Co-brand News Dominates - CardsFTW #23

Plus, a "Zero" Card Update and a Glow in the Dark Card

There were heaps of news the past two weeks on the card world, but the announcement of several new co-brand cards stood out to me.

The Wall Street Journal first broke the news that Instacart, the grocery delivery service, signed a deal to launch a co-brand credit card with JP Morgan Chase. This was a hotly contested co-brand card deal. In addition to the news about Instacart, the Journal also reported that DoorDash is in advanced talks with potential issuers about a card.

I predict that this is just the beginning of a slew of new card announcements.

Conventional wisdom over the past few years has been that there would be fewer and fewer co-brand cards available. As the major credit card issuers have consolidated, the number of co-brands has dropped precipitously. MBNA once issued more than 1,000 co-brands, which have dwindled to perhaps dozens at Bank of America post-acquisition. Barclaycard cut nearly two-thirds of their co-brands in the past few years.

In the past year, we have seen a shift in this narrative. Fast-growing technology startups have strong products that benefit from co-brands. Before Instacart, the only major technology startup co-brand credit card that made a big splash was Barclaycard’s Uber credit card. This card hasn’t performed well and it soured the industry overall. Uber is a single brand, however, and it should not be read as an indictment of co-brand cards.

Consumers love brands. Consumers love rewards. Brands love the data, insights, communications, and loyalty of co-brand cards. With so much to love, it feels inevitable that brands will continue to launch more co-brand cards.

Historically, the scale of national card issuers has kept small brands out of contention. Why would a major issuer launch a card that could have 10,000 or 30,000 cardholders when you could use the same effort in terms of time and people to launch a program with 1,000,000 cardholders? A number of startups (mine included) are trying to attack this open space.

As we recently covered, Cardless has launched the Cleveland Cavaliers card. The company is building a Synchrony competitor, with a pure co-brand approach built on a modern fintech stack using Corecard’s processing platform and First Electronic Bank, a Utah ILC.

Deserve, which pivoted from its own cards to being a credit-cards-as-a-service platform provides options for fully hosted white-labels to API-driven experiences. Deserve announced this week another co-brand for OppFi, which will also be issued by First Electronic Bank. Deserve now has publicly announced four different back-end issuers. Three are fintech-friendly banks, as well as the more traditional Sallie Mae Bank.

RailsBank, a European startup, has recently landed on American shores and is working with a number of startups, fintech and otherwise, to launch credit cards. Railsbank takes a purely API-driven approach, relying on partners to build out experiences.

My company, Vertical Finance, works with Deserve for processing and underwriting, while bringing together merchant networks to issue cards that produce co-brand benefits for small to midsize brands across a wider swath of an industry.

In between the fintech companies working on this problem and the major national card issuers are a select few regional banks such as Commerce or UMB which also issue co-brand card programs.

As the economy restarts and the underlying enhancements of fintech infrastructure grow, the demand and capabilities for smaller co-brand cards will grow. We will continue to see many new announcements of co-brand cards (I’ll likely cover them in this newsletter), although we will also see cards fail to gain traction. A few bumps in the road are to be expected, but the winners in all of this will be consumers, who will see more options for their wallet.

Marvel Card

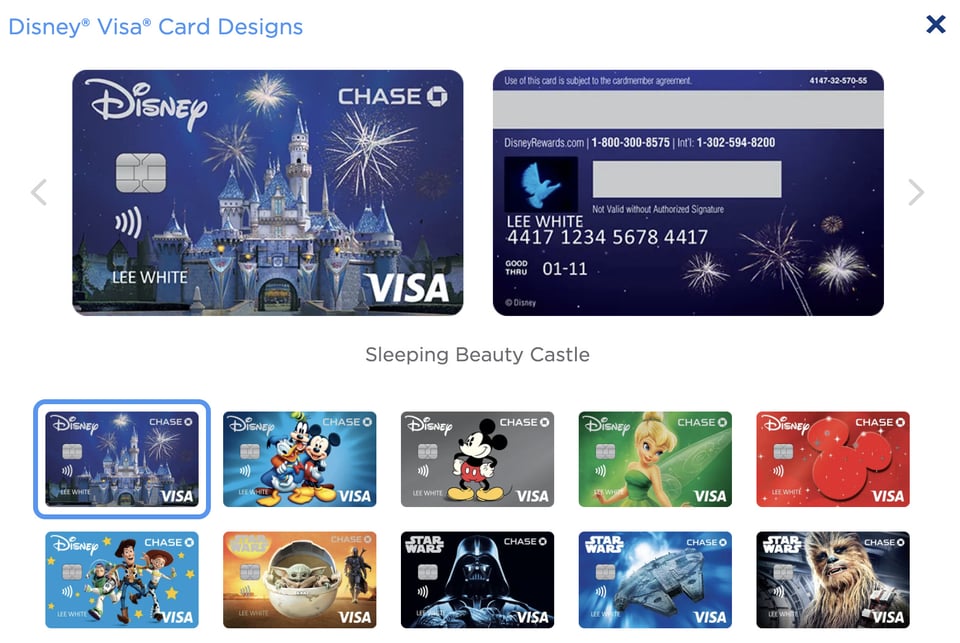

Speaking of co-brand bumps in the road, news broke this week that the Marvel Mastercard, issued by Synchrony, is being discontinued. Comic brand cards are a niche, but both major brands have cards, with UMB Bank issuing the DC Power Visa card. I wouldn’t write-off the Marvel card, however. Disney has a huge co-brand card business with JP Morgan. Given Disney’s acquisition of Marvel since the Marvel card was launched, I anticipate we will see the card (or elements of the program) shift to JP Morgan. The Disney card has eight designs to choose from today, including four from Star Wars. Bringing the Marvel brand in line with this program will surely bring some fun new designs from which to choose!

Rewards Are More Than Points

The other big credit card trend highlighted over the past couple of weeks is the introduction of new challenger credit cards with less-than-traditional points programs. I’ve talked about bitcoin rewards cards in the past, such as BlockFi’s upcoming credit card in CardsFTW #11. In addition to BlockFi, Gemini is launching a cryptocurrency rewards card (see CardsFTW #15).

The Wall Street Journal did a nice review of cards doing things in their Future of Everything series: Credit Card Points: Next Up, Shrink Your Student Loans, Invest in Bitcoin. Sadly, buying wine with rewards was not covered, although I am pretty sure Grand Reserve is quite innovative in that respect. Most of what the Journal covered is not live yet, and some of it has been done before, as I covered recently regarding climate-change focused cards. It is exciting to see both more traditional issuers and newer ones work on new ways to create, earn, and redeem points, because airline miles aren’t for everyone. For an additional take, check out this report by Cheddar on bitcoin rewards.

A Bit More on Zero Cards

The last issue of CardsFTW poked a bit of fun at all of the cards named Zero. Last week Zero Financial was acquired by Avant. Zero Financial originally offered a credit card named Zero, before it pivoted to a neobanking and debit experience using the brand Level. Avant is an online-lending startup focused on the underbanked market. They already offer an Avant-branded card (issued by WebBank) and according to press details, this acquisition is more about the debit product than the credit one. Maybe someone reading this newsletter will have more insight, but from the outside the Zero card product, which was an interesting set of features, appears to be set aside.

Zero created a sort-of multi-level marketing aspect to its rewards, enabling those who referred new users to earn cash back at a higher rate. This is an interesting take but creates some negative incentives for new users, who are stuck earning the lowest rate and may be hard to retain. As you referred or spent more, you earned more:

Quartz members (the base membership) get 1% cashback, and can level up to Graphite (1.5%) for referring one friend OR spending $25,000, Magnesium (2%) for referring 2 friends OR spending $50,000, and Carbon (3%) for referring 4 friends or spending $100,000.

The Zero card also allowed users to earn credit-level cashback while experiencing debit-style payments with immediate debits from a checking account as the credit transactions settled. This debit-style credit card has been tried before as a stand-alone app by firms such as Debitize (since acquired by Trim), but none have gained true market scale.

Innovations in Plastic

Pundits enjoy making fun of card design (“why does anyone need a metal card?”), but the reality of consumer behavior is that people love well-designed cards. European neobank Revolut announced a new glow-in-the-dark card.

I love it. It’s fun!

Your Drug Store is a Bank Branch

Finally, Walgreens announced that, in addition to the upcoming credit card product announced last year, they will be launching a Walgreens branded bank account and debit card program. The card will be issued in partnership with InComm (famous for Vanilla Visas and all the calling and gift cards) and issued by MetaBank. Like the credit card (which will be issued by Synchrony), the card will be linked to the Walgreens reward program.

When I first joined Green Dot in 2006 Walgreens was our biggest partner. Green Dot was the exclusive provider of reloadable prepaid debit cards at Walgreens. We enabled un/underbanked consumers to deposit cash at Walgreens, which were in every neighborhood and many open expanded or 24 hours per day. That cash could be secured on a card, used online, taken back out at an ATM, and more.

I remain skeptical that there is a brand audience for Walgreens, but bringing this analysis back to the point at the start of this newsletter: more choice is a good thing. Perhaps there are ultra-loyal Walgreens customers who love this rewards program enough to get a card. What I do know is that anyone who worked at Green Dot back in the day (or even now?) must be shuddering not to have this contract.

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.