD Cash card will continue to offer a 3/2/11 reward structure but is shifting from 3% dining and 2% grocery to a choose-your-own-adventure structure, allowing users to pick a particular category each quarter for the 3% and 2% category, with 1% everywhere else. There are no limits on these categories, which is a key differentiator to similar offerings like Bank of America’s Customized Cash card, which has a 3/2/1 structure with a choice on the 3% category, but with a $2500 per quarter limit on the 3% and 2% categories. Bank of America still wins on rewards for its highly-engaged customers, who can earn up to a 75% bonus if they maintain preferred customer status with the bank (done through combined deposit and investment levels).

CardsFTW

Thanks for reading CardsFTW, a debit and credit newsletter by Matthew Goldman. Matthew is the founder of Totavi, LLC. Totavi is GSD Product Consulting, helping to bring real, operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit totavi.com to learn more and engage us.

** Correction: This bullet point was originally misstated in the original email publish and has been corrected.