New Cards Debut, Clouds Form Anyway - CardsFTW #34

Plus, the now usual BNPL update

An exciting past week in cards land, which saw several significant new card debuts, news of Apple’s entry into buy-now-pay-later (BNPL), and mixed messages on how consumers will use credit in the coming months.

A Sharp New Card

While rewards cards often dominate the news, Chase launched their new interest-rate focused card: Slate Edge. The new card replaces Chase Slate, which closed to new applications in early 2020 amid the early days of the pandemic. The new card’s key feature is an automatic interest rate reduction. Cardmembers can have their going APR rate reduced by 2% each year if they pay on time and spend at least $1,000 per annum. Rates start at 14.99 - 23.74% for new applicants (with a 0% introductory rate for both purchases and balance transfers) and can be reduced to Prime plus 9.74% (12.99% as of today).

Chase often introduces new cards with a very strong signup offer, and this card is no exception, with a $100 statement credit on $500 in purchases within six months and no annual fee. Signup bonuses are usually rare or limited for low-interest cards, and combined with a 0% introductory APR; they are firing on all cylinders.

Chase also promotes an “automatic review for a higher credit limit” within six months with $500 in spending, although most major issuers automatically review limits anyway. (Making this promise will at least require it to be done consistently to maintain compliance with the marketing offer.)

The online reviews were mixed, with some folks noting that you can likely get a better APR from a credit union. The credit union argument does not persuade me as Chase Slate Edge looks to accept scores 690+ whereas most low APR credit union cards live in the 720-750+ range. In addition, data show that Americans are not very likely to consider credit union cards.

The new Slate Edge card reminds me of the SoFi Credit Card, which launched at the start of the year. That card features a 1% APR reduction after 12 monthly on-time payments with no spending minimum. The SoFi card also earns up to 2% cashback towards SoFi investment or loan products. No signup bonuses are available for SoFi.

It’s encouraging to see a large issuer innovate in the good credit and low APR space with meaningful incentives for better financial behavior rather than a pure rewards focus. Slate was a popular card sidelined due to economic uncertainty, and the relaunch is appealing.

New, but Not Really New

On the other end of the credit spectrum, Bank of America launched a new card, the Unlimited Cash Rewards Credit Card. BofA appears to be making a number of card moves, with the recent rebranding of their other cash rewards card to Customized Cash, featuring a 3-2-1% earnings setup with a choose your own category feature.

The new Unlimited Cash Rewards card earns 1.5% cashback on all purchases and is basically the same card as their Travel Rewards Card. I don’t understand why this positioning exists or works for consumers. Still, the Travel Rewards Card also earns 1.5% cashback, but only when you use that cashback as a statement credit towards travel purchases. (If you use the rewards for other cashback options, a discount factor is applied to reduce the value.)

In addition, Bank of America’s strong relationship rewards program applies here. Through their Preferred Rewards program, customers can earn 25-75% bonuses on their earnings by maintaining certain assets at Bank of America or Merrill Lynch. At its highest level of 75%, which requires $100,000 or more in deposit at either BofA or Merrill, customers earn 2.62% cashback on every purchase, which is quite hard to beat, especially with no annual fee.

This card also includes a $200 on $1000 spend signup bonus and a 15 month 0% introductory APR on purchases and 60-days on balance transfers.

While some noted that 2% cards are growing in popularity like Citi’s Double Cash and Wells Fargo’s Active Cash, the Bank of America offering is strong and market-winning when held by a Preferred Rewards customer.

The Travel Rewards card continues to be offered, with a higher signup bonus ($250) and similar introductory purchase 0% offer (12 months), but no balance transfers. The other difference is that the Unlimited Cash Rewards card has a 3% foreign transaction fee, while the Travel Card does not.

On review, while the new card sounds more appealing due to its flexibility, it carries additional fees the Travel Card does not. Many purchases are eligible under the travel designation, such as parking and museum fees. In the end, this card is new-ish but neither marketing-leading nor that different from its sibling.

Citi Switches Tactics

Last week, I talked about American Express’s continued upmarket moves on Platinum and some of the very high-end cards. I had noticed at the time that Citi’s ThankYou Prestige $495 annual fee card didn’t appear to be offered on Citi’s website anymore. I didn’t dig in, but this week saw confirmation via Bloomberg that Citi is discontinuing the card with no replacement at the current time.

Current cardholders of the Citi Prestige card can continue using it, but Citi appears to be focusing on its new Custom Cash Card.

The Citi Prestige was popular among travelers due to a feature enabling a free night on hotel stays of four nights or longer booked via the Citi travel portal. Over the years, as consumers gained skill using this feature, Citibank put more restrictions in place. Overall, this card was always a distant third in the volume compared to the American Express Platinum and the Chase Sapphire Reserve.

As with Chase’s Slate Edge product, more consumers need solid, everyday, and credit building cards than need $500 per-year-plus rewards cards. Leaving that market and focusing on America’s core should serve Citi well.

Zero Card with a Non-Zero Annual Fee

I covered the initial waitlist announcement from neobank Aspiration in March. Additional details are out now from Aspiration on this card will work. Bear with me; it’s a bit complicated.

Aspiration will plant one tree for each purchase. They will also plant a second tree if you enable round-ups on your purchases (e.g., a $27.80 purchase becomes $28.00, and the $0.20 is used to plant a tree).

The trees planted metric is also used to calculate your spending rewards. Plant 60 trees (60 purchases or 30 purchases with rounds-ups) and earn 1% cashback. Miss the mark and earn only 0.5% cashback. Thirty purchases is a lot. American Express’s Everyday CreditCard gives you a 20% bonus on rewards (2x at supermarkets, 1x everywhere else) when you use your card 20 or more times per billing period. 20 is a substantial burden as well. I think you can expect 7-15 purchases per month on a credit card to be the average state for a card unless a consumer uses that card all the time.

Assuming cardholders don’t hit that threshold all of the time, the card has a very weak rewards structure. It also has a $60 annual fee. There are reports of some waitlist members receiving a signup offer of $300 with $3,000 in spending, although the card is not yet open to full application access.

I think if you want to plant more trees, you could probably go with a 2% cashback card and just use your cashback to fund planting, which anyone can often do for $1 per tree planted.

The economics available to fintech companies working on issuing credit cards is very tough. We’ll continue to see these cards have annual fees (at least at launch) as the companies attempt to make these cards at least breakeven.

Social Rewards

Speaking on fintech credit card issuers, startup Jasper Card (formerly CreditStacks) announced a significant fundraising round and a new product launch. CreditStacks, like Deserve’s consumer product, was initially focused on alternative underwriting enabling access to credit for recent immigrants who do not have an established credit history in the United States.

While the new Jasper Card continues to use alternative underwriting, the rewards program has been revamped to focus on a referral program. The card earns a baseline cashback rate of 1%. Cardholders can earn a 1% increase in the rate for a year for each friend whom they refer to the card who is successfully approved (maximum of 6% cashback, or five referrals per year).

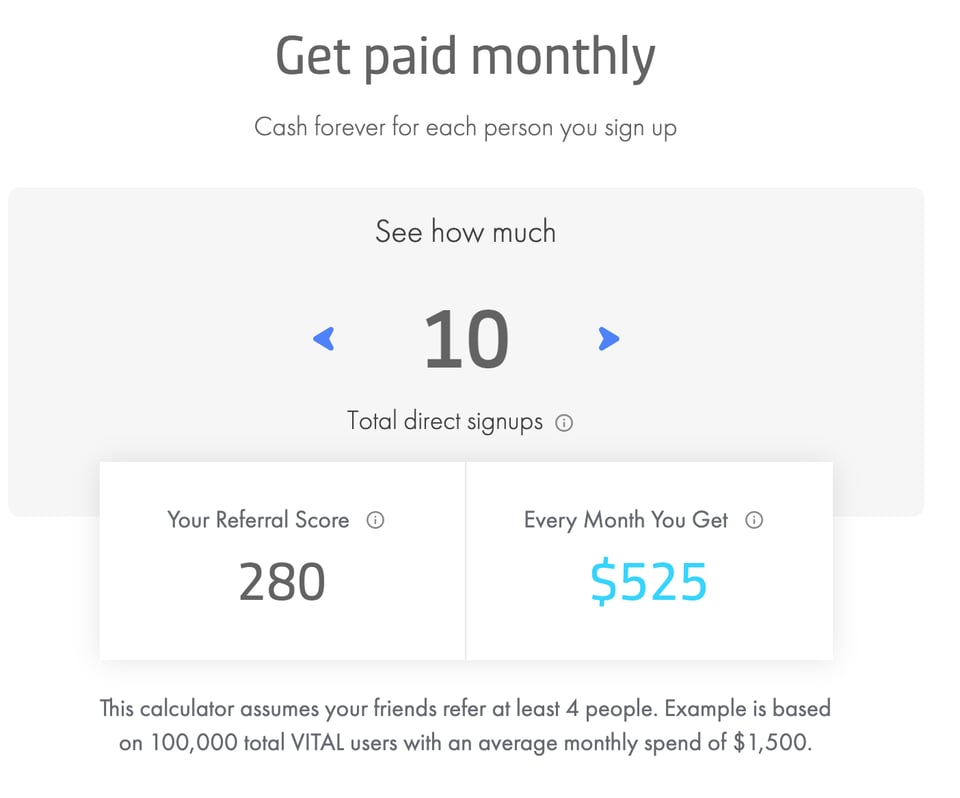

Jasper will face some social competition shortly from Vital Card, a pre-launch startup that bills itself as the “world’s first social credit card.” (Disclosure: I couldn’t resist making a small investment in Vital’s crowdfunding campaign via StartEngine earlier this year.) Vital isn’t quite as clear as to how their referral program works, but you earn points for referring friends in a multi-level marketing style setup, and a pool of referral fees is paid out to users. Vital’s website makes some intense claims about how big this could get, which I’ll show you here:

A lot of assumptions go into this. $525 per month would be impressive if true but seems very unlikely. I doubt this consumer demographic will spend $1,500 per month on the card.

Mixed Messages

As the economy restarts, stutters, and starts again following the pandemic, the business of credit cards has been under pressure. Various reports over the past week have shown substantial mixed messages. American Banker reported flat credit card growth at Chase. Consumers are carrying less debt, which limits earnings on the borrowed money. People are spending the same ($141.8B in 2Q21 vs. $141.7B in 2Q20) but paying a higher rate of spending back.

Meanwhile, over at Citibank, card purchases in North America were up 40% year-over-year. Similar to Chase, however, card loans were down 4%, again reflecting higher repayment rates.

According to the Financial Times, as this shift in consumer behavior pressures margins, banks are pressed to increase investments in marketing and technology to combat the rise of fintech challenger providers in the debit and credit space.

Buy-Now-Pay-for-it-Later

Finally, this week, the big news was that Apple is launching its own buy-now-pay-later service, aptly dubbed apple Pay Later. Many others have covered the details, but key points include that you do not need to have an Apple Card to use this. It sounds like it will be available in any Apple Pay transaction (replacing the use of your existing card products at the immediate time). I’m a bit fuzzy on the details, but it appears that consumers could pay their Apple Pay Later bill with one of these same cards (unless, of course, the issuer prevents it, as Capital One has with many BNPL companies).

The real point here is the proliferation of buy-now-pay-later options. I saw an Afterpay sign on the doors to my local Container Store this week. BNPL is everywhere, much as store financing always has been.

Consumers should watch out, though. Just as credit cards get you deeply into a debt problem, so can BNPL. This past week, the CFPB published a blog post warning consumers about how you really will pay for it later. The authors point out that you can still overextend yourself, have late payments reported to the credit bureaus and pay fees and interest. On the flip side, compared to credit cards, BNPL options don’t include Federal and industry-standard protections like disputes and return/warranty extensions. Consumers often don’t realize the value of dispute and credit protection until they need it, but that may be one vote in favor of the fixed repayment schemes on a card versus the Klarna and Affirm-style BNPL options.

CardsFTW

Thanks for reading CardsFTW, a weekly-ish newsletter about all things debit and credit. CardsFTW is written and curated by Matthew Goldman, Founder, and CEO at Vertical Finance, a challenger credit card startup. If you’re looking for insights into everyday payments beyond deal blogs, please subscribe for free at cardsftw.substack.com. If you enjoyed this, please share it with a friend! Follow me on Twitter @magoldman.