Streaming Deals - CardsFTW #124

Plus, New Best Western Cards, Bilt for Mortgage, and More

I’ve noticed a recent trend of credit cards offering more benefits around streaming services. Maybe it’s because people love entertainment, or perhaps it’s due to the growing frustration with subscription services. Either way, I want to explore this topic further.

We’ve moved from a world where people spent $50 to $150 on a single provider like DirecTV or Charter to one where they’re juggling multiple streaming services like Netflix, Peacock, HBO, and more. As card issuers try to justify the high annual fees of premium credit cards, they increasingly showcase their value through discounts or freebies for streaming services.

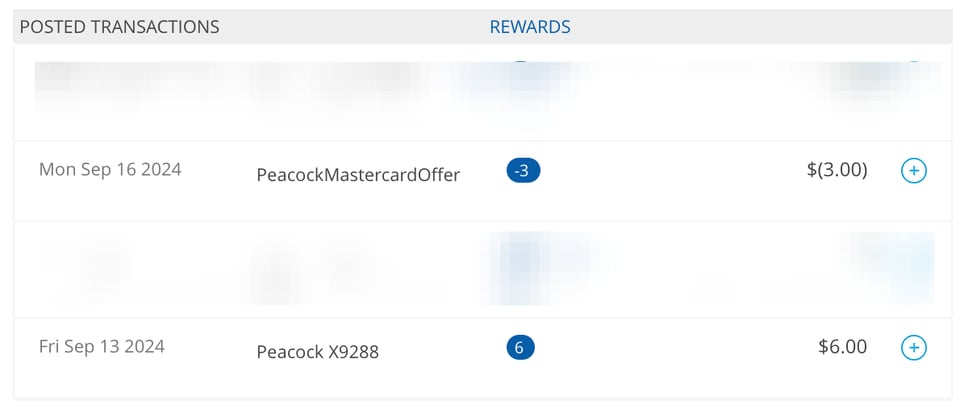

One recent benefit I discovered is that all World Elite Mastercard cards now offer discounts on Peacock TV. While Peacock isn’t quite on par with Netflix, the discount of three or six dollars off, depending on your chosen plan, is a nice perk. This benefit is available at the Mastercard network level, meaning any World Elite card can access it. I tested this on my Hawaiian Airlines World Elite card, and it worked seamlessly.

Other card programs have introduced more complicated offerings. For example, the Amex Platinum card, which costs $700 annually, includes a free Walmart+ membership, which is valued at $13 per month. That adds up to a decent value ($156 annually), although I wonder how much overlap exists between Amex Platinum cardholders and Walmart shoppers, but that’s another discussion. Walmart+ also provides access to Paramount+, though it’s the ad-supported version. Paramount+ is $7.99, so if you stack these perks you’re up to $251.88 per year, but you have to take a few hops to get there.

It’s interesting to see how credit cards are leaning into streaming service benefits because these are services people use daily. We’re also seeing more cards offering general rewards for streaming. For example, the Amex Blue Cash Preferred offers 6% cash back on streaming services charged directly to the card.

However, there are situations where benefits don’t stack. Take the Chase Sapphire Reserve, which includes a complimentary DoorDash DashPass membership. DashPass gives you access to Max (formerly HBO Max) as part of its premium offering, but Chase’s version doesn’t include HBO. It’s all a bit confusing.

I’m curious to see if any card issuer will strike a deal that lets consumers bundle all these streaming services into one package as part of the annual fee, perhaps creating an “entertainment card” that’s been difficult to execute effectively in the past. Other forms of entertainment, like bookstores or movie theaters, can also qualify for rewards on some rotating quarterly cards, and people find those valuable.

Overall, it’s a space worth watching to see how credit cards, the ubiquitous financial product, continue to intersect with streaming services, the ubiquitous entertainment product.

New Best Western Cards

Last week, Best Western announced two new card products in partnership with Mercury Financial. As a refresher, Mercury Financial (not the other Mercury) has historically focused on subprime offerings. This partnership is particularly interesting because Mercury has never really played in the travel rewards space before, let alone a prime offering.

The Best Western Rewards® Premium Visa Signature® Card comes with an $89 annual fee and a 80,000-point sign-up bonus with qualifying spend. It offers 10x points on stays and purchases at participating Best Western properties, 4x points on gas and groceries, and 2x points on everything else. It also provides a free night award each year on your account anniversary and another free night after $10,000 in annual spending. To top it off, cardholders get automatic Platinum Elite status, which includes perks like room upgrades and late check-out.

For those who prefer a no-fee option, there’s the Best Western Rewards® Visa Signature® Card. This card offers up to 40,000 bonus points with qualifying spend, 4x points on stays and purchases at participating Best Western properties, and 2x points on all other purchases. You’ll also earn an extra 10,000 points after spending $5,000 annually and receive automatic Gold Elite status, which still comes with some decent perks.

Walmart Still Hates Cards

Walmart has always had a bit of an aversion to credit cards. They’re one of the few massive chains that didn’t immediately jump on the Apple, Google, and Samsung digital wallet bandwagon. Instead, they launched their own solution, Walmart Pay. This move allowed them to sidestep some of the costs and complexities with the networks but made it more difficult for consumers to use their preferred payment methods. Walmart has historically negotiated directly with the card networks to secure lower interchange rates, using their size and scale to get a better deal. And now, they’re taking another step to reduce their reliance on cards altogether.

Last week Bloomberg announced that Walmart is launching instant bank payments, effectively cutting out card networks from the equation. For a retailer as large as Walmart, this is a big deal. They’ve recognized that cards, while convenient, are an expensive way to process payments, especially at their scale.

This isn’t entirely a new concept, though. Target has been doing something similar for years with their RedCard debit product, which connects directly to customers’ bank accounts. But Walmart’s scale and influence could make this a much bigger deal. They’ve always been about offering lower prices and squeezing out inefficiencies. Cutting out the middleman, whether that’s card networks or third-party digital wallets, fits right into their playbook.

For customers, this could mean more seamless and potentially faster payments. For Walmart, it’s a way to gain even more control over their payment ecosystem and reduce the fees they pay to card issuers and networks. It’ll be interesting to see how this move plays out, not just for Walmart, but for the broader retail and payments landscape. If other major retailers follow suit, we could be looking at a significant shift in how we pay for things.

Quick Notes

- DOJ sues Visa: People think Visa’s tax on the economy is too high. That’s not news, but the DOJ suing them is. More from the NY Times here.

- Cashback on your mortgage: Mesa announced their launch, saying they will offer cashback on your mortgage every month. Issued by Celtic Bank, the card has a waiting list (I’m number 8550! ) I don’t get the economics here, especially with a reported 20-22% APR. In the current environment, it would be hard to make money

- More ways to redeem: Ascenda and Uber announced their partnership. If you’re a bank or fintech that partners with Ascenda, your cardholders will now be able to redeem their reward points directly for Uber credits.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.