Underwriting is More Than Your Score - CardsFTW #210

Plus, the CFPB thinks people complain too much, and a new credit card for lawyers

Mercantile Launches ABA Card

Mercantile is a provider of co-brand small business card programs for professional associations, a decidedly old-school approach to card marketing. The company was acquired by Onboard Partners (formerly known as The Kessler Group) in January, 2025 (an under-reported acquisition, if you ask me).

Now backed by a large amount of capital and credit card expertise, Mercantile issues cards for associations like:

- American Association of Orthodontists

- Massachusetts Medical Society

- Academy of Doctors of Audiology

- Academy of General Dentistry

- American College of Physicians

- American Optometric Association

- Radiology Business Management Association

- Florida Medical Association

- National Funeral Directors Association

The latest entries, like that last one above, are a further extension outside of medical, with the American Bar Association and the American Society of Interior Designers. Both of these cards are issued by Celtic Bank and operate on the American Express Network. Earlier cards are issued by Hatch Bank and ride the Mastercard network.

This approach of co-branding to a traditional membership society was well-developed by MBNA, which was acquired by Bank of America, who eventually closed most of these cards. I’m surprised it still works, but I will commend Mercantile for doing more than slapping a logo on the cards by providing some unique benefits per association.

CFPB Makes Moves on Complaints

The Consumer Financial Protection Bureau, which under current leadership may not be interested in protecting consumers, announced a series of changes to its complaint system. Apparently, consumers complain too much.

OK, that’s in jest about this administration, but there is some truth to the rise of automated and AI-assisted complaint tools that attempt to get legitimate credit bureau complaints removed. The CFPB reports that credit or consumer reporting complaints have ballooned more than 3700% between 2019 and 2025. Maybe companies are acting worse, maybe consumers are getting smarter about their rights, or maybe there is a legitimate complaint here from the bureaus.

The press release is not that detailed, but I know that both things can be true at once:

- Consumers have valid complaints about inaccurate information on the bureau reports and have trouble getting these fixed

- Consumers have invalid complaints about accurate information on their bureau reports

We’ll have to keep an eye on this.

How Credit Card Underwriting Works

I have enjoyed the privilege of sitting in many places in the credit card world: affiliate marketing, program management, personal financial apps, rewards optimization, and underwriting. Through my work at Totavi, I help companies launching credit card programs with underwriting policies and procedures for consumer revolving credit cards.

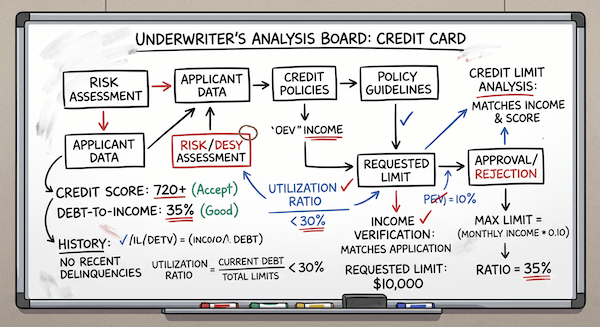

Part of this role is in teaching clients (and end applicants and cardholders) about underwriting. Education about credit scores has caused the general public to think that approval for a credit card comes down to a single number. You either "have a good score" or you do not. In reality, credit underwriting is far more nuanced. Lenders are making a forward-looking decision about risk, not simply reacting to a snapshot. Your credit score is one input. It is far from the only one. While many people use credit cards transactionally without carrying a balance, a credit card is a loan, and so companies must be able to evaluate the creditworthiness of an applicant prior to issuing a new credit card.

Understanding how underwriting actually works helps you predict outcomes, avoid surprises, and make more informed decisions about how to manage your credit profile.

Will You Repay?

At its core, underwriting answers a simple question: If this lender extends you a line of credit, what is the likelihood you will repay it as agreed? Underwriting is a process to evaluate if you, as a prospective cardholder, will be able (and willing!) to repay the credit extended to you.

An underwriting policy is designed to accept a specific amount of risk (some losses are inevitable). Each product has its own tolerance based on its goals and financials. For example, banks focusing on subprime and nearprime users may experience net chargeoff rates up to 10%, while prime programs may target 2-4% net chargeoff rates.

In Practice

In practice, when you apply for a card, you submit your name, birthdate, social security number, income, and housing payment. Your income may simply be self-reported (lying about this is a crime!) or it may be verified with bureau or cash flow data. Your housing payment (own vs. rent, amount) is used to determine what constitutes your discretionary income.