United Demands Your Loyalty - CardsFTW #193

Plus, more on BofA rewards and merchant steering research

United Really Insists You Get a MileagePlus Card

It’s been 40 years since the debut of co-brand airline rewards credit cards. United Airlines Mileage Plus First Card (a Visa card issued by First Chicago Corp.) debuted in 1986. With an annual fee of $45 (waived for the first year), you received a $25 travel certificate for use on United or affiliate companies like Westin, Hilton, and Hertz.

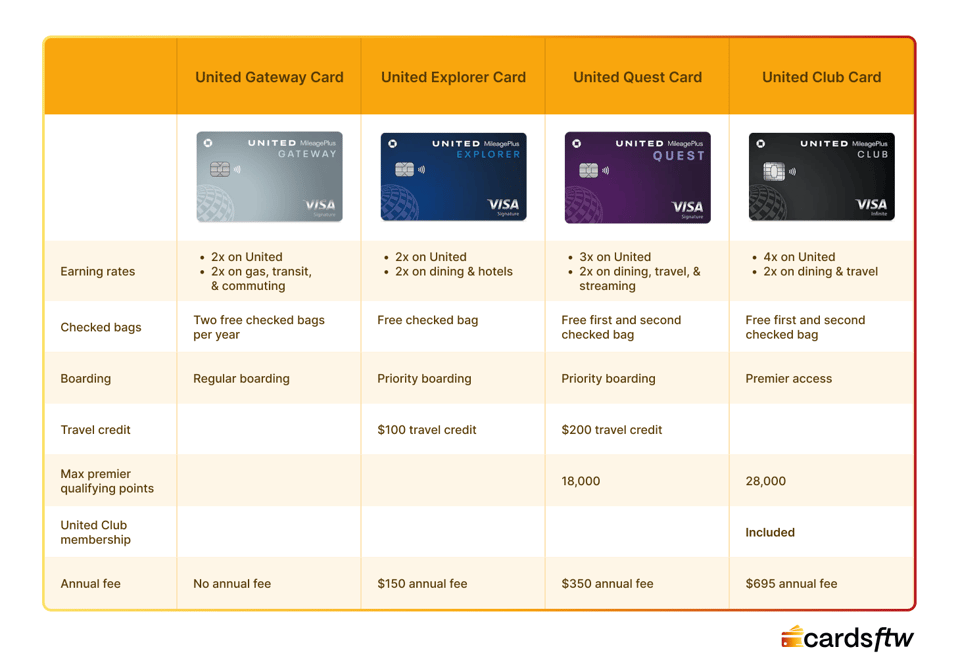

Today’s cards are both effectively the same and yet so much more complicated. For consumers United offers four credit cards, plus a debit card.

United no longer wants to simply incentivize you to get a card; they’re going to start punishing you for not having one. Instead of simplifying earning bonus points when you make flight purchases with your credit card, the actual mileage earning rates when you fly will vary based on both your status with the airline and whether or not you have a United co-brand card.

At its most basic level, with economy fares, non-cardholders won’t earn miles. At all. Cardmembers will earn 3 miles per dollar. For regular fares, non-cardholders will earn 3 miles per dollar and cardmembers will earn 6 miles. This 3 mile per dollar differential persists across all tiers of status (topping out at 12 miles per dollar for Premier 1K status cardmembers).

I suppose it makes sense: they are loyalty cards, so you better damn well prove your loyalty. I suspect we’ll see other airlines do this too, meaning that folks who are price or route sensitive will either need to a) turn into me and carry a lot of cards, or b) stop earning miles.

I don’t fly United, or generally fly enough anymore to care about all of this, but wow, this feels like a hardline position to me.

Bank of America Rewards Changes

Last week I covered rumored upcoming changes to the Bank of America loyalty program. They have arrived.

The big change is that any BofA checking account client now qualifies for rewards. An additional tier was also introduced, pushing the most lucrative rewards only to the wealthy with more than $1 million in assets at Bank of America and Merrill. Thousands of mass affluent BofA/Merrill users with more than $100,000, but less than $1,000,000 are saying goodbye to their 2.625% earnings rate on the TravelRewards card. Sad.

There are three features of this program that can be worthwhile:

- Bonuses on credit card rewards

- Discounts on loans

- Waivers of checking account fees

All of the other stuff, like automotive savings, access to sporting events, etc. are benefits that seem both challenging to redeem for and not great deals. One time I tried to see if buying a car through BofA was a good deal. It was not.

Merchant Steering

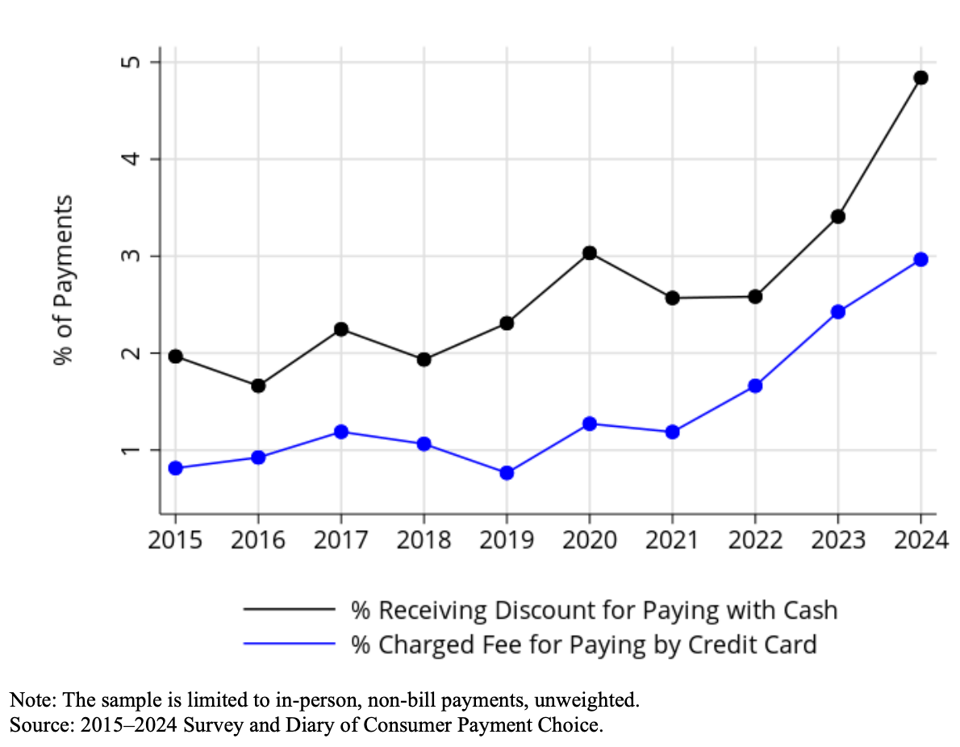

Merchant steering, which is when merchants try to push consumers to use one payment device (e.g., cash) over another (e.g., a credit card), is back in the academic news with a new working paper, “Merchant Steering of Consumer Payment Choice” by Claire Greene, Oz Shy, and Joanna Stavins of The Federal Reserve Bank of Atlanta. Frequent readers know I’m a bit obsessed with discussing credit card surcharging and merchant steering. My high-level take? Consumers hate steering in the form of credit card surcharges. Sure, they will sometimes be swayed, and other times pick new merchants, but paying a few more cents per gallon for gas or dollars for high-end purchases does not drive consumers to change payment methods.

The diverging interests of merchants and consumers is evident. While surcharges (or its twin, cash discounting) is on the rise:

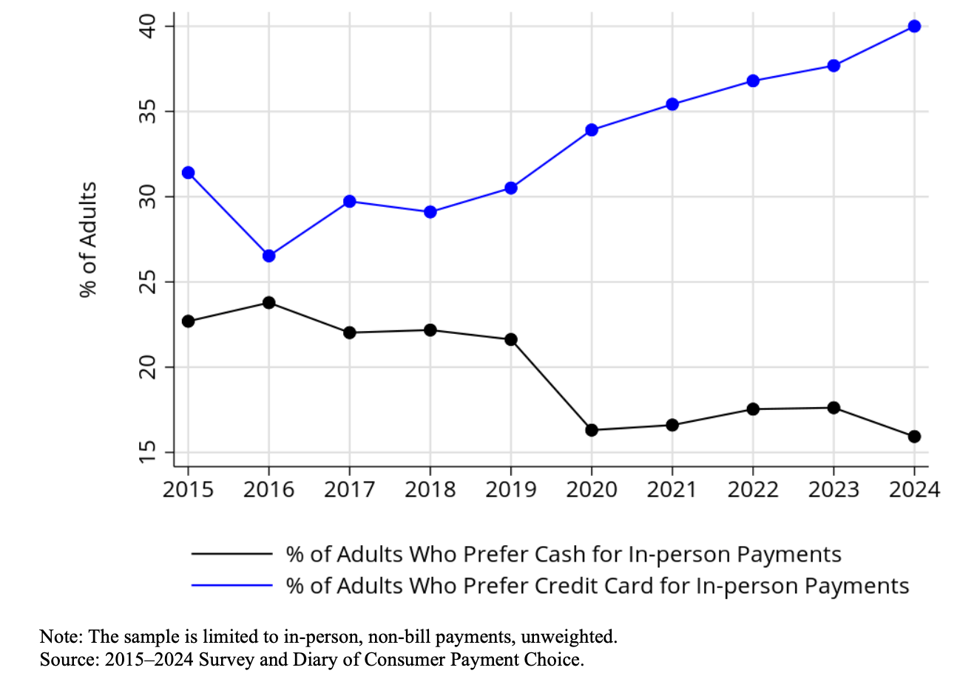

People prefer credit cards for in-person payments at an increased rate:

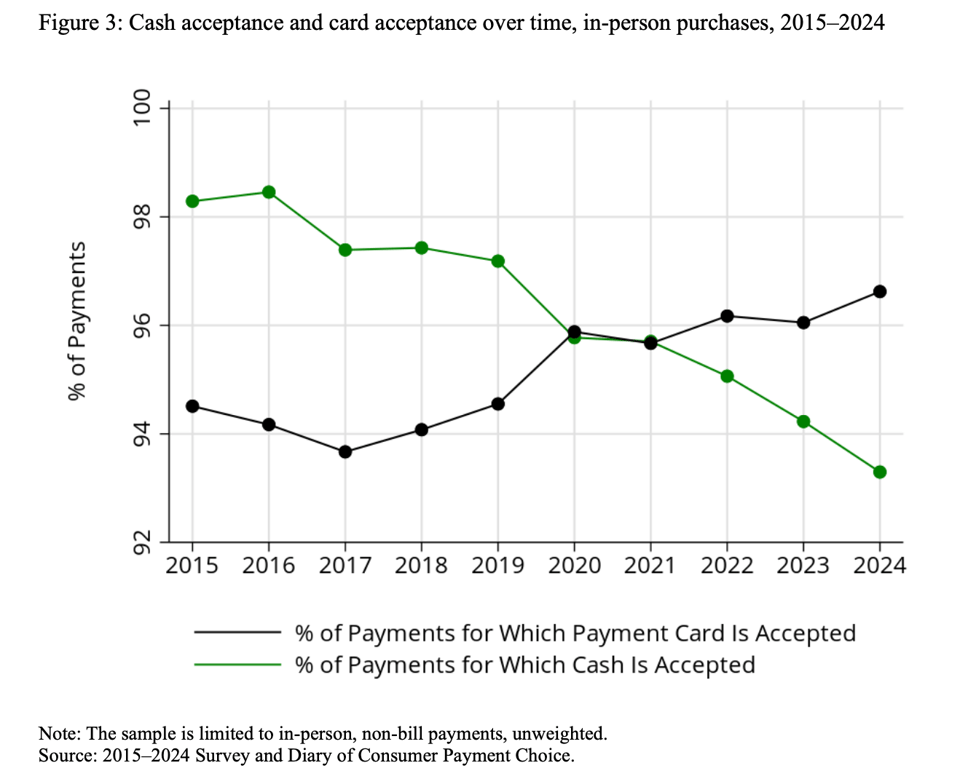

The share of merchants who are cashless (“card only”) is growing (7% of all merchants).

Merchants will continue to want to steer payment selection, but to quote the paper:

We find that consumers make most payments with their preferred method.

and

Discounts on cash purchases do not affect the probability of consumers deviating from using cards and paying with cash.

So, basically, good luck steering people. I still don’t understand merchants who seem to feel that all of the extra communication and friction of saying to their customers “pay me a different way” is worth it, but I guess they do. In the end, they are still sending dollars to the card networks and probably just annoying folks. (shrug)

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.