Private Label Cards - CardsFTW #120

Plus, Ongoing Point Devaluations and What Happens to Points and Miles in a Divorce?

Normally, CardsFTW, as a newsletter, covers many co-brand cards, which have multiple brands attached to them: a retailer brand, a bank brand, and a network brand like Visa, American Express, or Mastercard. However, there is a huge volume of private label credit cards in the United States, which are issued by retailers with a bank but without a network or payment scheme brand like Visa, Mastercard, American Express, or Discover.

A common example is Macy's: Macy's has both a private label card and a co-brand card, the latter being with American Express as the network. Another modern example is Amazon. Amazon has a relatively famous credit card with Chase, the Amazon Visa, but they also have a private label card powered by Synchrony Financial, which can only be used at Amazon.

Traditionally, retailers built private label cards before network schemes existed because it was the form of in-store credit, just like at a small department store. I grew up in a small town where, even in the 1980s, they still had a credit department. I could walk in, buy a piece of clothing, and charge it to my family's account. At the end of the month, a letter would be sent with the total amount owed, which my parents would then pay. (Thanks, Dad, for doing that!)

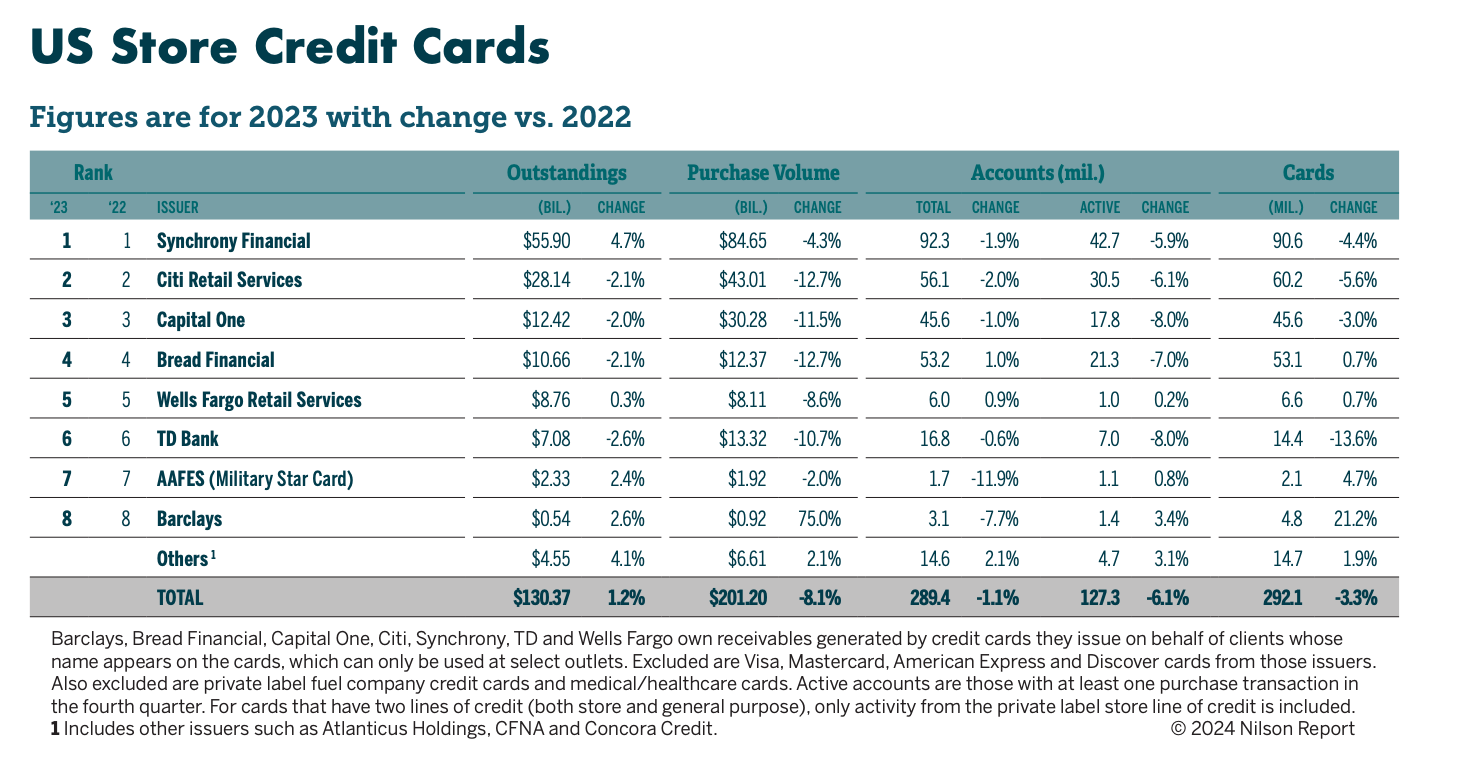

Larger retailers eventually migrated these to membership cards to keep track of customers across multiple locations. This led to the birth of the full open-loop credit card, which can be used at any store that accepts Visa, Mastercard, or Amex. In 2023, 292.1 million private-label store credit cards were in circulation in the United States, which generated $201.20 billion - showing just how common they are.1 One of the key functions of private label cards was to differentiate between creditworthiness. If a retailer gave someone a $1,000 credit limit to spend anywhere, the retailer might be partially responsible for credit losses. If that person didn't pay their bill after spending at another store, the retailer could be on the hook.

With private label cards, the retailer has more control. For one, they control authorization, and it's easier to know whether a card is valid or stolen, especially before modern real-time authorization. Also, if someone spends $1,000 and doesn't pay at least the goods were purchased from the retailer, which may lessen the financial impact since the store profited from those goods. There was a time when dynamic pricing and underwriting didn't exist, but Capital One revolutionized this in the 1990s by segregating users and card types more clearly.

If you're Macy's, for example, and want to give anyone who walks in a payment card, you could offer a Macy's store-branded private label card with a $200 credit limit, which is low-risk. For customers with higher credit scores and income, Macy's could offer an American Express-branded card with a $2,000 limit. This stratification creates a hierarchy: private label cards at the bottom, no-fee Visa cards, and higher-end cards like Visa Signature or Mastercard World.

In today's world, this makes less sense because we now have dynamic pricing. You can adjust credit limits and APRs across credit tiers. Private label cards often had the highest APRs, sometimes as high as 29.99%, and APRs would decrease as creditworthiness increased. It's more common to see variable pricing within a single product, where a person with good credit might get an APR of 9.99%, while someone with lower credit might get 29.99%.

I've had some interesting conversations with traditional mall retailers who don't offer co-branded cards. For them, it's about building loyalty and returning customers to their store. Only a few companies do private label cards on a large scale. Two major players are Synchrony, which used to be GE Money, and Bread Financial (formerly Alliance Data Systems). Some new entrants, like Tandym, focus on private label credit for e-commerce. Synchrony is still the largest provider of private-label store credit cards in the US.1

When I talk to retailers, my question often is: Why stick with private branding? One thing I hear is that they're trying to keep loyal customers happy by offering financing. Retailers like Victoria's Secret and Express used to have private label cards. I challenge these companies to consider adding a branded card because it's easier to do now and opens up more possibilities.

Providers like Imprint and Cardless are examples of this shift. Imprint, for instance, offers a Brooks Brothers card, and Cardless has partnerships with smaller airlines and Simon Malls. In the past, retailers may have thought it wasn't worth the effort to build these programs, but now they can have both private-label and co-branded cards.

Interestingly, some of these modern providers don't offer non-network-branded cards because they rely on the interchange from off-store spending. But I think we'll see private label providers expand beyond e-commerce and into physical retail. It might be easier than it seems, especially with mobile wallets and digital solutions.

Traditional retailers also have an untapped opportunity to rethink private label programs. Some mall retailers using Synchrony or Bread are actually much larger than many fintech programs. I don't think many fintechs today have programs running over $100 billion in receivables, but many mall retailers do. So, there's a huge opportunity to disrupt the private label market and help these traditional retailers modernize their offerings.

Quick Hits

The Virgin Red Rewards Mastercard, which was teased a few months ago (see CardsFTW #108), is getting closer with the launch of a waitlist and key details on the card. Virgin is interesting because it's hotel, airline, and cruise brands all together (which we don't normally see). As a limitation, though, for US customers, there are not a lot of Virgin flights, hotels, or cruises to take. The card carries a decent signup bonus (40,000 points), 3 points per dollar at Virgin Atlantic, Virgin Voyages, and Virgin Hotels, 2 points on grocery, dining, streaming, and EV charging, and 1 point everywhere, all for a $99 annual fee. Big spenders (over $15K) will have access to custom perks like a companion pass or cabin upgrade, a free night, or a bar credit on a cruise.

Best Western's Mastercard, issued by First National Bank of Omaha, appears to have been pulled from the market for new cardholders according to Nerdwallet. No details are forthcoming from the hotel brand or the bank. We hear less about mid-tier chains, which struggle with spending levels and consumer approvability, than we do about larger or more premier brands like Hilton, Hyatt, and others.

The Wall Street Journal is pointing out that loyalty programs are losing value. This has been happening for a while; first, it was airlines, and now it's hotels. International airlines and such do really well for points programs, but the devaluation will not stop.

Bilt announced a new partnership with Walgreens this week to enhance FSA spending. The partnership, powered by Banyan, is a noteworthy addition as Bilt continues to work on differentiating its program and finding new ways to drive non-rent spending to Bilt cards. By integrating FSA eligibility SKU-level data, the feature helps to make it easier for users to identify and manage their FSA-eligible purchases. It will be interesting to see if this approach resonates with consumers who are looking for more practical benefits in their credit card choices.

The Washington Post covered the economics of points in divorces - and death. When it comes to divorce, points are considered joint assets that must be divided just as any other community property, with the extra complexity of varying policies and fees for transferring rewards. They also make the case that if you have a significant amount of points or miles, determining what will happen with them upon your death is often overlooked. The article underscores the importance of understanding the value and rules governing these points and programs to ensure they are fairly distributed in legal and financial planning.

Me, Elsewhere

Last week, I participated in a webinar on the future of credit card rewards and loyalty presented by NYPAY.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.

1. Nilson Report, July 2024, Issue 1268, 14↩︎