PayPal Goes Big - CardsFTW #122

Plus, Robinhood Gold Card in the Wild and New Cards from Alibaba and US Bank

PayPal Goes Big…on Marketing

PayPal announced its largest US marketing campaign ever starring Will Ferrell. You probably saw this ad if you watched any live TV this weekend (and I watched a lot between the US Open and the NFL). The new ad campaign ties in with the announcement of a product called “PayPal Everywhere.”

As far as I understand, PayPal is pitching a deeper integration of the shopping discounts it brought in-house with its blockbuster 2019 $4B purchase of Honey, the pioneer of browser-based shopping tools. Paypal says that the new rewards program allows customers to choose a category of spending on which to earn up to 5% cashback (up to $1K per month) when they use their PayPal Debit Mastercard to purchase and to stack those rewards with other merchant offers.

OK, if this is easier, that’s nice. But also, it is already true that you can stack offers. I can stack my baseline Amex Platinum earnings with my Amex Offers bonus. I can also sometimes stack it with a cashback boost or rewards from Rakuten or another shopping site. The card-linked marketing industry has long tried to limit stacking and multiple rewards uses (because merchants might want to pay 10% but not 20%), but they are not great at it, to be frank. I get double-dipped rewards all of the time. Optimizing for maximum card rewards and other bonuses is an entire sub-culture with subreddits and tools, like Kudos.*

PayPal is also making a big deal out of the fact that you can use tap-to-pay (Apple or Google) at the point of sale. This isn’t news, though; this functionality was launched in 2022.

I’m curious to see how the new full circle approach goes. Few customers want to keep a balance in their PayPal account debit card when they could use another card, but from a consumer standpoint, the brand needs to find a way to break out of the online purchase category.

Consumer announcements weren’t the only thing PayPal had last week, either. They also announced that PayPal’s merchant processing platform will process some Shopify payments, which takes some volume from Shopify. Individual consumers won’t notice this, but it is a meaningful change for Shopify.

Robinhood Gold

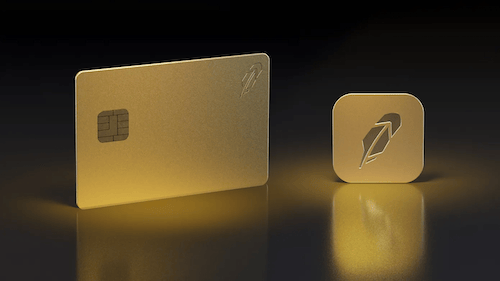

Reports have started of people getting the new Robinhood Gold card we touched on in CardsFTW #99. They really are sending a gold card to people. Not me, yet, though. Why? Because I need more referrals to signup using my link. Help a card collector out.

It’s totally wild to me. The card itself is worth $1,200 in gold and must cost them something in that range to manufacture. I remember a decade ago a bank in the Middle East doing a gold card, but it created problems with gold’s connectivity shorting out readers on occasion. I guess that was fixed. Much like the Apple Card in Titanium, the Robinhood Gold is a card I suspect people won’t really carry that much but will keep as a trophy.

US Bank Launches New Smartly Card

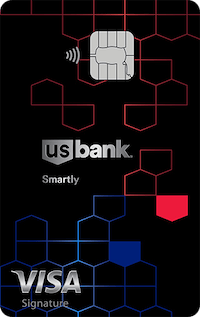

US Bank announced a waitlist for its new Smartly Visa Signature Card. Normally, I find waitlists a little annoying because they come from startups that never launch, but in this case, I’m sure US Bank will launch. The card is a really interesting offering that expands on the relationship bonuses that can drive deep bank relationships and manages to out-reward the Robinhood Gold Card (above, earning 3% cashback), with earnings up to 4% for cardholders with qualifying balances of at least $100,000.

Bank of America has long led the account bonuses program with its Preferred Rewards program. At BofA, when you have at least $100,000 in qualifying deposits you earn a 75% bonus on card cashback. You can earn 2.625% daily on the Bank of America Travel Rewards card and up to 5.25% cashback in your top selected category on the Customized Cash Rewards Card.

This US Bank offer starts with a 2% cashback baseline and grows through tiers of:

- 2.5% ($5,000 - $49,999)

- 3% ($50,000 - $99,999)

- 4% at $100,000 or more.

This card is smart(ly). I predict a wave of cashback seekers transferring an investment balance over to US Bank to get this. Is it sustainable? Who knows. I don’t think Robinhood’s is either, which requires a Gold Membership ($5 per month) to earn. They are both approaches on the relationship bonus structure. As banks continue to compete in a world of rewards seekers, but with a limited top-line income from interchange, these types of multi-product rewards make a ton of sense.

Alibaba Launches New Business Card

Alibaba, the Chinese shopping powerhouse, announced a new business card powered by Cardless* that is running on the Mastercard network. The Alibaba.com Business Edge Credit Card will be the company's first co-branded US credit card. Cardholders will have the option to earn either 3% cashback or a 60-day interest-free period on purchases, providing flexible earning and lending capabilities. Purchases not made on Alibaba earn 2% on business categories like advertising, dining, and more, and 1% everywhere else. The card carries a $199 annual fee.

This card reminds me of the Amex Plum Card. The Plum Card, with a $250 annual fee, offers businesses either 1.5% when charges are paid within 10 days of the closing date or 60 days to pay up to 90% of the balance. As a charge card, you cannot revolve balances past 60 days. I had a Plum Card for a business back in the early 2010s, and it was awesome to choose between needs as they changed.

The new Alibaba card is the first business card for Cardless and is a strong entry into the category.

Amex Ties the Knot with … Knot

Knot, the card-switcher API, announced a new deal with American Express to ease card switching for AMEX cardholders. Amex Ventures is also an investor in Knot. Knot makes it easy for customers to place or update the card on file at a particular merchant. Issuers love this because it drives spend (cardholders are more likely to use an already saved card than to switch). That said, I have a question about what happens once everyone has Knot. Does the last click win?

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.