Should You Use Rewards at Check Out - CardsFTW #112

Plus, I love intelligent card security

PayPal Introduces More Rewards Options

Recently, I sent some money to my sibling the good old-fashioned way through PayPal (peer-to-peer). Normally, this wouldn’t be my preferred P2P option, but the money I sent needed to go overseas to a cousin. While logged in, I was prompted to purchase items directly from PayPal using my Bank of America card rewards.

PayPal’s Pay With Rewards page lists many issuers (US Bank, Wells Fargo, uChoose Rewards, Bank of America, American Express, ScoreCard, CapitalOne, Chase, Discover, Citi, Elan, and US Bank). The feature also includes split tender, allowing users to pay part of their bill with rewards points and the rest with cash.

Pay with rewards is quite the talk lately. While Mastercard first announced its Pay with Rewards Program back in 2015, I have noticed many more checkout platforms and banks alike talking about it. For example, you can use rewards when checking out at Amazon, including rewards from major card issuers like Capital One, Chase, Discover, and American Express, as well as Amazon’s own private label card rewards program.

But should you use your rewards to pay? If you don't carry a balance on your card and pay it in full each month, using rewards points for purchases is typically not a great option. Converting rewards points to cash through points-for-goods often yields a lower value per point. For example, American Express Membership Rewards points typically have a value of 0.6 cents (that is $0.006) per point when redeemed for cash at checkout or for goods in the Amex rewards store. On the other end of the spectrum, transferring American Express points to Delta SkyMiles or other airmiles or hotel programs might net you 1.7 to 2.2 cents in value.

For the most part, the days of extremely high-value wins (like 5, 6, or 7 cents in value per point) are over, as programs have tightened up their redemption programs and shifted to fixed-value programs. However, a reward maximizer would say never use points for check out rewards.

So, why do programs do this?

It must be that consumers tell them both in surveys and in behaviors that they like it. Most consumers, especially folks not reading this industry newsletter, are not trying to maximize every last point. Everyone wants to be a smart consumer, but managing your cards carefully can feel like a full-time job. The average consumer has a busy life and doesn’t want to expend too much mental effort on this.

The psychology of reward points creates the feeling of using free money when redeemed. As the saying goes, “You can’t lose money, making money.” When you use reward points, you use free value earned through your card program. You may not get the highest value, but you are getting something.

As I covered in CardsFTW #98: The Economics of Points, programs depend on a variety of behaviors. If every cardholder maximized to the fullest extent mathematically, then the programs would have to adjust and pay less overall. Put more bluntly, the less savvy users enable higher values for savvier ones.

One final note on this: I assume that people are happy with the way they redeem their own points–no one is forcing them to redeem them. So, while you (or I) might never use our points at checkout at Amazon, for someone else, the economic utility (e.g., happiness or net value) to that person may be very high or higher than other options. If I hate to travel but can use my points to get a free iPad that I really want but don’t feel like I can spend cash on, then that’s a good deal for me.

Checkout Security

American consumers encounter out-of-band card security less frequently than those in other regions. In Europe, systems like 3-D Secure (3DS) and PDS2.0/SCA/3DS2.0 are commonly used to authenticate card users through alternative methods. However, as security measures increase, Americans are becoming more familiar with multi-factor authentication. A common example is logging into Gmail with a password and then entering a six-digit code sent via SMS (although this method is not very secure).

With 3DS enabled, the card issuer can prompt the merchant checkout process to ask users to validate more than just their card number (PAN or Primary Account Number), Expiration Date, security code (CVC/CCV), and billing ZIP code. The most frequent way users experience this is a pop-up web window wherein they must also log in to their bank account to authorize the transaction.

This process creates two factors - one thing you have (e.g., your PAN) and one thing you know (e.g., your bank account password). Plus, if your bank requires MFA to log in, you can get another layer.

Once a card transaction is verified via 3DS, the liability shifts to the bank if the charge is fraudulent, and the transaction can go through. All this creates checkout friction, so many retailers do the math and determine that bearing some fraud risk is less expensive than the drop-off in conversion from the 3DS process.

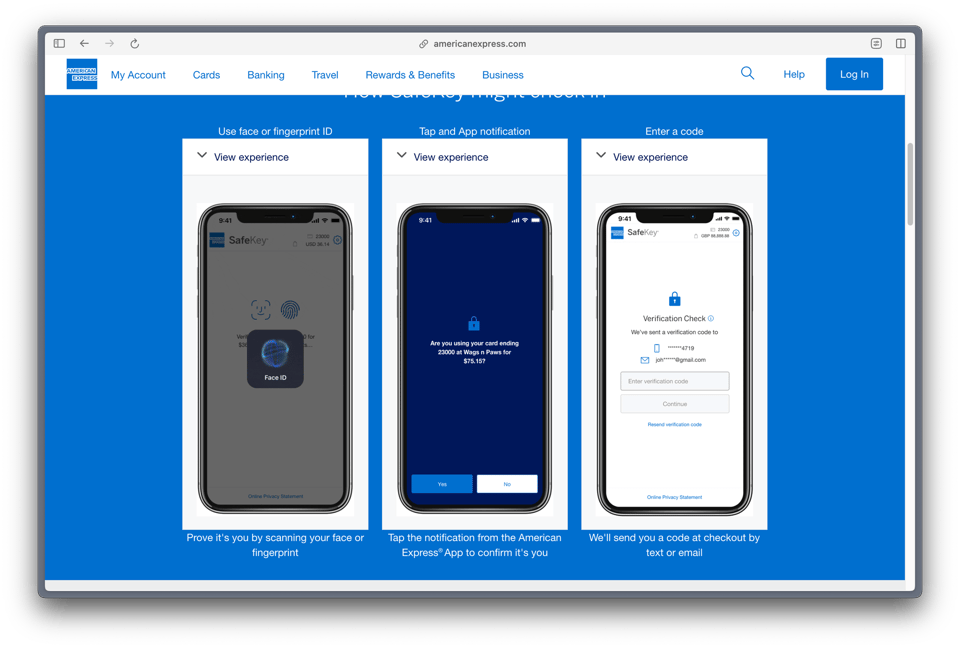

The other day, I experienced a really smooth 3DS process with my American Express card. Amex had named this SafeKey. There are a few different experiences, but on mobile, Amex will send you a notification via the AMEX app to verify the transaction, FaceID you, and then let the merchant know the transaction is complete. It was super easy and fast. I anticipate that users will see more and more 3DS2 in the coming months and years, and the whole industry will benefit from it.

New Huntington Business Card

Huntington Bank, America’s 25th largest bank (as of the end of 2023) that happens to be super regional, announced a new aggressive business card offering: The Voice Business Credit Card. The card earns 4% cashback on up to $7,000 per quarter in one of ten categories the user chooses. Cards with user-selectable categories allow a bank to have one product with many options and create flexibility.

Huntington doesn’t issue cards outside its footprint, and you need to apply in branch (and likely have a business banking relationship), but this is a great offer if this applies to you. The category list is really interesting, with both some very typical ones and some rare ones:

- Auto Parts & Service

- Department, Apparel, and Sporting Goods

- Discount and Warehouse

- Electronic, Computer, and Camera

- Gas Stations

- Grocery Stores

- Home Improvement

- Restaurants

- Travel and Entertainment

- Utilities and Office Supply Stores

Some of these feel like consumer categories (looking at you, restaurants and grocery stores), but a category like Auto is a rare one. Plus it looks super valuable for businesses with fleets, such as your local service providers. The card has no annual fee, employee cards and spend controls and no foreign exchange fees. It’s a very strong offering.

Marriott + Starbucks

OK, this story isn’t explicitly about a card, but both Marriott and Starbucks have huge loyalty programs, and the Marriott co-brand card portfolio, which lives across both Chase and American Express, is one of the largest co-brand portfolios in the world, so it feels on topic. Starbucks has been battling lower sales with discounts and other approaches of late. For a few years, they have had a tie-up with Delta, with extra earnings on travel days. (The Delta program just got a refresh with both double “stars” or Starbucks loyalty points on days you travel, plus Delta miles every time you reload at least $25 to your account.)

Last week, Starbucks and Marriott announced their partnership, with double stars through the duration of your stay at hotels participating in Marriott Bonvoy and 100 points during a “Marriott Bonvoy Week” when you go to Starbucks at least three times. What the heck is a Bonvoy Week? Well, it seems to be a made-up holiday. The first one is July 8th - 14th, so we’re about to find out.

Ironically, I was staying at a Marriott the day this was announced, but I failed to go to Starbucks, so no double points for me.

To me, the most interesting thing about the Delta and Marriott plus Starbucks programs is the development of multi-loyalty bonuses. In other countries, like Canada, complex multi-earning programs like Airmiles exist, bringing together all sorts of retailers. Folks have tried that here, most recently, to my memory, with Plenti from American Express, which lasted only three years and closed shop in 2018.

Building a new points program across retailers, like Plenti, from the ground up might be too hard. However, taking multiple well-loved (or at least ubiquitous) brands like Starbucks, Delta, and Marriott and putting them together may work a lot better. We also see this in the ride-sharing space, such as by taking a Lyft can earn you Delta SkyMiles (2x if it’s an airport trip). Consumers love to double dip by stacking coupons or earning rewards twice. Earning a credit card point, plus a Marriott point, plus a Starbucks point, all on the same dollar, is triple-dipping and feels good. Feeling good drives brand loyalty, which is what this is all about.

I’m looking forward to more of these deals and seeing the innovations brand leaders develop.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.