Merchants Still Hate Interchange - CardsFTW #19

Plus, a surprise exit by Dosh, and more on bitcoin rewards

This past week was just packed full of news. I was excited to start working on this issue, and then on Monday, Cardlytics announced it is acquiring Dosh, joining together the latest in card-linked offers with the original. More on that in a bit; let’s dive in.

Let’s All Sue the Networks

Merchants love to complain about interchange. At the same time, amusingly, merchants are increasingly paying larger fees to Buy Now Pay Later providers for point-of-sale lending. To my point previously, credit cards are point-of-sale lending. When credit cards launched, merchant discounts ran as high as 7-10%. Many merchants had lines of credit they ran directly for their customers and back-offices to operate them. The new discount rate was a pretty good deal based on payment speed and outsourcing this function to the bank. Over time, those have come down to 3%, but some merchants are still paying higher fees than they should because of obnoxious ISOs or unclear pricing.

In previous years, major lawsuits spearheaded by merchants like Walmart have ended in large settlements, but still no fundamental change from the networks. Now, Intuit is suing the networks. What’s unique about Intuit’s suit is that Intuit acts as both a payment facilitator, accepting payments on behalf of merchants, and a traditional merchant, charging its own fees. In previous suits, the litigants were on one side (merchants), but Intuit sits on both the retailer and the acceptance sides.

I am certainly no lawyer nor judge, but I think these lawsuits are dumb. It’s all negotiating tactics to me. The card networks are enormous. The card networks do have pricing power. The card networks also have strict operating rules. However, there are at least four major networks in the US (Discover and American Express count, too). Plus, a merchant doesn’t have to accept cards; they choose to do so. The operating rules generally make sense, and consumers enjoy them. The consumer experience wherein a user could only use a particular type of card at an individual merchant would be off-putting.

Simultaneously, the Wall Street Journal published another article in its series which could be titled “Merchants Still Hate Interchange.” Specifically, at issue in the latest installment, online purchases cost more than physical purchases (and merchants are selling a lot more online). There is also a looming rate increase (already delayed from last year). Consumers are using cards way more.

Yes, interchange could be lower. Yes, there is room for an alternative, low-cost network. Some merchants would adopt that, but many would not, only due to inertia. Many consumers would not because they are happy with the way things are. As we have seen with past interchange lawsuits, the most likely outcome will be a settlement. It’s unlikely that the card networks will be forced to change how they do business.

More on Bitcoin Rewards

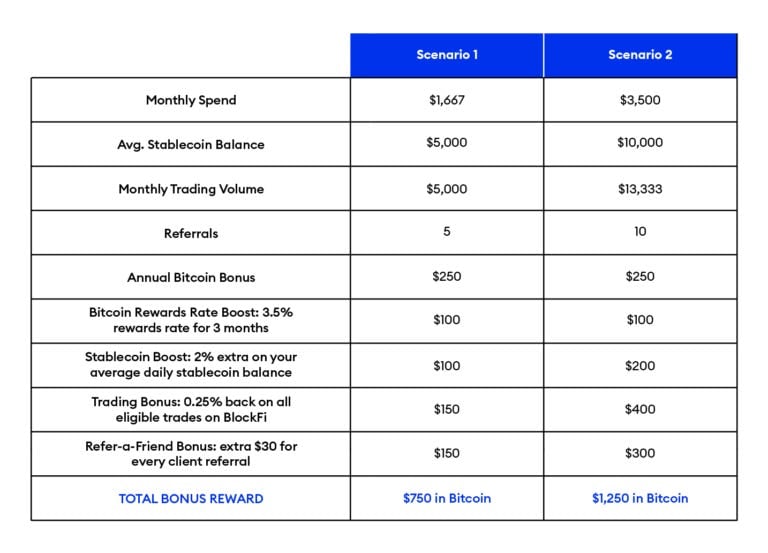

Speaking of expensive interchange, it funds those wonderful rewards customers can earn on their credit cards. Last year BlockFi, a large cryptocurrency exchange startup, announced it would be launching a Visa credit card in partnership with Deserve and Evolve Bank & Trust. At the time of the announcement, the card’s key feature was announced as a flat 1.5% cashback rate (paid in bitcoin). In addition to a standard-sounding signup offer ($250 after spending $3,000 in the first three months), BlockFI has announced three interesting new rewards structures (and a fourth standard one).

These are complicated to me but are designed to drive behaviors on the card and in the BlockFi system. Many existing cards reward consumers around other activities (e.g. benefits for hotel stays, etc.) but this represents a tighter coupling to the underlying brand than typically seen. It is the first card that I am aware of that is tied to trading activities. (Co-brand cards for traditional investment houses like Merrill Lynch typically provide benefits based on asset volume, not on specific activities.)

The first reward is a follow-up incentive to the signup bonus. After earning that $250 in bonus bitcoin for spending $3,000 in the first 90 days (effectively almost 10% cashback for the first 90 days), cardholders will earn 3.5% cashback in months four through seven, up to $100.

The second reward is a bonus in BlockFi’s interest-bearing cryptocurrency account. Users with certain assets in that account will earn a bonus APY of 2% when they use the card, up to $200. The card will have an annual fee of $200, so if you use the cardright, the fee will be covered, but it seems unlikely most users will earn this bonus.

The third reward is a trading bonus. Cardholders will earn a rebate of 0.25% on trading volume just by holding the card (up to $500). There is a fourth refer-a-friend bonus, but that’s pretty normal and a very low payout at just $30.

Here’s a handy chart to explain how this works:

If you need a chart to explain it to your users, you’re probably making it too complicated. (Note: I am guilty of building products that need charts to explain.)

These features will appeal to a gaming and trading crowd. If that’s an excellent match for their users, then this could go very well. I don’t know anything about BlockFi’s users, although I have a small account with some bitcoin. While more and more people are buying bitcoin, it’s unclear that your more average user will want to engage in these advanced strategies. I’m hoping this will work for them. They report a huge waitlist, and may their waitlist convert at above-average rates.

An Update on BNPL Cards

I recently wrote about the blurry lines between Buy Now Pay Later and Credit Cards. I noted that Affirm had a small virtual card business. Last week Affirm announced it would officially launch a buy now, pay later debit card in physical form. The new card will allow users to make Affirm purchases at any store, online or offline, and “pay now” with a debit-like function or pay in installments.

Max Levchin, founder and CEO of Affirm, said, “There is no card that currently allows consumers to make the choice between paying upfront or over time. We thought it would be very powerful to combine the two.” I find this claim false. Users can already pay for purchases on credit cards during a grace period with no fee or use a feature like MyChasePlan or other credit card-based fixed loan products. Or they could simply use a debit card for some purchases and a credit card for others (which is VERY common).

Generally speaking, I am in favor of more new products and choices. There is no single consumer mindset or feature that works for everyone. However, making BNPL installments a feature you can use every day and everywhere will inevitably lead to consumer confusion. How many simultaneous installments can a user keep track of at one time? When does it all just become a single credit card product

Varo’s New Credit Builder Card

Credit cards for people with no, limited, or bad credit have long been an area of attempted innovation. Traditional secured card products are terrible for consumers, with high fees and low limits. Back in CardsFTW #4 we discussed many of these, like cards from Chime, Jasper, TomoCredit, Deserve, Mission Lane, Upgrade, and Cred.ai. Varo, a fintech startup that keeps trying to convince people it’s the first fintech with a bank charter (I would say that is Green Dot), announced its new credit builder, Varo Believe. The card, much like Chime’s product, isn’t exactly secured, but does set aside funds in a linked deposit account as charges come in so that the card will be paid on time, every time.

I love products that help people establish credit and give them strong guardrails to success. Over time, we will see if these credit builder cards can train long-term creditworthy behaviors (not spending more than they have, paying ontime). Will consumers continue to demonstrate the right behaviors when graduating to traditional full credit products? Or, will consumers fail to properly manage their credit when the system doesn’t do it for them? I don’t agree with Varo’s claims about how unique the product is (I think Chime beat them to it), but it’s good to have more options out there for more customers.

Mexican Cards

Speaking of new cards, I learned this week about Stori, a Mexican credit card startup (via their funding announcement). Mexico is an interesting market for cards, as cash has had advantages in societal acceptance. Whereas in the United States, carrying a card can signal wealth, in Mexico, cash traditionally signals wealth. We looked at entering Mexico with Green Dot in 2007-2008 and didn’t due to the financial crisis, although I think the opportunity was huge. Online shopping, safety, and the fraud prevention offered by cards is a substantial benefit versus using cash.

More on Card-Linked Offers

The late-breaking news this week that Cardlytics will acquire Dosh surprised me. From the outside, Dosh appeared to be doing very well. The company pivoted from a direct-to-consumer offering with an app for card-linked cashback (still in market) to providing a B2B offering for neobanks and others that competed against Cardlytics. Dosh raised a total of $87MM according to Crunchbase and is now selling for $275MM, which sounds good but probably wasn’t the ideal outcome.

As we see additional debit and credit card entrants (neobanks and challenger credit cards), the rewards and loyalty component of their offering will be an important part of the market. There are a few other players in the space helping to bring merchant offers to consumers,including Kard, Rewards Network, and Figg, which provide merchant-funded discounts to consumers. Some card issuers (such as American Express) do this directly themselves , while others use a company like Cardlytics to power the experience.

From the outside, I am going to assume this is a defensive play on Cardlytics' part. One of the challenges in card-linked marketing is that it is unclear if the offers drive new consumer behavior, and many banks do it more for engagement than for the revenue it provides. It can be lucrative for consumers. I have saved thousands over the years, although high-value offers are fewer and further between now than a few years ago. For more on the card-linked offer space, read CardsFTW #5 from last October.

As fintech companies mature, there will be continuing demand for this service. Cardlytics is better positioned to work with smaller, modern companies via Dosh than its traditional offering, an on-premise, bank-grade setup.

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.