Family Finances - CardsFTW #24

Plus, Another New Challenger Card, More CLO Moves, and Instant Issuing

Welcome FTT Readers

A quick welcome to many new subscribers who joined after reading the first part of a credit cards report I developed with Cokie Hasiotis at FinTech Today. I hope you enjoy CardsFTW.

If you’re not familiar with FinTech Today and want to read about credit cards-as-a-service, check out Part I on their Substack.

Apple’s Take on Authorized Users

At their spring announcement event, Apple announced an interesting take on family finances with the Apple Card Family. (They also announced the return of the orange iMac, which I surely don’t need, but definitely think is a beautiful sculpture.)

One of the major frustrations with Apple Card since its launch is its lack of authorized users. Most credit cards support this feature, which allows the primary cardholder to issue additional physical plastics for additional cardholders. In the traditional feature only the primary cardholders hold responsibility for the line of credit. The authorized users can spend against that line of credit, but do not pay a separate bill or have their credit checked. The issuer will report the authorized users status to the credit bureau.

Most processors and issuers don’t support multiple card numbers per account. As a result, the cards issued to the primary user and authorized users share the same number. There is no way to differentiate who made which purchases. A notable exception to this among major issuers is American Express, which creates a unique card number for each user and shows charges by card its statements and online transaction views.

Some issuers also support co-owned accounts, which are different from authorized users. In a joint ownership structure, the credit of both applicants is taken into consideration and both have repayment responsibility. Which banks support joint ownership is not easy to discover. From personal experience I can say that you can call certain major issuers (such as Bank of America) and add a joint account owner. This allows both owners to make changes to the account and is a level above authorized user.

The new Apple Card features are the first major enhancements to the card since its launch less than two years ago. The way Apple is implementing authorized users is a very classic Apple take on a feature. Rather than simply implementing an industry-standard feature of authorized users with additional cards, Apple is bringing some meaningful family-based finance features into the forefront.

The Apple Card will now allow for both joint ownership and for authorized users. If an existing couple each have their own Apple Cards, they will be allowed to merge the accounts in a best-of-both-worlds way, by combining the separate limits into a new higher one and taking the lower account APR.

Cardholders can also add up to five people as authorized users for, including children aged 13 and up. The card will be deployed via Apple Wallet on a device, although it is unclear if additional physical cards will be issued. (The Apple Card is designed such that, despite using a super-high-end titanium card, you don’t really want to use the physical card ever. Mine is in a drawer somewhere.)

For authorized users who are 18 or older, but who are not joint owners, Apple will also report account activity to the credit bureau.

In their announcement Apple emphasized the family aspects of the new capabilities. Family finance is a growing area in fintech. Most neobanks and challenger cards start out with a single user in mind and slowly migrate into support joint ownership. Joint ownership is more complicated to manage and some processors may not support the underlying structures required. There are a number of fintech apps that are specifically focused on the topic such as Zeta, HoneyFi, HoneyDue, and others. These vary from pure personal finance management tools to full-fledged accounts.

Apple is bringing some of these management features to the credit side with the ability to provide spending details by user, sharing payment responsibility, and credit reporting. I’m excited to try these features which should be released shortly with the next iOS upgrade. Even more, I hope that this helps encourage some other larger issuers to provide more detailed authorized user reporting with their credit products.

Apple Knows You Use Other Cards

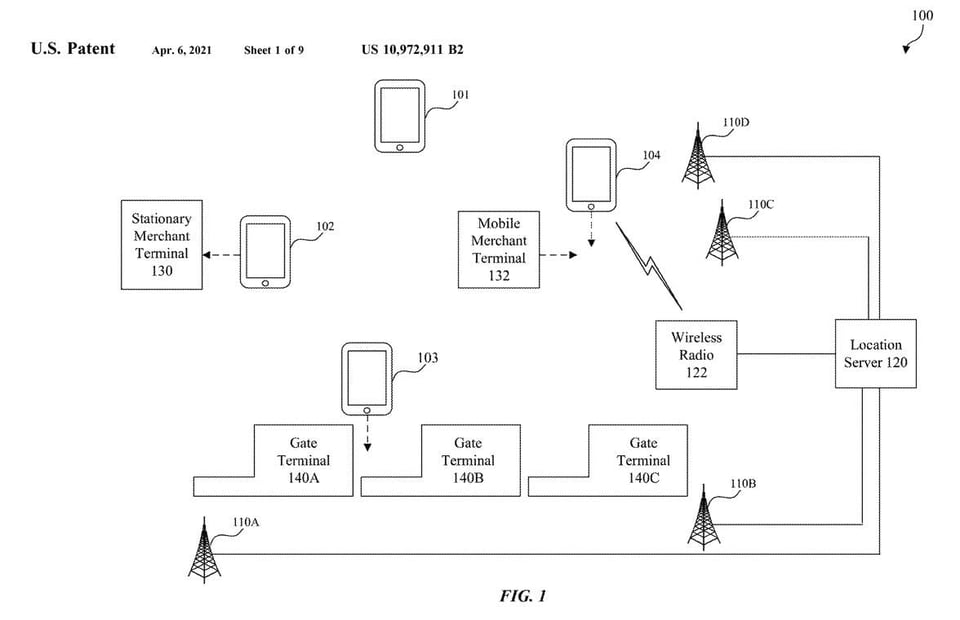

Before moving on from Apple, I wanted to highlight this recent Apple patent that could enable Apple Pay to intelligently select the right card to pay for at the point of sale. If you know me at all, you know I spent many years on this concept while starting and operating Wallaby. We even attempted to file our own patent around such a service, but didn’t put enough hardware into the flow to get it granted. A patent is no guarantee of implementation, but all of the elements of smart card intelligence are coming together here.

Given ultra-precise location awareness in modern phones, coupled with signals from bluetooth low energy beacons or other wireless technologies, a point of sale terminal could communicate a merchant’s name and category to Apple Pay. This would allow the wallet to pull up loyalty cards or payment cards intelligently. We did some of this at Wallaby for recommendations, using location awareness to push an alert to users. For example, as you pulled into a gas station, we could send an alert to remind you to use your best card for gas rewards. This worked really well (once we finally got it working after many tries and some very amusing card suggestions at Disneyland) and was one of the most delightful features of Wallaby.

Making the decision based on rewards rules is hard, though. There is a lot of data required (and ongoing maintenance). In addition, issuers will likely push back, as they don’t like steering (recommendations of which card to use by a wallet, as it may discourage usage). If anyone can do it, Apple can. I would be happy to help! I know exactly how to build a card optimization engine. Give me a call.

Gas Cards and Decoupled Debit

Speaking of spending money at gas stations, this item isn’t news related but a topic that’s come up in a few conversations of late. Many tech companies want to get involved in a user’s transactional payments without having full responsibility for either extending a line of credit or maintaining a deposit account. A decoupled debit card is a way to do this. In decoupled debit, the cardholder carries a debit card that is immediately funded per transaction or daily by a corresponding ACH debit from an underlying bank account. There have been a number of attempts around this such as Debitman, which was renamed Temp Payments, but ultimately could not survive the regulatory challenges of the Durbin amendment. The most successful of these products is Target’s Red Card debit product, which provides users with a Target payment card that is funded directly by their account, for those consumers who don’t have or want to open a Target credit line.

GasBuddy also operates a decoupled debit program, with the Pay with Gas Buddy. With this product, consumers can save at gas stations that fund extra cashback in exchange for forgoing the credit card fees. The Gas Buddy card is directly funded by the underlying bank account. More startups should explore how a feature like this might help them achieve their goals without requiring their users set up an entirely new account.

Unifi Launches a New Challenger Card

Unifi Money is an early-stage neobanking brand targeted at affluent consumers with a full-featured financial experience across deposit, trading, and now credit. Unifi is building on RailsBank’s credit-cards-as-a-service platform and looking to launch their product in the third quarter.

Unifi’s branding is very much about poking fun at major banks and “traditional” financial marketing. The card has no signup bonus, but pays a very high rate of rewards at 2%. The rewards can be redeemed for bitcoin, gold, or equities (presumably through their built-in trading capabilities).

The Unifi Premier Credit Card page has few details, but additional details were disclosed to Business Insider. The card will have an annual fee (which can be waived with enough annual spending). I get the flat-cash back rate approach, but I don’t think that limiting rewards to investments and having an annual fee necessarily puts the card in the super user-friendly category.

Based on research I’ve consulted and my experience in the space over the past 15 years I would say that there is a pretty even split between consumers who enjoy the game and the possibilities of points-based rewards programs, and those that want cash back. There is a similar split between people who care about a nice looking plastic (or metal) card and those that don’t.

I am very skeptical that people frequently switch from one camp to the other and marketing on that basis strikes me as off-target. If you want to have a flat rate, plastic card, great! Find those users. If you want to have a rewards program and a metal card, that’s also great for other people. I don’t get the negativity-based marketing of these items. I might think rewards in gold is a terrible idea, but I wouldn’t market my points based card “not having gold-based rewards.”

As always, the market will tell us if this feature set is compelling. There is something here in the approach, but it will be a challenge to grow a premium cardholder base without signup bonuses. People are too used to it and it is an expectation for this group of users

Gap Switches Cobrand Issuers

Clothing giant Gap announced that it is moving its cobrand card program to Barclays and Mastercard from Synchrony and Visa. The change will take effect in May 2022 and is a major brand loss for Synchrony, which also lost its Walmart card relationship to Capital One about two years ago. According to the Wall Street Journal, the Gap portfolio is approximately 11 million cards with $3.8 billion in outstanding balances. Synchrony has been the brand’s issuer for 22 years. The Gap is a top-five client for Synchrony, but represents just 5% of outstanding balances.

Gap has been working aggressively to reinvigorate its brands, which include Old Navy and Banana Republic. The new cards will tie-in more closely to a new rewards program Gap launched last year. In addition, Gap sought more guaranteed revenues. Broadly speaking, many retail cobrand cards have had limited loyalty tie-ins. The easier financing and some built-in enhanced reward was deemed enough. This is no longer the case and retailers are enhancing their rewards and loyalty programs. To make the most out of rewards programs, they must be integrated into the credit card offering. As a high-frequency wearer of their polo shirts, I am excited to see what the new Banana Republic card offer will be!

Another Acquisition by Cardlytics

Following hot on the heels of their acquisition of Dosh, Cardlytics announced it will acquire Bridg. Cardlytics is the giant in the card-linked offer space, which provides cashback or extra rewards to consumers for shopping at a specific merchant with a specific card.

I didn’t see this one coming, but, on a personal note, congratulate Amit, founder of Bridg, and my former MuckerLab Accelerator Winter 2012 classmate. I think Bridg is the largest exit for that cohort. After thinking about the possibilities more, this acquisition opens fantastic new possibilities for Cardlytics.

Credit card issuers are limited to what is called level two data. This is the merchant name, amount, and date that detail a transaction on a payment card. The issuers do not have access to level three data, which would include the specific items or products purchased. Level three data is the ultimate goal and it tells you what the consumer is buying not just where.

For a card-linked offer at a single brand merchant, such as Starbucks or the Gap, knowing where the consumer is shopping is enough to drive an offer. Starbucks can fund the 5% discount for the offer because they know if $10 is spent at their cafe, they earned the revenue.

However, if you are a consumer packaged goods company that sells products at a merchant (think Proctor & Gamble) you can’t use traditional card-linked offers. When a user spends $100 at Safeway, you don’t know if that money went to any of your products or another producer’s.

As a result, we have seen the rise of receipt scanning or loyalty-integrated discount apps which allow a CPG company to directly discount or reward a consumer for a specific item (much like a traditional coupon) through acquiring the level three data outside of the payment network. Along with this, though, comes a meaningful amount of consumer friction to scan receipts.

Bridg’s market platform connects advertising directly with point-of-sale integrations to understand specific products purchased based on advertising. If Cardlytics can combine that point-of-sale data with their portfolio of issuer relationships, they will be able to unlock the large CPG marketing budgets to create card-linked product specific offers. This would be very powerful and create a step-change in the usefulness of card-linked offers, which today suffer from limited variety. Watch out for new discounts on a card in your wallet.

A New Instant Issuance Platform

It keeps getting easier to create your own debit cards. I’m very excited about the announcement by fintech Apto Payments of the official launch of their instant issuance platform, which you can try now. Apto is led by Meg Nakamura, who is a fintech OG and previously brought the first bitcoin enabled debit card to the market, almost a decade ago. I had a chance to preview the Apto platform a few months back and I think it will rapidly become a platform of choice for companies looking to add debit and deposit capabilities to their products.

A US Card for a UK Football

Cardless, the early-stage fintech card issuer aiming to take on Synchrony, announced its second cobrand card deal, this time with Manchester United. Cardless is going all-in on sports co-brands, with the ManU card joining their existing Cleveland Cavs card. I know ManU is a huge global brand, but I am skeptical of the number of US-based consumers who want a ManU credit card. It is an interesting first though, with most cobrand cards existing only in the home country of the brand, with a few travel card based exceptions, such as the US British Airways Card from Chase or the Korean Air SkyPass card from US Bank. Will this be the first of many football cards in the United States? I’m doubtful, even major MLS teams are lacking cards (although Canadian MLS clubs have cards via Bank of Montreal).

CardsFTW

Thanks for reading CardsFTW, a weekly newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.