Everybody Focus on Cards! - CardsFTW #192

Plus, Cards 101 and Infrastructure

Cards 101: (Almost) Everything You Need to Know About Payment Cards

Launching a credit or debit card can be complex, even for experienced fintech founders. Our free Cards 101 deck breaks down how card products work, the key players involved in every transaction, and the economics of running a card program. Whether you’re launching a new card product or looking to enter the card industry, this is a great starting point.

The Cost of Many Vendors

Marqeta released a report this morning about the cost of having multiple payment vendors, authored by yours truly. I spoke with executives of scaled fintech companies about their experiences switching providers (see also last week's CardsFTW #191: It’s the Dawning of the Age of Migration) or using multiple providers (e.g., one for credit, one for debit) and the associated costs.

Citi and BofA: We’re Focused on Cards

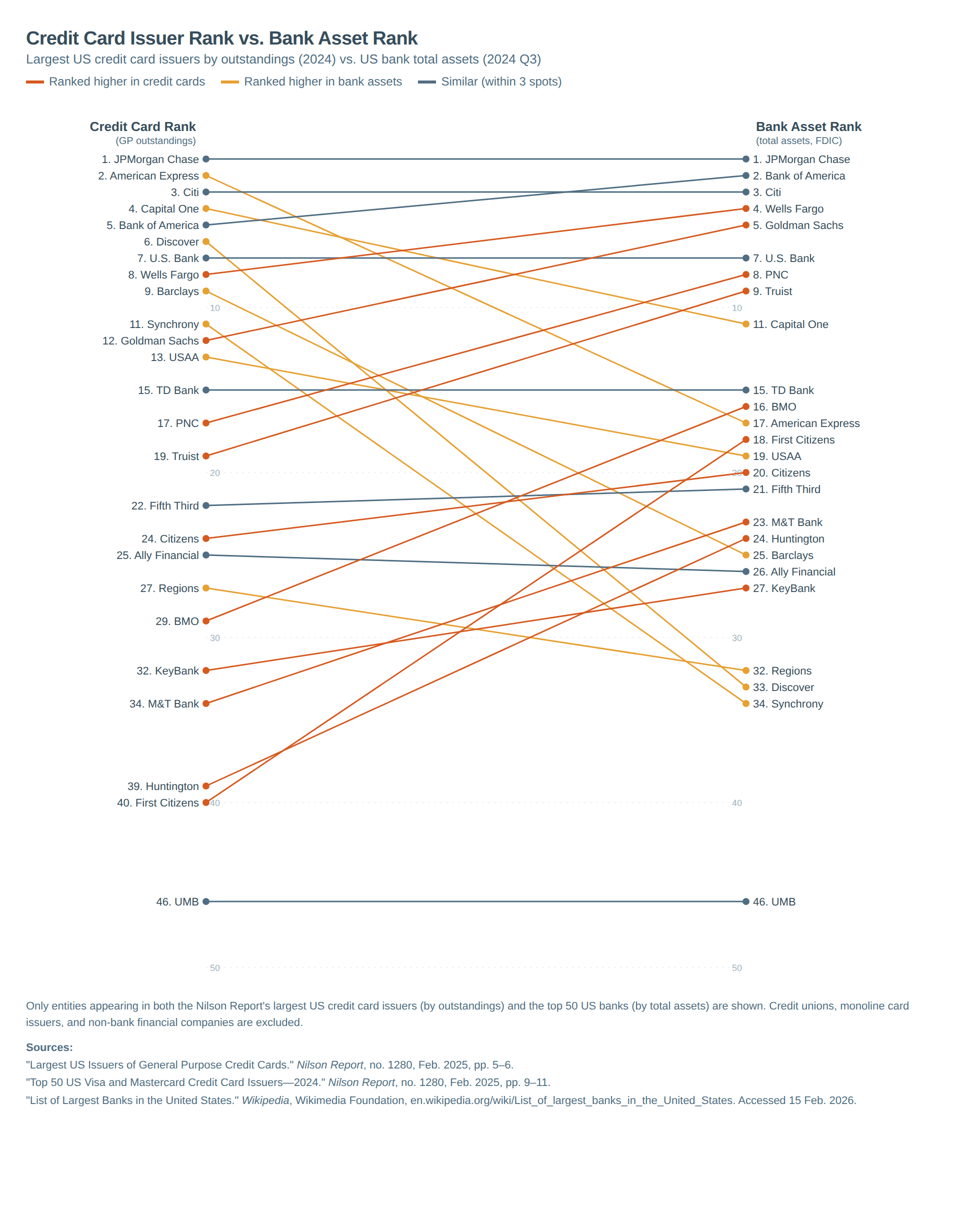

According to the Nilson Report Issue #1280, in 2024 (the latest year available), the top five U.S. general-purpose credit card issuers by transaction volume were:

- JP Morgan Chase: $1.344 trillion

- American Express: $1.168 trillion

- Citibank: $616 billion

- Capital One: $609 billion

- Bank of America: $502 billion

With the 2025 merger of Capital One and Discover, we can expect Capital One to leapfrog Citibank to the number three spot with somewhere around $828 billion in transactional volume. (Plus, JP Morgan will extend its lead when it takes on some $20-30 billion in Apple Card volume from Goldman Sachs.)

The gap between the top three and the next two issuers is growing. A combined Capital One/Discover will be 34% larger than Citibank. JP Morgan is already 15% larger than Amex and is likely to process almost three times the volume of Bank of America in 2025.

Credit Card Issuer Rank vs. Bank Asset Rank

Largest US credit card issuers by outstandings (2024) vs. US bank total assets (2024 Q3)

Only entities appearing in both the Nilson Report's largest US credit card issuers (by outstandings) and the top 50 US banks (by total assets) are shown. Credit unions, monoline card issuers, and non-bank financial companies are excluded.

"Largest US Issuers of General Purpose Credit Cards." Nilson Report, no. 1280, Feb. 2025, pp. 5–6.

"Top 50 US Visa and Mastercard Credit Card Issuers—2024." Nilson Report, no. 1280, Feb. 2025, pp. 9–11.

"List of Largest Banks in the United States." Wikipedia, Wikimedia Foundation, en.wikipedia.org/wiki/List_of_largest_banks_in_the_United_States. Accessed 15 Feb. 2026.

Credit cards are a game of scale: the more you process, the more efficient your systems can be, from pure processing infrastructure to data intelligence for underwriting. Chase is running away with the game.

Credit cards do make money, though, and a lot of it. Plus, they are a product that consumers are more likely to try when considering new relationships with new financial institutions. The average consumer has three to four credit cards, but one checking account. Moving your checking account is a big deal, but adding a credit card is not.

Against this backdrop, our expected fourth and fifth-place volume issuers in 2025 both recently announced a renewed focus on cards.

Speaking at the 2026 BofA Securities Financial Services Conference, Citibank’s Head of U.S. Personal Banking and Incoming Chief Financial Officer Gonzalo Luchetti, shared his thoughts on the launch of Citi Strata and its continued focus on cards. The bank has recently reorganized its card operations in its retail business, separating them from wealth management. A key note, which we’ve touched on here before, is the “blurring lines between the co-branded space and the private label space.”

[C]ustomers over the last few years [are] really choosing with their wallet to lean more towards general purpose cards. So whether the proprietary cards or the co-branded cards, the ones that you can use in any store. And so I think what you’re going to see from us, is us making investments and leaning in that direction, where the customers are taking us as we go forward.

Strata was a big investment, Costco is a huge investment, and here comes more.

On the Bank of America side, Bloomberg reported that BofA is “aiming to double the profit it makes from consumers” through revamping its approach to credit cards. BofA’s cards have typically been pedestrian over the last few years, although recent launches like the Atmos Summit card and Premium Travel Rewards card have shown a new desire to head into the ultra-premium space.

Bank of America has focused uniquely on relationship bonuses for its credit card business, offering rewards of 10%-75% based on the bank's assets. While Chase once did something like this, it has long since been discontinued.

I’d like to see both Citibank and BofA offer relationship bonuses to compete with larger issuers that may not see a need to do so. If they want to increase profitability, however, I imagine the #4 and #5 will not go all-in on high acquisition costs, although both have room for ultra-premium cards. Citi is well along this path with Strata (I heard the card looks amazing in person), but has had some public stumbles. (See CardsFTW #178: Citi Fumbles the Strata).

BofA, meanwhile, has never pushed a mass-affluent ultra-premium card. BofA’s top-tier Bank of America® Premium Rewards® Elite Credit Card (what a mouthful) is basically the same thing as their fee-free Bank of America® Unlimited Cash Rewards, except, you know, “lifestyle credits.” A lack of travel portal transfer partners and a subpar user experience will not earn BofA a top-tier spot.

Many large US consumer banks lag in card issuance due to the dominance of Chase and Amex. I don’t think they all want to invest in more cards, but they should be concerned that ceding the space will ultimately cost them longer-term clients and cross-sale opportunities.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.