Understanding FBOs in Fintech - CardsFTW #123

Plus, is JPMorgan taking over the Apple card?

There's been a lot of news lately about how fintech card programs work, pass-through FDIC insurance, and the downfall of Synapse and Evolve programs. It's more important than ever to understand how FBOs work. So, how did we get here and what the heck is an FBO?

What's an FBO and Why Does It Matter?

FBOs, or "For Benefit Of" accounts, are a fundamental structure in many fintech operations. They're the bridge between traditional banking systems and fintech services. FBOs matter because they allow fintechs to manage large numbers of customer accounts efficiently and enable pass-through FDIC insurance in certain scenarios. They're also at the center of recent controversies in the industry.

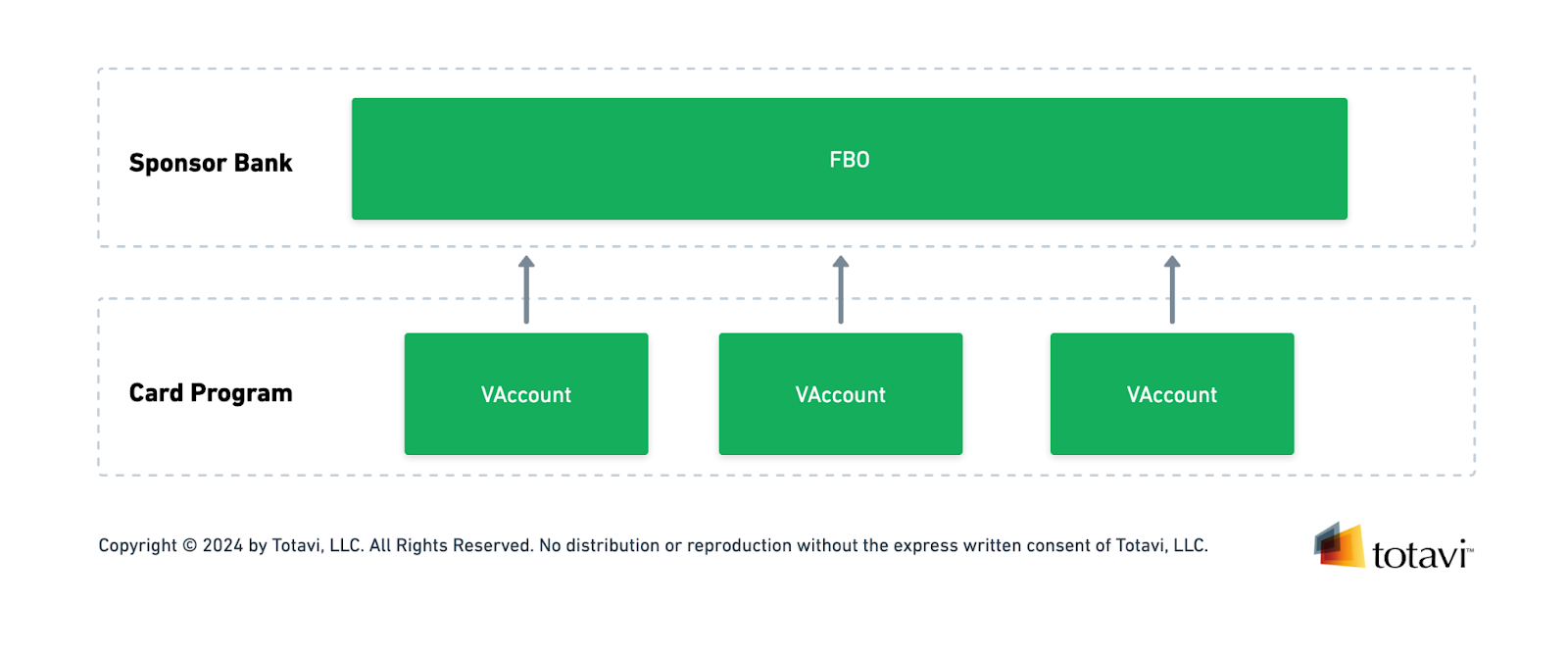

Fintech programs have traditionally worked on what is called a virtual account (vaccount) basis. This doesn't mean the accounts aren’t real, but they’re not on the core system that banks use to track money. The bank's core or operating ledger comes from services like FIS, Fiserv, Jack Henry, and other traditional providers, as well as newer ones like Temenos. That's where your account is. If you walk into a Bank of America, open an account, get an account number, and transact into and out of that account, it's all on that core. The banks usually pay a fee for every account, making them somewhat expensive for banks to manage on a per-account basis.

Now, enter fintech programs that want to do new and interesting things and not be constrained by the bank's core. Their solution? The FBO account.

How FBOs Work

An FBO is essentially one big account that holds money for all of a fintech program’s users. Sometimes, they're also called omnibus accounts because they hold everything (which is what omnibus means).