Mastercard & Postmates Break Up - CardsFTW #1

and other COIVD-19 effects on the credit card world

An Introduction

Welcome to the inaugural edition of CardsFTW. There are so many great newsletters and websites covering banking, fintech, and personal finance. Still, I haven’t found one that focuses on credit and debit cards as products with a viewpoint that straddles consumer value and industry analysis.

We will be covering both startup and traditional issuers of credit cards, debit cards, and prepaid cards. We will focus on the U.S., but bring in international news that stands out. The goal of this newsletter isn’t to help you save money and we can’t replace The Points Guy. We’ll report on big-deal offer changes and new products, but not on individual deals or coupon codes. If you love cards, either personally or professionally, we know you’ll find some thing interesting each week.

Time to Switch to DoorDash

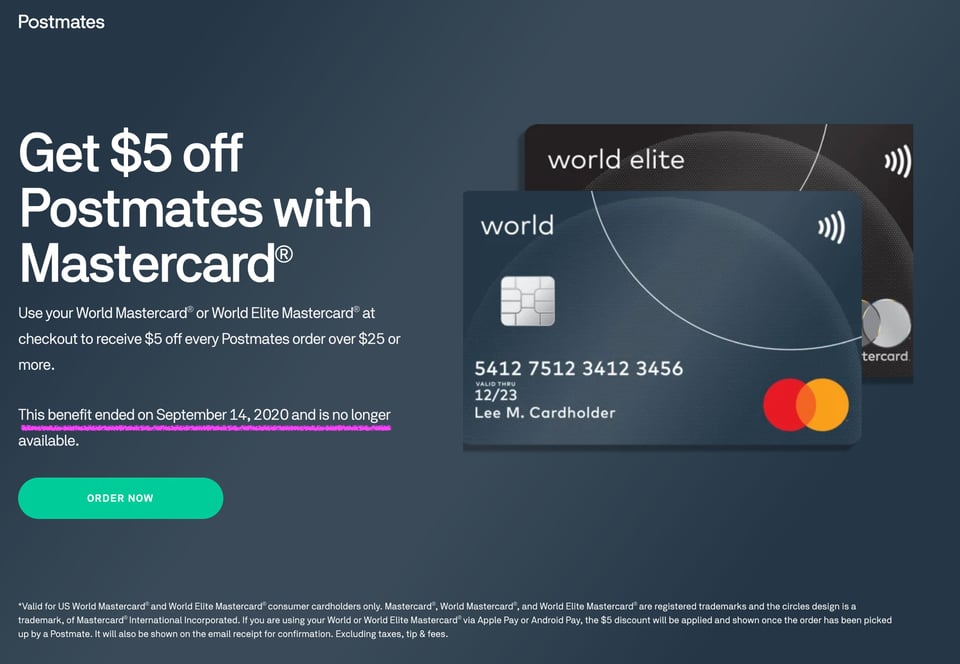

In April 2019, Mastercard launched a slew of new benefits for holders of their World and World Elite card products. The easiest to use and highest consumer value benefit was a $5 discount on every Postmates order of $25 or more. With no limitations and the spike of frequent, quarantine-induced Postmates purchases, this offer had hundreds or even thousands of dollars worth of value for Mastercard World cardholders.

While attempting to take advantage of this benefit myself last week, I noticed that, with no public announcement, the offer was gone. The Postmates website simply stated, “This benefit ended on September 14, 2020 and is no longer available.”

Screenshot from postmates.com, September 17, 2020

Given Mastercard’s limited income on an individual transaction (around 13-15bps), I have always assumed this was paid for by Postmates, with Mastercard providing the marketing benefit as their contribution to the deal. It’s hard to tell if this is due to the early July proposed acquisition of Postmates by Uber, the massive cost of this benefit to Postmates, or something else.

To quote a friend:

Ugh. That sucks.

It sure does and represents a key challenge of these deals: They provide high consumer value and create significant negative brand value to all parties when discontinued.

Both Mastercard and Visa have developed a set of benefits for their premium product lines, such as travel insurance, ShopRunner membership, and cellphone insurance. Over time, many of these benefits have trickled into even the most basic credit and debit card products. If you have a single credit card, the value of any one of these benefits can be large, but as you add cards to your wallet, the benefits to overlap. A great example is the first card you receive with a free ShopRunner membership, which gives you $99 in value (what that membership costs), but the second card with the same benefit adds no value.

If a feature is never used, does it have any value? When I was a product manager at Green Dot, we offered a travel-oriented prepaid card, which included a travel emergency insurance policy that could whisk you home if you were in medical distress. We asked our Visa rep how frequently it was used. He said it had never been used.

The networks and banks tend to pull back on these benefits whenever they are used frequently. Trip cancellation insurance has long been included in credit cards, but we’ve seen them removed from card products since the start of the pandemic. Mastercard once included a price protection feature on all of their cards, and Chase had a program for their Visa cards as well. When Earny and other startups made it easy for consumers to claim on these programs, the cost skyrocketed, and the networks and banks removed the feature.

As our world has changed rapidly this year due to COVID-19, so have these card benefits. I anticipate an acceleration in change as card networks and banks attempt to both limit their costs and provide high value to their cardholders.

Challenger Cards

Chime, the neobank started in 2013 by my former Green Dot colleague Chris Britt, announced new funding of $485M, bringing its private market valuation to $14.5B. Chime claims more than 8 million active accounts and has hit EBITDA profitability. The company started in the pure debit card space before adding savings and a very innovative secured-card program earlier this year. Chime’s cards are issued by The Bancorp Bank and Stride Bank, N.A. for debit cards and Stride for credit. They are processed on Galileo and use Visa as their network. I continued to be impressed by Chime’s growth. I am very impressed if they have hit profitability, as their no-fee model has very limited revenue opportunities.

X1Card announced the waitlist for its new credit card product. This card is being developed by the team behind ThriveCash, which previously raised $11M from some big-name investors, including David Sacks. The buzz was intense with product features including very high reward cashback rates. The card will earn 2% cashback on all purchases and 3% cashback on all purchases over the first $15,000 in annual spend. In addition, they are promising 30-day boosts to 4% for cardholder referrals. Other features include a heavy (17g) card and instant digital virtual cards. At last check, 130,000 people joined the waitlist. X1 says they have underwriting that values income instead of your credit score and that no hard credit inquiry is required. I don’t understand this, as a hard inquiry should be required by credit bureau rules. Card images include Visa Signature branding, but these earnings rates appear unsustainable with a Visa Signature product. And we don’t know the issuer. Either X1 has a cease and desist from Visa branding, or they do have a bank relationship. In all cases, this card sounds too good to be true.

Sequin Card also announced its waitlist. I’ve had a chance to chat with founder Vrinda Gupta a few times in the past month. While they have a ways to go before the first card is issued, I like their approach to helping women understand and earn credit, as well as receive relevant discounts. I am a big fan of products that market to and are designed for specific groups (like wine lovers 😉🍷), so I am in Sequin’s corner. No known bank here, although Visa looks to be the network as Vrinda is an alumna of the organization and the company is enrolled in the Visa fintech program.

MSCHF, best known for a pair of faux Nikes (the Jesus Shoes), launched a bound-to-go-viral multiplayer debit card built on the new Privacy.com issuing stack. Called Card v Card, users are sent a physical card with no account number on it. They are notified when a deposit is made to a shared ledger, and then it’s a race to spend the money before someone else does. This whole thing seems ridiculous, but if you love giveaways, you might be able to snag some great free products.

Everyone Gets a Co-brand

Barclaycard launched new co-branded cards with Emirates. The new Mastercard products are your basic airline cards and don’t have any unique features. The $99/year Emirates Skywards Rewards World Elite Mastercard® and $499/year Emirates Skywards Premium World Elite Mastercard® include the usual array of elite status with the spend, points bonus, and lounge access features. If you’re a frequent Emirates flier, they probably make some sense.

Wells Fargo launched a new co-branded card with Hotels.com. This is a poorly timed-announcement, given hotel revenues are down more 70% on the year. As with most Wells Fargo cards, the card has a pretty lackluster offer and yet is still somehow confusing. You earn “stamps” instead of points – think a cardstock loyalty punchcard at your local sandwich shop. You earn one stamp per $500 spent on the card and one stamp per night spent at a property booked through Hotels.com. Based on redemption options, this could work out to 2.0-2.2% cashback, which sounds great, but somehow this card makes it sound, well, not great. Just remember not to punch actual holes in your Hotels.com credit card.

Citibank announced it is issuing a co-branded card with Wayfair, which has been having a fantastic year. This one also surprised me because retail co-brand cards are on the definite decline, but existing Wayfair-issuer Comenity already disclosed their partnership was ending this year. Citi will issue both a Mastercard and a private label card. The Mastercard product will earn 5% cashback at Wayfair, 3% back at grocery stores, 2% on online purchases, and 1% everywhere else. That is a lot of categories for a store card, but a definite trend of late (see Verizon’s recent offering).

Chase Changes Popular Products

Chase rolled out the previously-announced new Chase Freedom Flex Mastercard. This card is an evolution of the long-standing and most-popular Chase consumer card Chase Freedom. The new card adds three accelerated earnings categories (5% on travel purchased through Chase, 3% on dining, and 3% at drugstores) to the traditional 5% quarterly rotating category structure and 1% everywhere else structure. I’m most intrigued that Chase did a deal with Mastercard on this product, especially considering the economic power of the Chase/VisaNet processing deal, which gives Chase a huge incentive to partner closely with Visa. I’m unclear if I should upgrade my Chase Freedom, but I do love new plastics, so I’ll probably try to move my existing Freedom to the new card. The only downside appears to be that you can’t use the card at Costco.

Chase also started taking applications for their updated Chase Freedom Unlimited, which moved from a 1.5% cashback on everything, just the basics, keep everything simple card, to including accelerated earnings categories (5% with Chase travel and 3% on dining and drugstores). This one really confuses me. These cards are almost the same. I thought the whole point of Freedom Unlimited was the lack of bonus categories.

Not-a-Card Card News

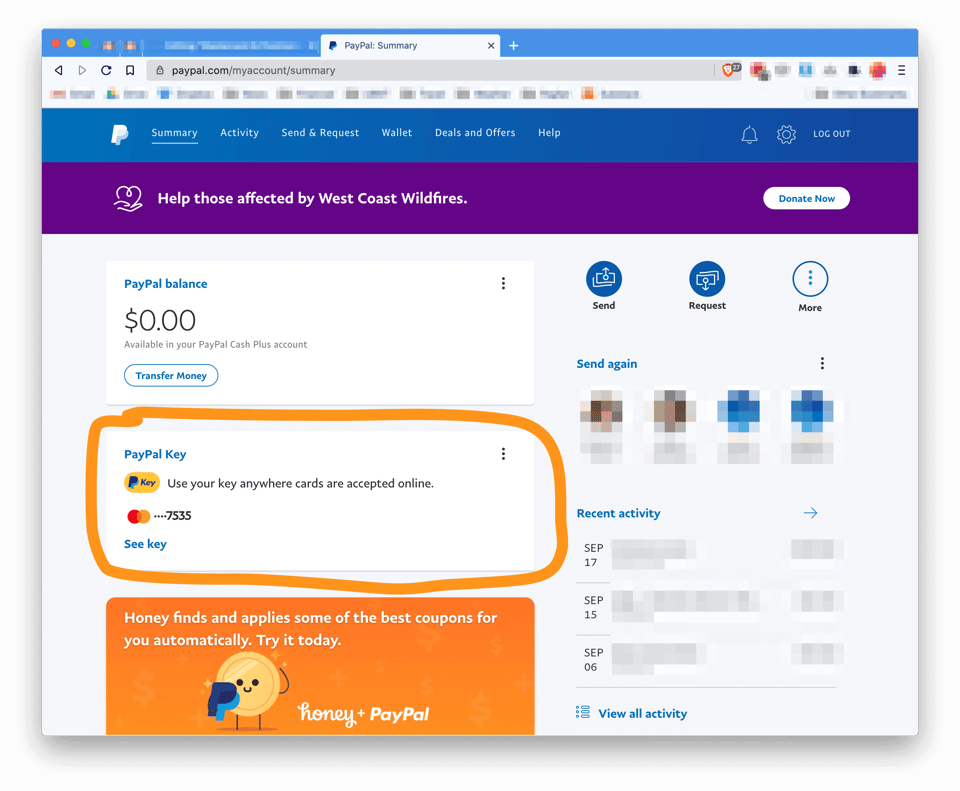

PayPal Key on the PayPal Dashboard

PayPal quietly rolled out PayPal Key, which Forbes described as “hiding in plain sight.” PayPal Key is a virtual Mastercard card which you can use on any ecommerce transaction by typing in the virtual card number. The company is enjoying its share of the 45% year-over-year growth in ecommerce in Q2 (per the U.S. Department of Commerce). This new product allows you to use PayPal on any website, not just those with a PayPal integration. Signing up for PayPal key isn’t obvious in your account and it’s unclear if all users are eligible. This direct link should take you to a setup page. PayPal will then fund the transaction with your existing PayPal payment source, such as your balance or another card. This type of over-the-top-wallet is what Curve is doing in the U.K. (and which Curve will launch soon here in the U.S.) I tried to build this at Wallaby in 2012. At the time, and as a small startup, Mastercard did not allow us to create this type of payment layering. With PayPal Key and Curve, it’s clear that the rules have changed and this type of card-within-a-card wallet is acceptable.