Score! 10% Rewards at Dick’s Sporting Goods - CardsFTW #204

Plus, Uber Drops Discover, Citi Makes ThankYou Points Worse, and New Fancy Lounges

See how Lithic delivers reliability

Dick’s Mastercard Credit Card Launches

Have I mentioned recently that I volunteer as a referee for youth soccer? (I also run the scheduling and stats!) Refereeing is an excellent gig for financial newsletter writers. Well, anyway, youth sports are BIG business. According to The Wall Street Journal, the winner of the $40 billion annual market is Dick’s Sporting Goods. (It’s not where I buy my referee gear, except shoes, but it is where I have purchased all my kids’ sporting gear.)

Dick’s has more than 700 locations (including additional brands like Golf Galaxy and House of Sport) across the U.S. and reported more than $17 billion in total revenue in its last fiscal year. The company has long offered a strong loyalty program (ScoreCard Rewards) with a simple, if a bit odd, structure of 1 point earned per dollar spent, with each point worth 3.3% (so 300 points is worth a $10 reward). If you spend at least $500 per year at Dick’s you achieve ScoreCard Gold status, which gives you one day per year with 3x points (or 10% cashback).

The retailer has offered a private label credit card with issuer Synchrony. Last week, the company announced a refreshed offering, including a co-branded Mastercard card. The new Dick’s Mastercard card earns 10% back on all purchases at Dick’s brands (which is 3 points, but worth more than the regular three points, so you have to define it in cashback, which shows why points not worth 1.0 cents are hard to market), plus 1% cashback everywhere else. Cardholders also earn automatic ScoreCard Gold.

To pull off 1% cashback everywhere else with the weird points value, users earn 1 point per $3.00 at non-Dick’s locations. I want to know if the product team had a long debate about fractional point values and how to show them in the statements.

The card doesn’t have an exciting design, but I do give them (fractional) points for keeping their logo small.

Am I going to get this card? No, my kids aren’t playing sports anymore, and their soccer referee gear selection isn’t good. That aside, it’s a very strong card compared to most retailer cards that max out at 5% cashback on spend at their own brands. Sounds like a home run/touchdown/goal/point for the sports parent or athlete.

Sponsored by Lithic

Most processors connect through middlemen. Lithic connects directly to the network.

High-growth fintechs don't have time for unreliable infrastructure. Lithic delivers 99.99% uptime, high-fidelity transaction data, and direct network connections. No filtered data, no downtime excuses.

Citi Ends ThankYou Points Sharing

One of the most enjoyable things we do at Totavi is help people build innovative loyalty programs. One of the biggest challenges is that the features users want in a loyalty program are often more expensive for providers. This leads to difficult trade-offs.

One thing that technically can add cost, but seems like an easy win, is points sharing. For example, if my spouse and I each have memberships in a loyalty program, the program allows us to combine our points. I love this from both the standpoint of getting more out of our combined household spending and because it prevents one member of the couple from feeling dependent on the other. For example, my house shares a Starbucks Rewards account and, as a result, my wife picks up her coffee when they yell “Matthew G.”

In most programs that support sharing, you can only share points with a member of the same household, which is a smart and fair limitation to potential scams. Several leading programs offer points sharing both in travel (JetBlue’s TrueBlue program) and in financial services (Chase Ultimate Rewards).

Citibank’s ThankYou Rewards program has allowed points sharing in the past, one of its redeeming features (it’s not a great program, IMO). However, as of this past Sunday (May 17), the option is gone! Citi’s program had been very flexible, allowing for points transfers with anyone. I can see where that will get you into trouble (e.g., manufactured spending, points theft, etc.), however they could have simply gone to a household system.

Mastercard Launches World Legend Lounges

Back in March, I covered Mastercard’s launch of the first World Legend Card in Canada, following the July 2025 launch of the new product type. Today, there are only three World Legend Mastercard cards issued in the United States:

- Citi Strata Elite™ Card

- Citi® / AAdvantage® Globe™ Mastercard®

- Bilt Palladium Card

Because a premium credit card just isn’t a premium credit card without a special lounge, Mastercard has launched a new “Mastercard Airport Dining Experience.” This is an exclusive premium benefit that is available to the cardholder and up to 3 guests with a World Legend Mastercard™ on an unlimited basis! These experiences are currently only available at GRU (Sao Paulo, Brazil) and HKG (Hong Kong), with MEX (Mexico City) coming next. What is it? I don’t know!

Each premium airport dining experience location is a specially curated experience designed for World Legend and World Legend Exclusive Mastercard cardholders and their companions, including, but not limited to, the following amenities:À la carte dining and chef-curated tasting menus featuring locally inspired cuisineSignature Priceless desserts & beverages will be exclusively available to order (including Mastercard’s own Priceless Passion and Priceless Optimism cocktailsComfortable seating for dining, working, and relaxing, with nearby power outletsFree and unlimited high-speed Wi-Fi

Not a World Legend Cardholder? You can access the HKG lounge with a World or World Elite cardholder and pay just $85 USD (or $700 KHD). In GRU, you can’t do that; you must be with a World Legend cardholder.

Thank goodness for video reviews! I couldn’t find one for HKG. LMK if you make it in.

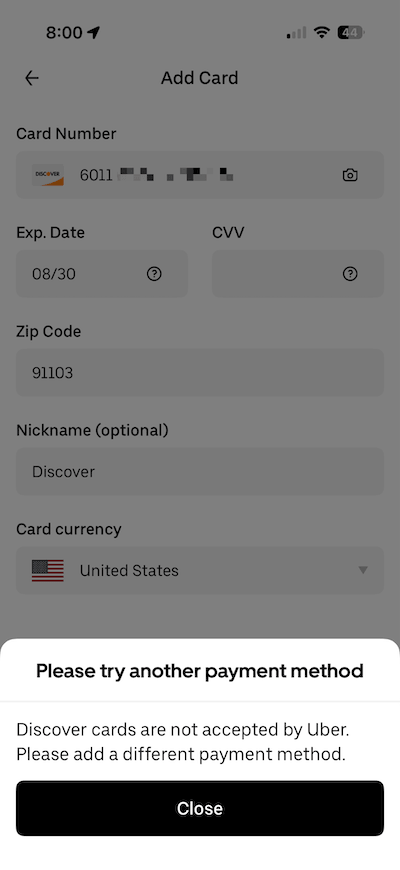

Uber Denies Discover Dollars

As seen on Reddit’s r/discover, for some reason, Uber has decided no longer to accept Discover Network cards. They claim it’s “expensive,” which seems wild. Discover is not more expensive to accept than Visa or Mastercard. Is this related to the Capital One acquisition? (See last week’s newsletter for a full history and exploration of the future for Discover.)

I tried this myself, and the worst part is they don’t tell you they don’t accept Discover until you finish filling out the form! I mean, you know it’s a Discover card (Starts with 6011? That’s Discover). They even changed the network logo on the form in the top left, so you know they know. Rude.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.