It’s the Dawning of the Age of Migration - CardsFTW #191

Plus, Inspire, Shield, Slate, and more

Search!

We upgraded our site search functionality for CardsFTW. We hope you enjoy.

Inspire

People who love Disney love Disney. It may cost $1,000 per person per day to have a good experience (e.g., avoiding long lines) at Disneyland, but people still love Disney.

Chase has offered a Disney credit card for a very long time. It was fine. I think the big appeal was Disney images on the cards.

Chase and Disney have announced a new, more expensive Disney card, continuing the trend of high-annual-fee cards. The Disney Inspire Visa is $149 per year and joins the Disney Premier ($49 per year) and the Disney Visa (no annual fee).

The card looks a lot like other premium cards with brand earnings:

- 10% at DisneyPlus.com, Hulu.com, and Plus.ESPN.com

- 3% at most other U.S. Disney locations and gas stations

- 2% at grocery stores and restaurants

- 1% on all other card purchases

And annual benefits:

- 200 Disney Rewards Dollars after spending $2,000 per anniversary year on U.S. Disney Resort stays and Disney Cruise Line bookings

- $100 statement credit after spending $200 per anniversary year on U.S. Disney Theme Park Tickets

- Up to $120 annual credit on Disney+, Hulu, and Plus.ESPN.com purchases

It’s not a terrible deal, even if you’re just streaming Disney all the time. You can use the cards for many Disney products, including theme park tickets, cruise lines, AMC movie tickets, and more.

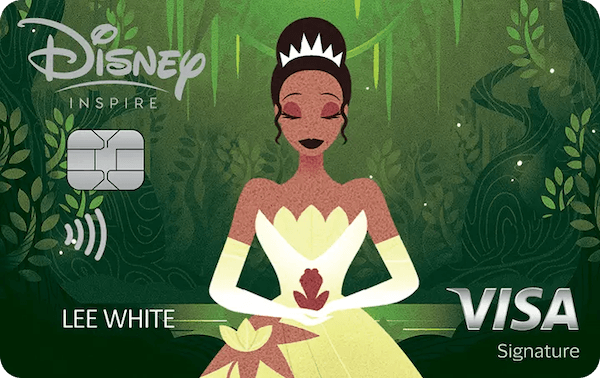

There are five new exclusive designs. If I were to get one, I’d go for one of the traditional designs: Princess Tiana from The Princess and the Frog. Tiana is my favorite princess because, before she marries a prince, she is an entrepreneur working to build her own restaurant. Or, as we say around my house, she’s a Tian-trepreneur.

Slate (Return of)

Speaking of Chase, the old standby low-interest-rate Chase Slate card has returned! Slate is an old card (I think it launched in 2008 or 2009?) It had a famous triple-zero value proposition: $0 annual fee, $0 balance transfer fee for the first 60 days, and 0% intro APR for 15 months (purchases and balance transfers).

The card went away during the pandemic in Spring 2020 (when we thought the economy might totally collapse). Then, in July 2021, Chase Slate Edge came in, with a shifted focus on APR reductions over time.

Our old friend is back: the new Chase Slate offers 21 months of 0% APR on purchases and no annual fee. However, there is a 5% balance transfer fee, which could add up.

Small Business Shield

Along the lines of 0% intro APRs, U.S. Bank has offered a Shield consumer Visa card, with 0% APR on purchases and balance transfers for 24 months (take that, Chase). The bank just introduced the Business Shield™ Visa® Card, with 0% APR for 12 months. Both cards have 5% balance transfer fees. From what I’ve seen, this is the longest small-business introductory offer available (many others offer only 12 months, and only for purchases).

It’s the Dawning of the Age of Migration

If you zoom out over the last 25 years of fintech, you realize the industry didn’t start with sleek apps, neobanks, or venture-scale credit programs. It started with prepaid cards. In the early 2000s, prepaid wasn’t a disruption story so much as a clever workaround. Companies like Green Dot and NetSpend, along with early payroll providers, built products that let money move onto plastic without requiring a traditional checking account. It was the era of government benefits, gift cards, and remittances. Banks were cautious, core systems were inflexible, and prepaid lived comfortably in the gaps they left behind.

What prepaid did, quietly but critically, was establish the modern card program model we use today. It was the first time we saw issuing banks partnering with non-bank program managers. Processors learned how to support pooled accounts and alternative ledgering, while networks proved that card rails could handle much more than just classic debit and credit. Compliance, KYC, and customer service were abstracted and outsourced for the first time. By the time the industry actually understood prepaid, the idea that a fintech company could sit between a bank and a consumer was no longer a radical concept.

Debit came next, and it brought a different level of ambition. As smartphones became ubiquitous and APIs became practical, fintech stopped focusing on just distributing money and started focusing on holding it. Players like Simple, Moven, Chime, and later Varo, reframed the debit card as the front door to a better bank account. These products still leaned heavily on prepaid-era infrastructure (often using the same legacy processors and banks) but the customer promise shifted. Direct deposit replaced physical reload networks, interchange replaced predatory fees as the revenue engine, and transaction data became a product input rather than just a back-office record.

This debit-based era normalized something that feels obvious now but was revolutionary at the time: the fintech brand owned the relationship, not the bank. The issuing bank became invisible to the end user, and that shift set the stage for everything that followed.

For years, credit was the thing fintech circled but rarely embraced. Early attempts were cautious, dominated by secured cards, charge cards, and hybrid products. Brex, Ramp, and Divvy structured credit in ways that limited their risk, while Petal and Tomo focused on alternative underwriting. Even the Apple Card, for all its massive scale, leaned heavily on a traditional issuing and servicing model. Fintech had the distribution and the UX perfected, but true balance sheet risk was still something most founders and investors treated with extreme care.

By the late 2010s, that caution finally started to fade. Better data, more experienced operators, and a growing pool of specialized program managers made fintech credit viable at scale. Companies began launching with the intent to support debit, credit, rewards, and lending all under one roof. The ecosystem finally looked mature. Names like Sutton, Cross River, and Celtic became household words inside the industry, while processors like Marqeta, Galileo, and Stripe Issuing defined the modern stack. From the outside, the industry looked stable.

Much of that stability is younger and more fragile than it looks, however.

Many of today’s scaled fintech card programs launched only in the last five to seven years. Chime’s core growth years, Cash App’s massive card expansion, and Brex’s evolution into a full spend platform all happened during a window of rapid expansion and friendly economics. Back then, speed mattered more than long-term flexibility. Very few teams had the prior experience of migrating a live card program at scale. Contracts were long, and optimism was high.

Now, those same programs look very different. What started as a single debit card now has to support international expansion, complex rewards, real-time risk controls, and embedded payments. Regulatory expectations have skyrocketed, margins are under pressure, and investors have pivoted from "growth at any cost" to demanding long-term durability.

This is where the next phase of fintech is already taking shape.

As those original agreements approach renewal, fintech companies are taking a hard look at the platforms they chose when they were much smaller. Some are discovering their processor can’t support new use cases without messy workarounds. Others find their issuing bank relationship is operationally strained or strategically misaligned. In many cases, the economics negotiated at launch simply don’t make sense at scale. Sometimes, regulators or bank risk committees force the issue for them.

The result is going to be a wave of migrations. Not hypothetical whiteboarding sessions, but real, painful, highly visible moves between issuing banks, processors, and program managers. We are already seeing this happen quietly across the industry, and it will only accelerate as contracts expire. Some of these migrations are to in-house systems (see Chime’s launch of their own core), while others will be using the same structure but with a new bank, new processor, and/or new network.

This isn’t a sign of fintech failing; it’s a sign of maturity. Traditional banks have been migrating cores and processors for decades. Fintech is just reaching that same stage, only faster and much more publicly. The difference is that many fintech companies built their businesses assuming migration would be a "break glass in case of emergency" scenario, not a standard phase of growth.

Over the next few years, the strongest operators will treat platform choice as a strategic asset rather than a launch checklist item. Issuers will be forced to compete on the quality of their partnership, not just balance sheet access. Processors that can’t evolve quickly enough will lose relevance, regardless of how strong their early growth was. The first 25 years of fintech were about proving that non-banks could build meaningful financial products. The next chapter is about proving those products can change, migrate, and adapt without breaking the business. That transition is already underway, whether the industry is ready for it or not.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.