Another Zero Card - CardsFTW #22

Not to be confused with the Zoro Card. Yes, these are all real products.

There is an absolute overload of news from the past week, but let's try to keep things in order. First up, more challenger cards are coming to market.

Neobank Aspiration Announces Zero Card

Aspiration is a late-stage neobank with a reported $250 MM in venture funding. Aspiration has taken a social approach to its business. Their core debit card product promises lower fees than traditional banks, paired with investments in climate change projects driven through consumer behavior.

The core Aspiration account is pay-what-you-want (whether this is good or fair is an entirely separate topic for another day). The card promises that (unlike banks) no profits will be invested into fossil fuel projects and provides cashback on purchases from merchants that are members of the Conscience Coalition, a group of brands committed to combating climate change. The Aspiration Plus account is $15 per month but includes more cashback, plus carbon offsets based on gas purchases and more.

Last week Aspiration rolled out a waitlist for the Aspiration Zero card, a climate-focused credit card. Details are light, but the card promises to plant one tree per swipe, track climate neutrality by user action, and reward you for doing so. (One unique note on the waitlist, Aspiration promises to plant trees when you join, so go on and sign up!)

Green cards are hot on the market, although most are in the pre-launch phase. Several years back, Commerce Bank launched the SustainGreen Mastercard, but the bank pulled it from the market in just months. There is, of course, the World Wildlife Foundation credit card from Bank of America and several other smaller programs for smaller nonprofits. There are also debit card products, like Bank of the West's One Percent for the Planet card.

Will consumers go for these reward programs? Or will they continue to want to earn their airline miles and then fly on carbon-spewing planes? Time will tell, but with several products coming to market, the chance of success grows.

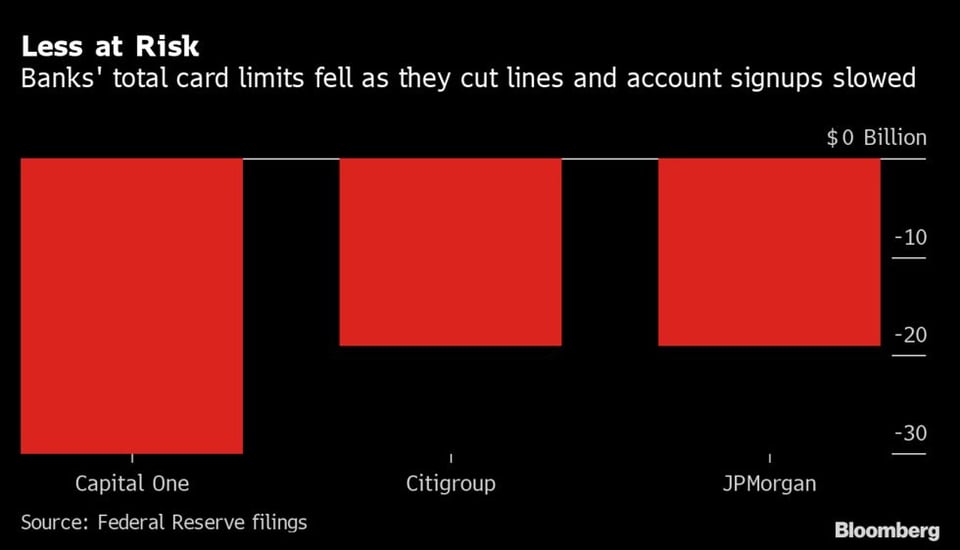

Credit Card Lines Aren't for Certain

Many consumers don't fully understand that the credit line attached to their open revolving card may go down. You can open an account and receive a line of $500, $5,000, or even $50,000. However, if you're not using it, or if signs in your credit behavior show risk, the bank can trim that line. Bloomberg reported that large national banks cut 99 billion dollars in cumulative credit lines from consumer cards through the pandemic. These most likely affected folks who needed it the most. As the article points out, if you're in a rough spot financially, replacing those lines may be challenging. (With a lower score or income, it will be hard or impossible to open a new card to replace the old line.) Reducing lines at a time of need adds insult to injury as cards are a financial tool one can turn to in hard times.

As we head in the rest of 2021, I think we will see line sizes increasing and new card offers and approvals growing. Line reduction may be a short-term concern, but it was no doubt highly impactful for consumers affected.

In related news, people don't like their banks very much. The Consumer Financial Protection Bureau, a federal regulator, reported that complaints were up 54% year-over-year. Credit and consumer reporting complaints accounted for more than 58% of complaints received. Credit card-specific complaints came in at 7%. As banks squeeze access to credit and pandemic-related rules governing what can and cannot be placed as negative marks on credit reporting sprung up, consumers reported many errors with the nation's big three credit bureaus. (Credit reporting agencies are one set of companies that people might dislike even more than their bank). Credit reporting is a mess in regular times, and the pandemic exacerbated the chaos last year. There will be a long tail of errors and complaints, and I expect continued CFPB complaint growth in 2021.

Challenger Card Updates

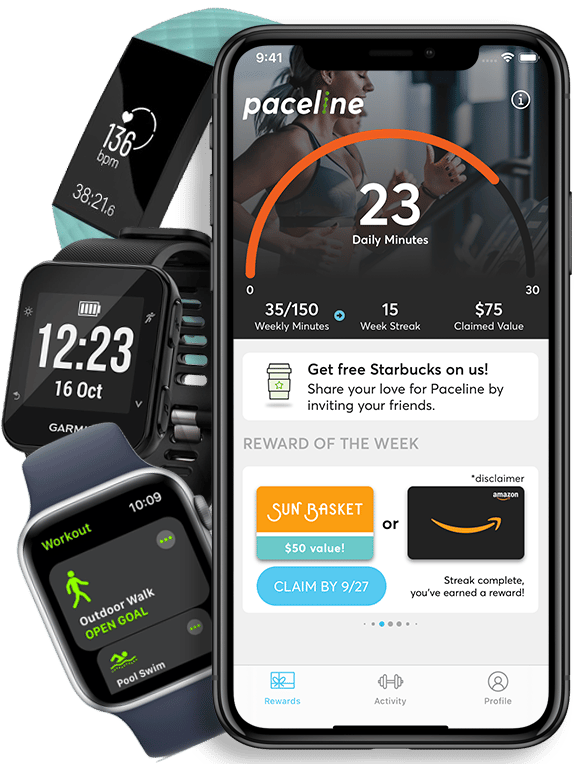

In addition to the new Aspiration card, we saw more signs of progress with challenger credit cards. Paceline, an early-stage fitness-related startup, announced its intention to work with RailsBank and their new US Credit Cards as a Service platform to launch a Paceline credit card. Paceline currently has a card-linked offer reward system.

Download their app, connect your Apple Watch, and earn a cash reward for every week you meet the fitness goal. Paceline has been very popular--free money! Now, they are moving to the next phase of their business by adding a rewards card that promises to reward you for spending and healthy decisions. Joel Lieginger, Paceline's founder, has shared the company goals around insurance and other products tied to health and wellness. Paceline is not the only company working in the health and card space. A few stealth efforts are out there, and I hope to feature them soon!

OppLoans, a personal loan company focused on helping middle-income, credit-challenged consumers, is also working on a credit card, as evidenced by several recent job postings. There is limited information available publicly, but we can expect a secured or low credit limit card with credit builder aspects to come to market given the company's focus.

UK Interchange Increase

While I usually focus on US news (I don't think I could keep up with global news!), I wanted to highlight recent Visa news given the relevance to the last several weeks of discussion on interchange. The Financial Times reports that Visa will raise interchange in the UK. The EU heavily regulates credit card interchange, which is not regulated here. The change is dramatic given historical UK/EU country purchases. Card not present transactions between the UK and EU will grow to 1.5% for credit (an increase of 500%) and 1.15% for debit (an increase of 575%!). I missed it, but Mastercard made a similar announcement in January. While this only affects certain cross-border transactions, the increase brings the cost more in line with US interchange (1.6-2% for credit). Without regulation, interchange rates will continue to increase.

Nothing to See Here

In late 2019 as Apple launched their credit card with Goldman Sachs, an extensive online discussion started about underwriting (very strange!). The Apple Card, unlike most major credit cards from American Express, Bank of America, or other major banks, does not support Authorized Users. (An authorized user is someone who can use and carry their personalized card for an account but who is not the named owner of the credit line.) The lack of authorized user cards is an odd limitation of the product. (From my understanding, this is a limitation at the underlying processor CoreCard.)

Because there were no authorized users, some couples decided each of them would apply for an Apple Card (no fee, why not?). The dual applications led to couples comparing, in virtually real-time, different credit lines issued to them. Some couples saw the woman in the pair receiving a much lower credit line than the man, even if they had similar scores, shared household income, etc.

For those in the industry, this is not surprising. There is more to underwriting than the pure score. It is improbable any two people have identical credit reports, especially as many credit accounts are not joint (see above).

People love to complain about big brands messing up, and the pairing of Apple and Goldman-Sachs was too much. Complaints and investigations ensued. Now we have an answer from the New York State regulators that there are no signs of violations of the Fair Credit Act. I don't find this surprising. I thought it was interesting to see that more than 400,000 applications from New York residents alone were reviewed. The Apple Card is a huge force in the industry based on that initial application volume. While they don't advertise in all the usual places and miss the 40% of the population that uses Android, the Apple Card went from 0-60 very quickly.

A Rare CardsFTW Post About Cards Being Lame

For a final note this week, I wanted to write about the stimulus payments. The Federal government could be doing a much better job distributing these. While it is true that they have improved, and I will acknowledge it's a huge problem, I think the approach is wrong. As you know, I spend a lot of time talking about how great cards are. They are great for paying for things. They are not great for being paid.

There are three ways the government sends people money:

- Via a direct deposit (ACH) to your bank account

- Via a check

- Via a prepaid card

If the IRS knows your bank account data (e.g., they paid you a refund via ACH in previous years), they are supposed to pay stimulus payments the same way. If not, they sent you a prepaid card.

If you get a prepaid card, the theory is that it's easy to use and there are no check-cashing fees. That sounds good, but the reality is: The government has to pay a service provider (e.g., MetaBank) to manufacture cards, personalize them with card numbers, mail you the card, run a website and phone system to activate the card, service the card, allow you to get cash from the card, etc. Even better, if you lose the card or throw it away because it looks like a scam (the EIP cards are very scammy looking!), you have to call the IRS and ask them to send you a new card, which produces all the cost and waste again.

Once you get the card, you easily request the funds be transferred via ACH to your bank account. Then, without ever using the card, you can throw it away.

Terrible.

If the government is going to keep sending money to people (which it probably will again), it should have a way to register our preferences and avoid the cards. Security is complex here, but you could send a letter first. An ACH for the IRS must cost about $0.01. You can't even mail a plastic card for less than $0.398 (USPS First Class 5-digit automation rate).

We don't have a good national payor system, and we don't have options like a postal bank, as seen in many other countries.

While cards are great, they are not always the answer!

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you're looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.