Levels of Data - CardsFTW #111

Plus, I’m Not Writing About Bilt Again, More Apple Pay

The card industry news cycle is leaving me with a deep feeling of déjà vu. It’s getting a bit boring.

This week, I’ve decided to shake things up by discussing what I won’t be covering:

- Bilt: Skip my rant and head over to the Wall Street Journal article. Spoiler alert: Everyone in the industry already knew the Bilt card had unsustainable economics.

- Apple’s payment moves. You should catch up on the latest with Frank Young’s guest post on the Noyes Payment Blog about eCom and Apple.

- The end of Apple Pay Later: Or whether BNPL on credit cards and BNPL programs with credit cards are different things anymore. Honestly, it's all blurring together.

- Visa Flexible credential: I considered writing about it but decided against it. However, I did get a few good quotes at NerdWallet in What Visa’s Upcoming Changes Might Mean for Your Wallet.

- Visa/Mastercard settlement: Likely to get thrown out. So much for CardsFTW #99.

Data, Data, Data

For CardFTW #111, which feels like a special edition, I want to write about data levels. I considered waiting for CardsFTW #1-2-3, but I can’t wait three more months to discuss Level 3 data (yes, this is a dad joke—it was just Father’s Day).

Most consumers probably don’t realize what payment data levels are, but they’ve probably experienced some frustration at one time or another by being unable to access receipt-level data on their card statements. Today, we will explain why this is the case and how the network offers financial incentives to merchants to provide this data.

Before diving in, Let’s start with some definitions.

Level 1 Data

Level 1 data provides the most basic information required to process a transaction. This includes:

- Total payment amount

- Date and time of the transaction

- Card number (or token)

- Card expiry date

- Card security value (CVV)

- ZIP code (sometimes)

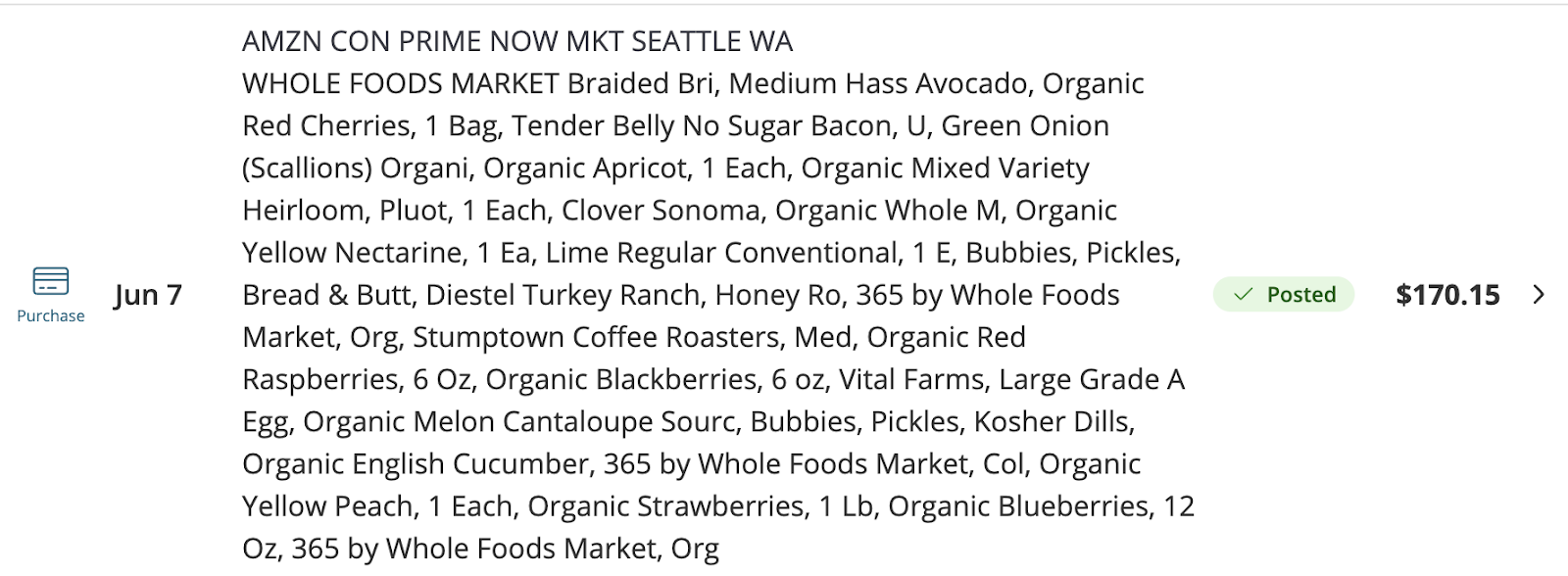

For consumers, this information is similar to that seen on card statements: transaction date, merchant name, and amount. For instance, your statement might show that you spent $612.45 at Best Buy on a certain date, but it won’t specify what items you purchased. To get details about the items, you would need to keep your receipt or contact the store directly.

Level 2 Data

Level 2 data includes everything from Level 1 plus a few other fields, primarily tax information. Consumer cards don’t support Level 2 or Level 3 data; these levels are reserved for commercial, business, or government cards. Building on our example above, with Level 2 data, you would know that you spent $612.45 at Best Buy, which was $551.21 on merchandise and $61.24 on taxes.

Level 3 Data

Level 3 data is the maximal set of data that payment networks accept today, including everything in Level 1 and Level 2, plus item or SKU (stock-keeping unit) level details. So, back to the Best Buy example, you would know that you spent $612.45, which was $501.22 for a TV and $49.99 for a TV mount (for a total of $551.21 on merchandise), and $61.24 on taxes.

A Note About American Express

American Express runs a three-party network (where the bank and network are the same, unlike Visa and Mastercard, which are separate entities). In the AMEX network, consumer cards can carry additional data on certain transactions, such as airline transactions and restaurant purchases.

What Higher Data Levels Get You

When merchants provide Level 2 and Level 3 data on business, commercial, or government card transactions, the payment networks provide financial incentives by reducing the overall cost of card acceptance. Merchants can save up to 80 bps by providing full Level 3 data. Commercial cards are expensive to accept so these savings are meaningful. Networks state that increased data levels reduce fraud (on both sides) as more information makes it easier to detect. The networks and their issuers also benefit from additional data insights about what customers are purchasing.

The Level 3 Dream

Throughout my career, I have met many entrepreneurs who ask, “Wouldn’t it be cool if my credit card had all the data about my purchases?” (By which they mean Level 3 data.) Yes, that would be cool. Folks are working on this, like the team at Banyan, which offers a privacy-forward platform to enable merchants, banks, and other middleware platforms an opportunity to find and match receipt data (with SKUs) to card data and enhance information to support card-linked marketing, reduce fraud, and ease expense management.

There are competing interests around Level 3 data, however, that make a universal solution very hard to achieve:

- Consumers may not want their bank to know what they are buying (would certain SKUs get your account flagged, closed, or suspended?)

- Merchants may not want their data used by aggregated data sources for competitive intelligence reasons.

- Banks may…while I don’t know why banks wouldn’t want all this data, they have the most to gain.

People have also attempted solutions using receipt scanning. Motivated savings-driven shoppers will take the time to do this type of work; see the success of recently publicly listed iBotta, which uses receipt scanning to issue SKU-level discounts.

I spent a lot of time researching card-linked marketing while at Wallaby and Bankrate, joining the CardLinx association, and attempting to find a way to align interests with the user at its center. It didn’t work for me, and I’m not clear if CardLinx is much of a thing anymore.

As a user, I would love to have all my receipts and transactions tied together. Many of us buy many things from Amazon, but they won’t even email your receipt details anymore because inbox data scraping led to data brokers selling pricing information. Pricing and information are power, and large companies like Amazon and Walmart want to keep those private. In the physical world, legions of mystery shoppers gather pricing data all the time.

However, if I have an Amazon private label credit card (issued by Synchrony), I can see a form of Level 3 data natively in my credit card statement (items, but not cost per item).

As merchants of all kinds become savvier about payment costs, enhanced data offers both opportunities and challenges. For merchants, providing Level 2 and Level 3 data can mean cost savings and fraud prevention. As with all things, there is no such thing as a free lunch, and the savings on Level 3 data could create a cost in data privacy (for all involved).

I don't foresee the dream of universally accessible Level 3 data coming to pass anytime soon, but it is something I hope more merchants will consider. Just think about all those cardholders living in the dark ages of Level 1 data, blissfully unaware of the treasure trove of details just out of reach, who would never have to dig through crumpled receipts again to remember what they bought.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.