Current Creates a Charge Card with Cross River Bank - CardsFTW #72

Plus, Guava Card & quick news

Cross River and Current Launch a Charge Card

Current is one of the largest digital neobanks in the US market. Long known for its core debit card product, Current announced their new Build charge card, a secured credit product. The launch comes more than three years after neobanking industry leader Chime first launched its secured credit card product. More recently, several other challenger banks have entered the credit card space, such as M1 with their Owner Rewards Card

This newly minted Build card is emblematic of the innovation we're seeing in the credit and charge card sectors of fintech. While the previous decade was dominated by fintech entities battling it out in the core checking accounts arena (sans the checks, of course), the current one is leaning towards creativity on the credit front.

The Build card, akin to other credit builder contemporaries like Chime, Extra, and Fizz, subtly melds the realms of debit and credit. Historically, the dichotomy was clear: cards either revolved (credit) or didn't (charge) and they either had an asset backing them up or they didn't. But the Build card offers a fresh blend—your debit account's balance anchors it yet doesn't allow for revolving it. It's a curious blend of debit functionality while fostering credit growth.

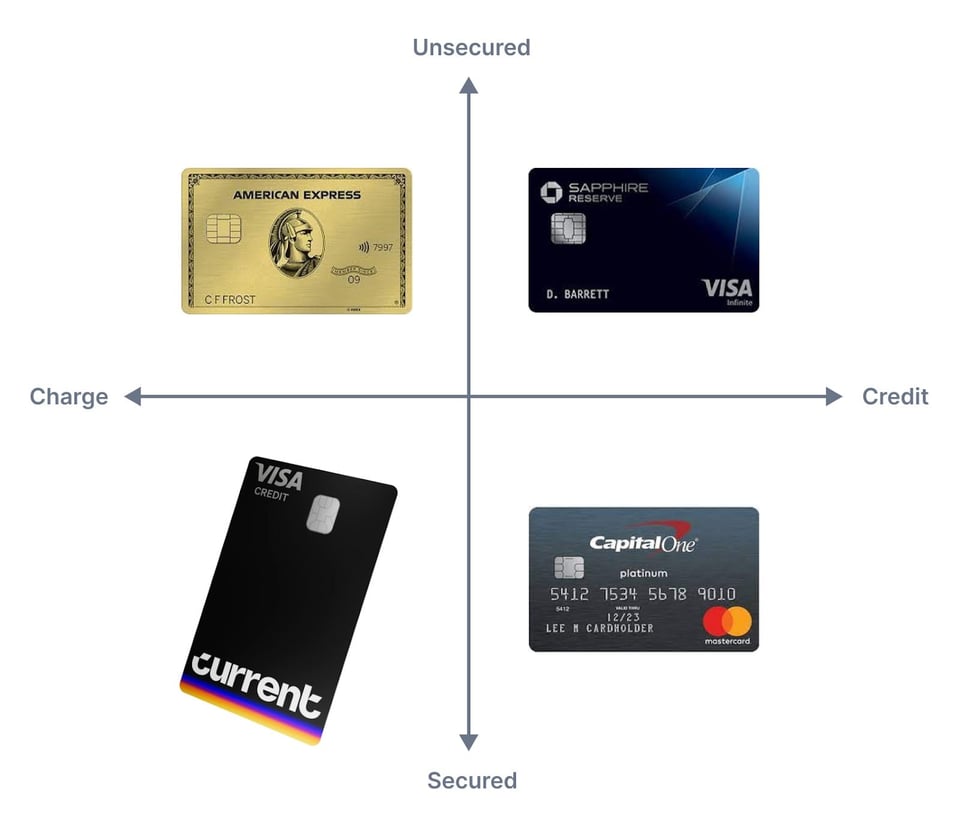

Your card could either revolve (credit) or not (charge). Your card could also be secured with an asset or not. Simple.

Common examples include American Express’s legacy charge cards (unsecured) vs. Chase’s Sapphire cards (unsecured but revolving) and Capital One’s secured credit product (also revolving). The Build card goes in a new spot. It’s sort of a debit card, but it also builds credit.

Back in May, Cards FTW 57 discussed these cards at length. Current is not the first one to the party, but they are one of the largest companies to show up.

The card has only been on the market for a few days, and I haven’t had time to research thoroughly, but I think it demonstrates an interesting product direction and some regulatory gray area. Traditional rules around what makes a card prepaid get blurry here. The CFPB even has a decision flow chart dedicated to this. By no means am I suggesting that anything funny is going on here, but I do think it shows how innovation can outpace traditional rules.

Guava Card

Guava launched a card product for Black entrepreneurs and created a business owner network. They accompanied this launch with news of a $2.4M pre-seed round. We’ve seen quite a few neobanking products focused on a particular identity, but I have seen fewer business card products with this angle. The card features appear to be everything you would expect from a standard small business deposit account. The business owner network is the unique play here, and it’s a compelling part of the experience. Entrepreneurship is often a very lonely existence, and it is that much harder when you are part of a group that historically has been shut out of many networks and funding options.

Quick News

Fintech trailblazer Figure recently backpedaled on its charter application, echoing similar moves by its peers in the fintech domain. The road to securing a bank or initiating a de novo charter seems more twisted than many anticipate. It prompts reflection: Is it necessary for fintech entities to secure these charters? Acquiring your own bank is very expensive and fundamentally changes your valuation, exit, and ownership options. While there will also be a desire for vertical integration to own your charter; I think that technology companies should focus on their roots and put that money to better use.

East West Bank, in my hometown of Pasadena, CA, finds itself ascending to the apex position among California-chartered banks, particularly after the tribulations of Silicon Valley Bank and First Republic. Rumblings suggest a possible targeting of some SVB clientele. Could this signify an imminent pivot towards fintech sponsorship? It's certainly worth monitoring the scene closely!

CardsFTW

Thanks for reading CardsFTW, a debit and credit newsletter by Matthew Goldman. Matthew is the founder of Totavi, LLC, which provides GSD Product Consulting with real operational value. Visit totavi.com to learn more and engage us.

* Indicates a company with whom Matthew Goldman or Totavi, LLC has a financial relationship.