Wells Fargo’s Self-Care Card - CardsFTW #110

Plus, Apple Wallet Enhancements, Visa DPS Credit, and More

Wells Fargo’s New Self-Care Card

No card has garnered so much activity in a Totavi Slack thread as the new Wells Fargo Attune World Elite Mastercard. After many years of staying out of the mass-market rewards card game, Wells Fargo has been on an absolute tear this year, launching card after card after card.

The New Attune℠ World Elite Mastercard® provides 4% cashback on fitness and self care, including select sporting and entertainment, plus good-for-you categories like public transit, EV charging, and thrift stores. The card reminds me of what the team at Ness was trying to do (RIP) with cardholder rewards focused on something other than travel and more personal.

The categories included for accelerated earnings on this card include rare or brand-new ones. There have been a few attempts at pet cards, either direct with brands or a debit card (no longer around, it seems) and a rumored upcoming card from insurer Nibbles (see the fine print in the footer for clues).

I do not have a Wells Fargo card, but this might be the one that drives me over the line. Let’s just say that my family spends a lot on pets and a lot on self-care. I was a massive user of Ness, and while Attune doesn’t appear to provide bonus rewards in healthcare, it has everything from salons to tattoo shops to florists, sewing stores, golf courses, bookstores (Amazon), and pet care. Wow. Sign me up.

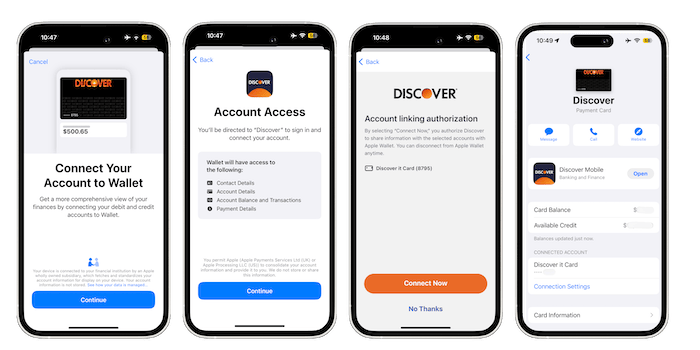

Apple Wallet Enhancements

On Monday at its annual developer conference Apple launched two new payments features for iOS 18: peer-to-peer Tap to Pay and enhanced wallet data. I was planning to cover wallet data–I had noticed last week a feature promoted in Wallet (on iOS 17) that enabled a link between my Apple Wallet and my Discover card, so I could see basic card info directly in the Apple Wallet Screens.

The first iteration of iOS 17 simply showed the balance and available credit. Promised in iOS 18 is the ability to view rewards and redeem them as well. These are great steps on the path from a wallet to a truly smart wallet. I am curious to see which issuers play along. I would also caution savvy users not to redeem points at purchase. Although networks and issuers have been pushing this for a while (you can do this in Amazon checkout, for example), it is usually a sub-optimal way to use points.

Apple’s peer-to-peer Tap to Pay allows users with Apple Cash Card (issued by Green Dot Bank) to transfer money directly to one another with a tap. Anecdotally, Apple Cash peer-to-peer is a distant fourth to Venmo, Cash App, and Zelle for peer-to-peer payments. The ease of use should help, but displacing the top providers will be a challenge.

Visa DPS + LoanPro

On the nerdier infrastructure side of things, LoanPro announced an integration with Visa DPS to create a new credit card issuing platform option this past week. With the failure of banking-as-a-service provider Synapse, a lot of attention has been paid over the past few weeks to ledgers and their capabilities. Many processors do not natively do revolving credit cards well because their ledgers aren’t capable enough–they are only able to do debit or charge (wherein there are no interest calculations).

Many fintech startups over the years have taken a path to stitch together credit by connecting a processor (such as Galileo or DPS) to a credit ledger/loan management system (such as LoanPro, Canopy, or Peach). Generally speaking, I do not recommend this. There are always integration and reconciliation problems. The best platforms have integrated credit ledgers. Some of the modern processors do this, such as CoreCard and Highnote, while most traditional processors handle this as well (think FIS, TSYS, Fiserv).

A press release doesn’t tell you much about how deep this integration is, but it is an interesting note about a traditional prepaid and debit-only platform (DPS) moving into credit and further proof of my long-standing position that the 2020s are the decade of credit innovation, following the 2010s decade of debit innovation.

I am skeptical that it’s as simple as “now you can issue credit at DPS.” There are many other capabilities needed to issue a credit card. For a full read, you can check out our market report on this.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.