Settlement Surcharges Will Lead to More Confusion - CardsFTW #208

Plus, Spinwheel Data, Kudos launches my favorite Wallaby feature, and more

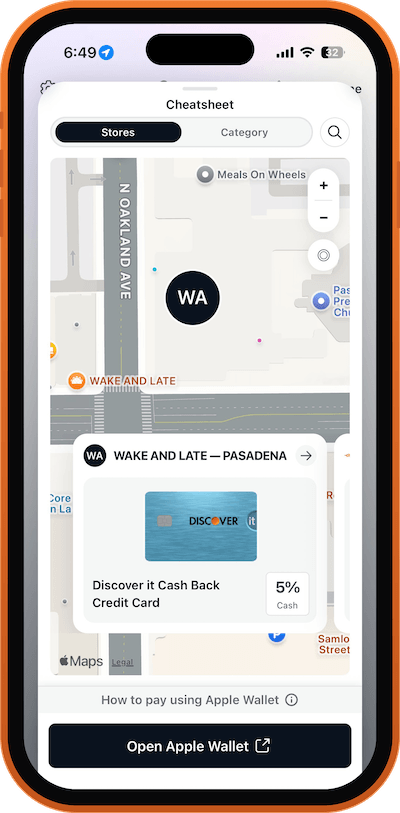

Kudos Meets Wallaby

In 2011, I started Wallaby to help people better manage their credit card rewards. A key feature of our app was to geo-locate you and immediately recommend the right card for your purchase based on the merchant you at which you are shopping.

Readers may know I’ve been a long-time fan of Kudos, which launched as a rewards-maximizing browser extension. Last week, they launched a new feature in the app to do the same geo-location. Thank goodness! Credit card rewards optimization has never been more popular (I might have mistimed this), and I’m glad to see a team focused on accuracy and intelligence bring this capability back to the market.

Even I Don’t Have 170 Cards

Spinwheel, a real-time consumer credit data and payments company, is out with a fun study from its data this week. Spinwheel says one borrower has 170 different credit cards, which is absurd. When I’m sitting in the chief credit officer role, I have knock-outs for this behavior, but I guess some issuers do not! (What could you be doing with that many cards? Come on.)

The report covers a number of interesting metrics I suggest you check out yourself, but beyond the 170-card borrower, the thing that caught my eye was an analysis of debt mix: nine out of ten consumers carried a credit card balance at the time of the report (note, this doesn’t mean they are revolving that balance, just that it exists). However, credit cards account for just 7.2% of total dollars owed, with 70% of the loan value going to mortgages. Sort of obvious, of course, but still interesting to see that order of magnitude difference highlighted.

While many of the metrics come across as a bit obvious (e.g., folks with higher scores have lower credit card debt), others are a bit counterintuitive. Building on the mortgage point above, people with excellent credit (800+) have most of their debt as secured (91.8%), driven by mortgages, even though we often think of low-quality borrowers as having the need for more secured debt (but only true for credit cards typically).

In a related note in the Wall Street Journal on Monday, banks are trying to grow their loan books at the same time consumers are stressed by inflation.

Chase Sapphire Preferred’s Refresh

Chase announced a refresh of its Sapphire Preferred Visa card. The most surprising part is that the annual fee didn’t go up (still $95).

Starting on June 15, the card adds 3x points on gas and EV charging, as well as on vacation home brands (think Vrbo and Airbnb). The card also adds an additional Chase Travel Hotel Credit ($100), a $120 credit to Global Entry or PreCheck, and new coverage for emergency evacuation and transportation. If you happen to be one of the few customers who haven’t already received a free Apple TV subscription from some other service, you can also get one here.

The card battle continues. Chase has been very aggressive as of late, pushing very high signup offers across both consumer and business cards. Many categories now earn 3x on Sapphire Preferred, including dining, streaming, and online grocery points, plus 2x on travel other than vacation homes (an odd distinction if you ask me).

Given the value delivery, I think it looks surprising that the annual fee didn’t go up (the Reserve went up $245 last year!), but $100 is a major psychological threshold. There are a lot of customers who won’t pay a card fee, and a lot more who won’t pay more than $100. That line is keeping this card from price pressure (this time around anyway).

Books and Barclays

A small note in co-brand news: Barclaycard announced the renewal of the Barnes & Noble Mastercard program. This is a card program I had forgotten about, although I am aware that the bookstore still exists. This is a 20-year-long partnership, something I feel like we see less and less of in co-brand.

The card is a standard variety co-brand: 5% cashback on purchases at Barnes & Noble, in the form of $25 gift cards. Plus, a Premium Membership if you spend $7,500.

I think they should extend that membership to everyone, but so it goes.

Surcharges: They’re Just So Messy

Last week, US District Court Judge Brian Cogan provided preliminary approval in a multi-decade lawsuit over the fee merchants pay for accepting credit cards. The headline number indicates that the settlement will be worth more than $200 billion (up from the proposed $30 billion settlement that was rejected in 2024).

As I have written time and again, merchants love to complain about paying to accept payment cards, yet continue to accept them. Even this settlement doesn’t unite merchants: organizations representing both big-box retailers and convenience stores requested that the issue go to trial.

The new settlement does away with what was known as “honor all cards,” allowing merchants to choose to accept all card types, just “traditional” or baseline rewards cards, premium cards, commercial cards, or some combination thereof.

The settlement also requires a net 10 bps interchange deduction (to posted rates) over the next five years, a 1.25% cap on interchange for consumer cards over the next eight years, and the rights for merchants to steer customers to lower-cost cards with surcharges and discounts.

A few notes:

- You know who doesn’t pay posted rates? Big retailers.

- The cap in interchange does not cap network fees; those could go up.

- Regular rewards cards often earn between 1.4% and 1.6% interchange today, so the cap is meaningful, although many merchants see more premium cards than traditional ones.

At a high level, I think merchants will continue to accept all consumer cards: do you want to turn away your highest spend user who has a Chase Sapphire Reserve? Some merchants absolutely will enforce this, but I think they might alienate their customers.

Prior to the settlement being approved, I was thinking about the problem with surcharges in a personal anecdote: the company that maintains my pool (I do live in Los Angeles) posts a surcharge on every invoice that violates rules. I don’t think anyone is going to complain or report him, but it sure makes interactions around payments difficult (it’s a good thing the pool stays clean).

At the bottom of his invoice sits a line I have stared at every month for a while now:

> Credit card processing fees apply (3.5% Visa/Mastercard | 4% Amex)

It is a small thing. It is also, in roughly four different ways, not how surcharging is supposed to work.

Repair Work is Expensive

This month, the pool bill was way larger than normal because I had to have a major piece of equipment replaced. I figured I would just dodge the card fee entirely and send it over Zelle. Free, instant, done. That is the whole pitch of Zelle.

My bank had other ideas. Typically, the company debits the funds out of my account, but that wasn’t an option here. To my bank, he looked like a new payee, so it capped what I could send to a brand new recipient. My limit was way too small to pay in one shot. So I did what any reasonable person does at 9pm on a Sunday: I broke a single payment into installments like I was financing a sofa.

Then the second surprise. Because he was a “new payee,” the bank also decided this particular Zelle would not be instant. It would take three days. Zelle, the network whose entire reason to exist is that the money shows up before you have put your phone down, made me wait three business days to pay my pool guy in chunks. The one time I wanted the rails to behave like the marketing, they unionized.

The friction here is not an accident. New payee plus a large amount is a textbook authorized push payment fraud pattern, so the bank slows it down and rings fences the limit. These are good risk controls. Genuinely the correct call, but very annoying.

I had an alternative: I could have just accepted the 3.5% and paid by card, then run it through my Robinhood Gold card at 3% cash back to minimize the fee.

As I thought about my options, I double-checked my math to make sure these surcharges, which looked suspicious, were allowed. They are not.

Visa caps credit card surcharges at 3%, lowered from 4% back in April 2023. A 3.5% Visa surcharge is over the ceiling before anything else is considered. The surcharge is also supposed to be the lesser of your actual cost of acceptance or the cap, so a flat 3.5% from a small services merchant whose real effective rate is closer to 2.9% is recovering more than the cost it is meant to offset. That is the exact pattern that turns a fee program into a rules violation.

The Visa versus Amex split is its own problem. Networks do not (as of today) allow charging different surcharge rates by network, and Amex specifically forbids surcharging its cards at a higher rate than the competition. Charging 4% on Amex and 3.5% on everything else breaks both ideas at once.

And the surcharge cannot touch debit or prepaid cards at all. Durbin closed that door. A blanket "credit card processing fees apply" line tends to sweep debit in without anyone noticing.

Then there is the small matter of geography. This is California, where SB 478, the Honest Pricing Law, took effect July 1, 2024. A posted percentage fee on the invoice is the drip pricing the law was written to kill. The compliant move here is to build the cost into the price, post-separate cash and card prices, or offer a cash discount. A line at the bottom of the bill is not a structure; it is an exposure.

Look, I’m not going to tell him (and I’m not trying to report him to the folks at the networks who read this newsletter), but it’s an example of the many challenges of legally surcharging. I think it’s only going to get worse with the new rules. I want to know why businesses are willing to make it so frustrating to give them money!

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.