Notes from Vegas - CardsFTW #179

Plus, new debit and credit cards, deals day, and more

2025 Money20/20 Recap

I’m still recovering from another year of Money20/20. I’m not too cool to admit that I love going to this show every year. I think I’ve been every year it’s been put on, starting in 2012. There are a lot of tongue-in-cheek LinkedIn posts about how hard it is, or how to survive Vegas, but if people didn’t want to go, they simply wouldn’t. It’s the fintech industry’s largest and most important gathering. The show sells more than 10,000 tickets, and there must be another 1,000 to 2,000 people who don’t buy tickets and participate in LobbyCon. I love it.

Money20/20 this year felt like: “fintech is back.” In 2022, we were at peak fintech: you could feel that the end and scandals were coming, but companies still had money and had booked events months in advance. I was out until midnight daily, going to pre-parties, post-parties, and dinners in between. 2023 was sort of sad. 2024 was recovering. 2025 was great. We tracked more than 110 events around the main show, up 42% from last year and ~65% from 2023. We’re back!

I was proud to see Totavi’s own Ellen Dearborn take the stage for the first time as a moderator, leading a panel on modern card issuing strategies (perhaps our favorite topic), with leaders from American Express, Qolo, and Fetch Rewards. The seats were packed. (Last time Money20/20 put me on a panel, I got the dreaded Wednesday late morning special and a mostly-empty room.)

Discussions about agentic payments, artificial intelligence, and stablecoins were everywhere. As were discussions about how overblown agentic payments, artificial intelligence, and stablecoins are. I love talking about the new technologies that will seem commonplace ten years out, but the show was also a reminder of how far we’ve come. Apple spoke about its journey in mobile payments, which was announced just before Money20/20 in 2014. (Please enjoy this throw-back article with a great video showing EARLY Apple Pay.) Today, mobile payments are (finally) commonplace.

The folks from Totavi (myself, Ellen Dearborn, and Jessica Marquez) spent our time talking about embedded payments, debit and credit card issuers, and loan sponsorship. These are the nuts and bolts of modern fintech and we love building on them.

See you next year.

BofA Deals Day

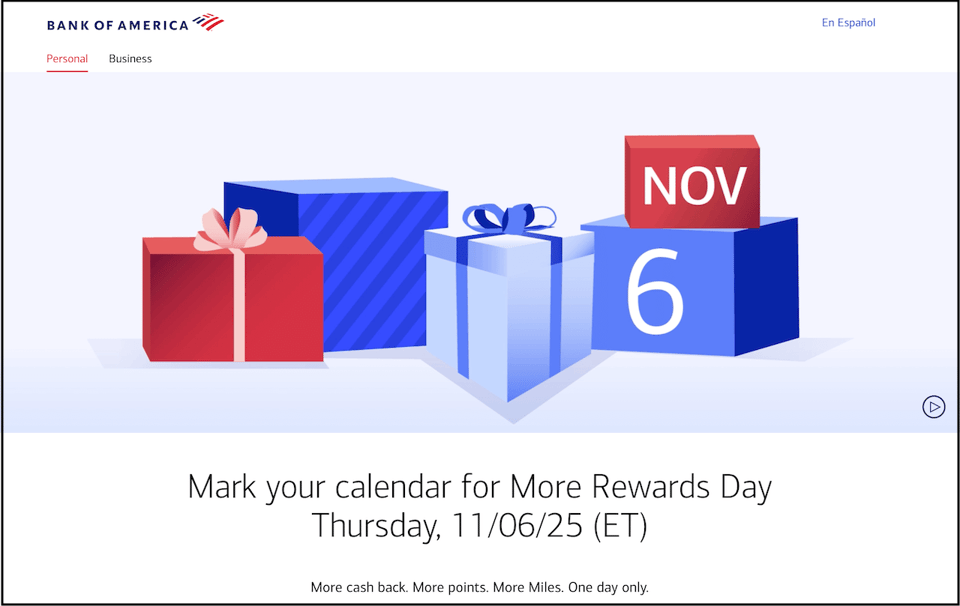

Bank of America is running its “More Rewards Day” again tomorrow, November 6th. For the entire day, all rewards on Bank of America cards are enhanced (to a limit of $2,500 in purchases). If you’ve been pondering a big purchase; you can time it right (all times are in Eastern Standard time). Cardholders with cashback, miles, or points cards earn an additional 2% cashback (or 2 points/miles) per dollar. Even users without existing cashback rewards will earn a minimum of 2% cashback.

Included in the deal are cobrand cards like the Atmos (formerly Alaska Airlines), Norwegian Cruises and Allegiant cards. Play your cards right and you could really score - I think you could top out at 7.25% cashback if you stack your top category on the Customized Cash Rewards Card with Platinum Honors.

I’m not sure why BofA does this, but it is fun. We don’t see a lot of one-day-only deals and this doesn’t coincide with a particular holiday. I don’t need another reason to spend money, but I’ll try to remember to select from my BofA cards on Thursday.

Gemini Solana Card

We continue to see more activity in the crypto rewards credit card arena. Gemini has one of the longest-running products in the market and has started to issue special edition cards to drive adoption. With Gemini’s Mastercard, consumers can select in which cryptocurrency to earn rewards and now have several card design choices to align with their preferences: Bitcoin, Solana, and XRP. The Solana design launched last month. It reminds me of 1990s-era MBNA credit cards for everyone’s alumni association: we use our credit cards to align with our identity.

With the Gemini card you can earn from more than 50 different crypto currencies and choose from 6 card designs: three standard in black, pink, and silver, or the Solana, XRP, or Bitcoin editions. The cards work the same (indeed, you can select Bitcoin as your reward and carry a Solana card), but speak to the way in which consumers like to personalize. Discover card offers more than 100 designs and people love that!

Uphold XRP Reward Debit Card

Speaking of Ripple and rewards, Uphold, another major crypto exchange known for its users' love of the Ripple XRP token, has relaunched its debit card product. When I was President of Apto Payments, we helped to power Uphold’s prior generation debit card. The new card returns after a more than two year break and enables users to earn up to 6% in XRP rewards, whether they spend fiat (e.g., USD), crypto (XRP), or stablecoins with the card.

Southwest Airlines Debit Card

In early October (see CardsFTW #175) I mentioned the upcoming Southwest Airlines Debit Card. The card officially launched last week. The card is issued by Sunrise Banks, N.A., and processed by Galileo. Rewards on debit cards are rare (crypto notwithstanding), but this new card includes a 2,500-point welcome bonus, 1 point per dollar on Southwest airlines purchases, as well as dining and subscriptions, and 0.5 points per dollar on all other spend. Cardholders can also earn various qualifying points and discounts.

Revenue on debit cards is substantially constrained compared to credit cards (lower interchange, no revolving interest fees) which leads to reduced rewards. Prior to the Durbin Amendment many debit cards had some form of rewards, but airline debit cards have been less common. Truist offers a Delta SkyMiles card, Bank of Hawai’i offers a Hawaiian Airlines Visa Debit Card, and Bask Bank offers an American Airlines AAdvantage Savings Account.

The new Southwest card (and upcoming United Card) are unique in that they are offered on a fintech stack (by long-time industry participants Sunrise and Galileo) whereas other offerings are offered by traditional banks.

There is absolutely a market for folks who cannot access credit (or just prefer debit). I expect we’ll see more of these.

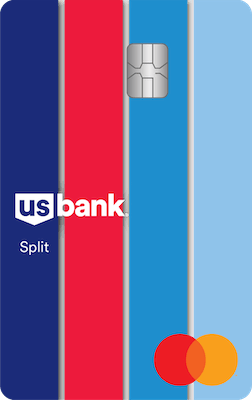

U.S. Bank Split World Mastercard

U.S. Bank continues to introduce new products. Its latest is a combination credit card and BNPL-style product, the Split Card World Mastercard. Every purchase (of more than $100) on the Split card is eligible for a no interest, no annual fee, three-month, three-part payment plan, or extended six and twelve-month options. I have written ad nauseum about the convergence of credit cards and BNPL, including the pay later/fixed repayment options that come with most Chase and American Express Cards. The unique angle here is that purchases are automatically split into three. Users who want to extend for six or twelve months need to simply login into the app prior to the end of their billing cycle, review and agree to the plan fee, and shift a purchase.

Plan fees will be calculated and shared with users when they attempt to change the plan length, so it's not clear to me from the marketing and disclosure materials if these are good deals or not.

While I think that consumers crave transparency on interest fees and this is a step in that direction vs. compounding-interest open-ended revolving plans, I am concerned users of this card will simply end up with many, many plans, paying similar rates to another card (except that it won’t be all lumped together). I’ll be watching for more cards of this type.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience, spanning from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.