Sending Money, with Credit - CardsFTW #8

More digital checkout buttons, restaurant points, and going to the bank

Sending Money, with Credit

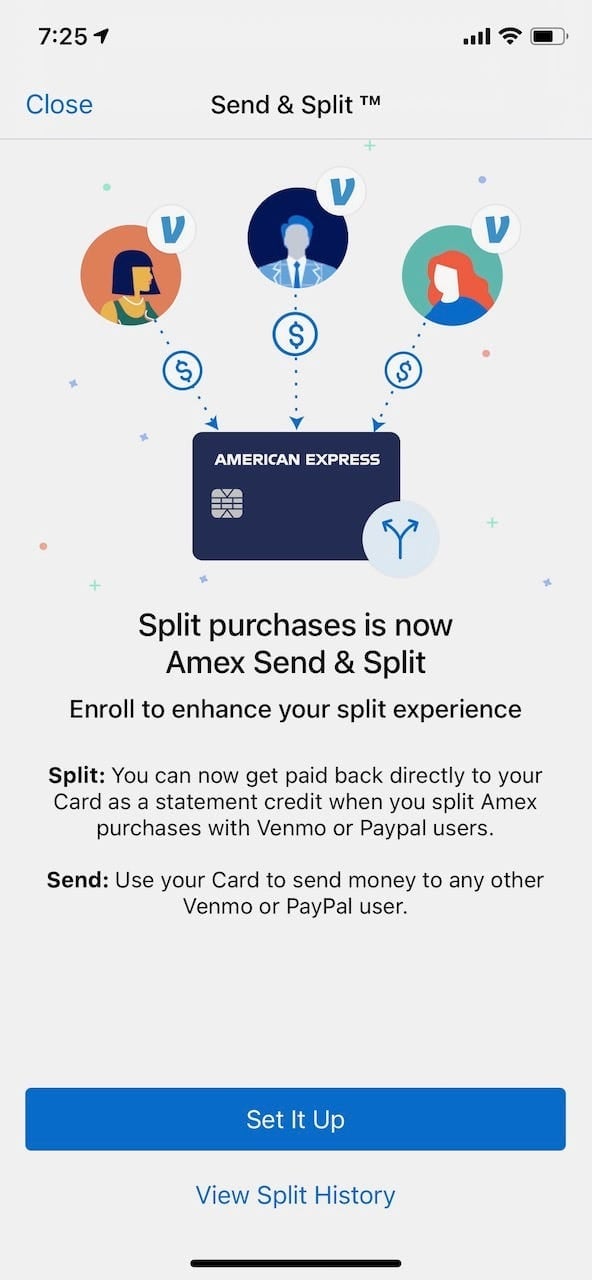

American Express announced a new feature that allows consumers to send cash via PayPal or Venmo and fund it with their existing American Express credit or charge cards with no fee. This news received little notice from what I can tell, but I think it is by far the most exciting news of the week.

Digital peer-to-peer payments have grown tremendously in the past decade. Sending money to friends with Venmo, Square Cash, and PayPal are huge drivers of digital payments and a new part of everyday life (even more so with COVID-19). Funding those payments requires cash from the sender, of course, and, usually, funding those payments with an open, revolving credit line involves the sender paying a fee of around 3%, covering the standard merchant interchange that retailers typically pay.

American Express started to dabble in this space earlier with a feature in their app that allowed you to split a charge with friends. We all know the scenario: A group of friends goes to dinner or buys a gift and needs to split the charge. The easiest way to pay whoever pulled out the card to pay for the meal or item asks people to send their share via Venmo or Square Cash.While much of this is informal, American Express rolled out a feature earlier that let you select a particular transaction, split it, and send a request to your friends via Venmo to pay you back. The funds would be deposited to your Venmo account (and you still needed to pay your Amex bill).

With this new feature, you can fund a payment to your friends from your credit line with no fee. The process is a bit complicated, but once set up, sending money is easy. Consumers need to enroll their American Express account from their mobile app by linking their Amex account to their Venmo or PayPal account (or both). Following enrollment, you can fund a prepaid Amex Send balance. This Amex Send balance appears to be a new account Amex is creating for you on the fly in their banking platform. You can fund the balance from your existing American Express cards at no fee. I have several Amex cards, one Gold charge card (no limit) and two credit cards (Blue Cash Preferred and Bonvoy) with traditional credit card limits. The app allowed me to charge up to $2,000 each from each card ($6,000 total) and fund the Amex Send account. (No, I didn't do this.) Amex didn't charge any fees, but interest will accrue if I don't pay on time, and I won't earn rewards on these charges.

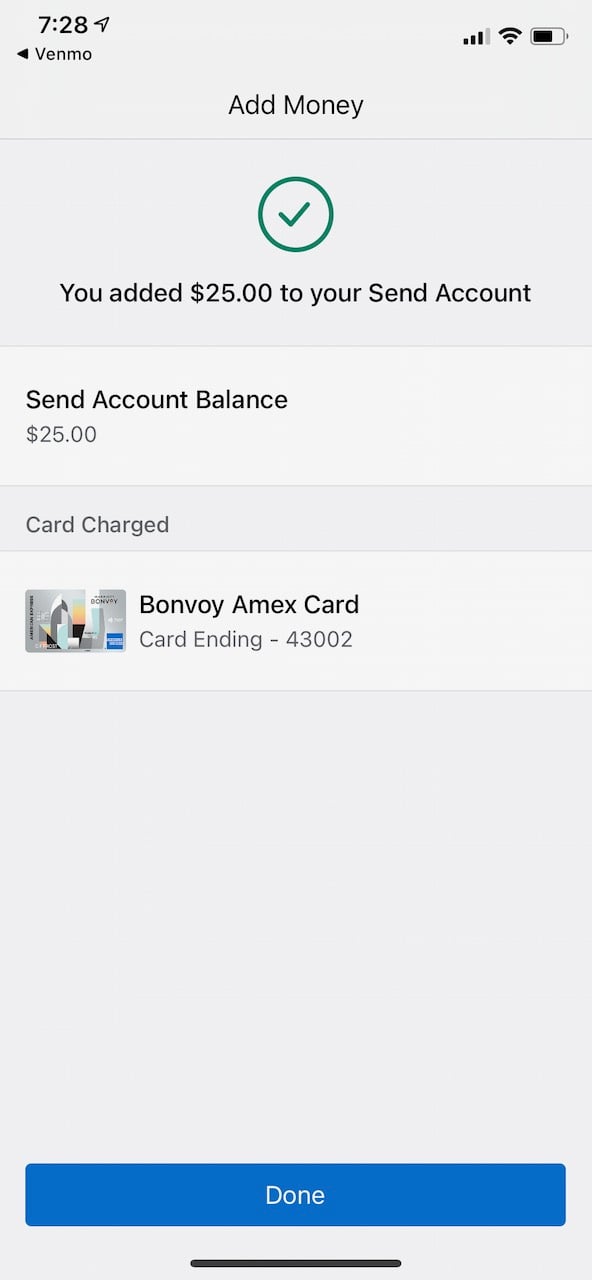

With $25.00 in my Amex Send account, I could send money out via both PayPal and Venmo. It was all effortless and my test recipients received their funds as usual.

As a user, this is a great way to get a short-term loan. I could pull money from my Amex credit line and pay $0 fees for domestic transfers, provided I pay my bill on time. The legal wording says that this transaction is treated as a purchase, not a cash advance, giving you the usual grace period and a lower APR if you do revolve the balance.

I was surprised to see this new feature because there appear to be little economic incentives for American Express. Unless I missed some fine print, they may earn no interest, no fees, and no interchange on these transactions (unless I missed some fine print!). Perhaps this is a long play, as it will allow Amex to take a leading place as a more dynamic credit card company in a payment flow for younger consumers.

There is a strategic rationale to be positioning Amex as part of your everyday payments, driving American Express cardholders to use their card more both for splitting purchases and funding these peer-to-peer transfers. There could also be a more significant play here around that Amex Send account and the long-considered questions about whether American Express will get into everyday banking, building on their existing credit and savings products.

With the rise of many more digital banks, American Express can position itself as a significant national full-service bank. They have many of the assets: a proprietary network (which enables superior economics compared to other issuers) and a great brand. American Express has spent considerable time and money working in prepaid before, each time eventually closing down the significant experiments (aside from gift cards) because it just didn't work. However, consumer expectations for banking continue to evolve, and now might be the right time. After all, if Goldman Sachs is getting into everyday banking, why wouldn't another Wall Street blue blood firm follow? After 150+ years, it might finally be time for American Express to go full service.

Do Not Pass Go (Bank)

Green Dot has been evolving faster since former NetSpend CEO Dan Henry took over at the beginning of the year from founder and CEO Steve Streit. Green Dot is growing as a banking-as-a-service platform, powering notable experiences like Uber, Stash, and the Apple Cash card. However, its consumer business is under pressure. While there was a time when Green Dot was near the only option for the un- and underbanked, the rise of challenger neobanks, such as Stash, Current, Chime, Square Cash, and others, have siphoned users and increased marketing expenses.

Green Dot previously launched a mobile-first product that was more a neobank than the traditional reloadable prepaid card (a distinction perhaps lost on users but beloved by fintech nerds) called GoBank. When that didn't take-off, they launched Unlimited by Green Dot last summer with high headline rewards and interest, but lots of fine print. Now they are launching Go2Bank, which looks like all their other products, but with a new name. I am not impressed. I don't think this one will make it around the board and collect $200. See more in American Banker (subscription required).

Discover Joins Click to Pay

The networks have been attempting to join the digital wallet and faster checkout experience for years. There have been attempts by all the networks over the year, notably Checkout by Visa, which has morphed into the latest "Click to Pay" wallet, which now features the ability to support Visa, Mastercard, American Express, and now Discover. Every time you see this handy logo, you can pay from a tokenized digital wallet:

- You enter your email.

- You receive a code.

- You can pick a card and pay.

Now you're wondering how or why this could be better than just typing in your card number or using PayPal, ShopPay, Apple Pay, Google Pay, or even Stripe. It doesn't seem to be better, easier, simpler, or more secure (at least to users). This continued effort on the part of the networks makes sense in that they need to have their option through the EMVCo standards, but unless a powerful ecommerce platform rolls it out widely (which I doubt), this latest attempt will languish.

An Update on Travel Rewards

This week brought more news of how the major credit card issuers are attempting to deal with how the total lack of interest in travel by consumers compares with their primary focus on travel credit cards (seems like we update this every week!). Chase announced that Chase Sapphire Reserve cardholders, who pay $550 per year for their cards, will continue to earn triple points at grocery stores from November 1st through April 30th, 2021.

Meanwhile, American Express noted that cardholders are stockpiling their rewards and assume it's because people will want to travel again. I'm sure there is some truth to that, but it's also true that the other options for redeeming American Express Membership Rewards points are not good (dropping effective earnings rates from 1% to 0.6% when used in their merchandise mall). I am sitting on more than 750,000 hard-earned Membership Rewards points myself. It's not that I don't want to use them; it's that there aren't any good ways to do so!

More Cards at CardConExpo 2020 (Next Week!)

Last chance to sign up for CardConExpo, a (virtual) conference dedicated to credit cards! Produced by Jason Steele, longtime credit card journalist and Director of Credit Card Content for Money.com, CardCon is a must-attend! The all-virtual 2020 edition is a few hours daily November 16-19th. My panel is on Thursday, November 19th, focusing on startups in the credit card space. Joining me on the panel will be Moderator Melissa Long of MaxRewards and two other entrepreneurs: Kristy Kim, CEO of TomoCredit, and Vrinda Gupta, CEO of Sequin Card. CardsFTW readers get a 25% discount with the code "Goldman2020" Register via Eventbrite.

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you're looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.