End-of-Year CFPB Excitement - CardsFTW #137

Plus, Bernie Sanders hates risk-based pricing and more

Happy New Year, CardsFTW subscribers! I enjoyed a brief vacation from writing the newsletter and am feeling energized and ready to get back to work for what looks to be an exciting year in cards and payments.

If you haven’t lately, now is a great time to forward CardsFTW to a curious colleague or friend who is interested in cards. They can subscribe for free or get a paid subscription for more of our deep insights coming later this year. On to the news and analysis…

Squeezing in those last Biden-era CFPB moves

Who knows what the next four years will bring for the Consumer Financial Protection Bureau? It’s probably not aggressive enforcement (count that as an official 2025 prediction). The CFPB has been hard at work through the end of the year, pushing out a number of enforcement actions, lawsuits, and more, most of which I will not cover here. However, two key updates are right in my area of interest.

Credit Card Finder Tool

First, the CFPB launched its long-anticipated consumer credit card finder tool on its website. I can’t find documentation, but I think they’ve been hinting at doing something like this since the early 2010s when the agency was nascent. The tool is built on data that card issuers must, by law, submit to the CFPB with full credit card terms and interest rates.

I love this data set. When I was operating Wallaby, we used the CFPB data to find out how cards really worked since it is surprisingly hard to find the terms and conditions for a credit card that isn’t in your wallet. The dataset here should represent the superset of all known cards you can apply for in the U.S., but (at least 10 years ago) it was not complete as it didn’t include cards that were active but weren’t accepting applications (e.g., deprecated products) nor did it properly account for cards that may operate on a single cardholder agreement, but with different tiers of rewards.

The new tool is positioned as a consumer-first, unbiased marketplace. However, it has some major flaws. First, the data will rapidly be outdated as these terms are snapshots provided periodically by law (every six months), not real-time updates as rates change (especially important in today’s market). Second, there is too much data!

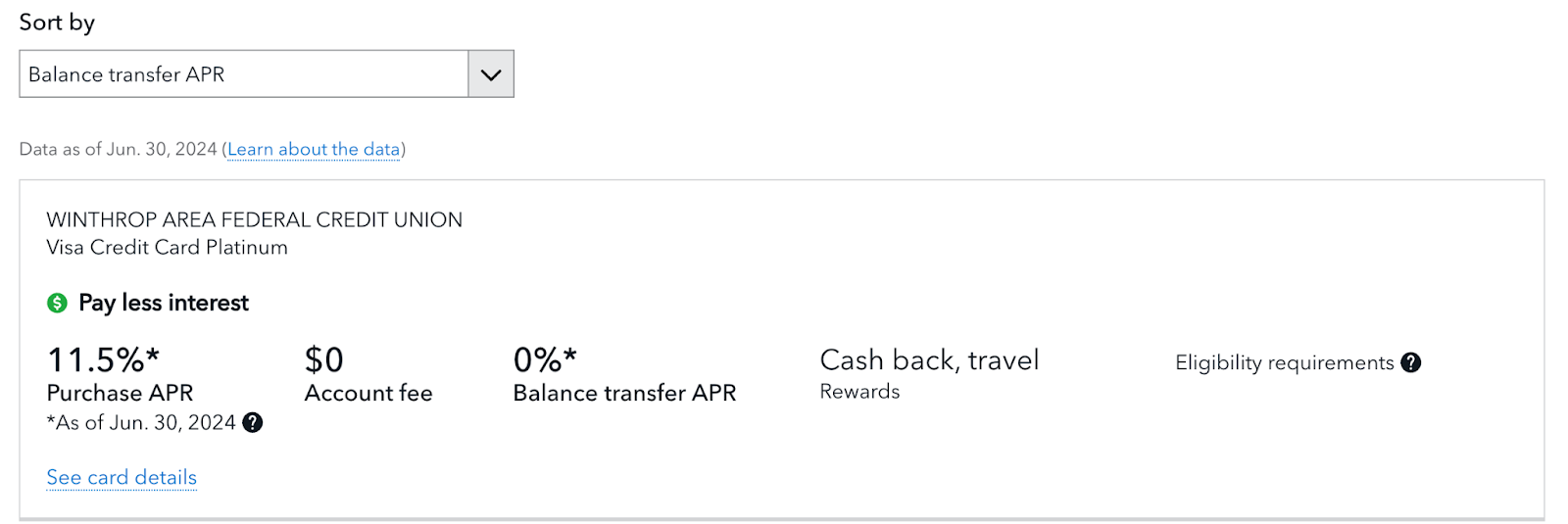

The underlying dataset includes 638 cards, which is a lot, but it isn't comprehensive. My friends at Kudos* have more than 3800 card profiles in their system. Even if I filter for folks like me (excellent credit, California), I get 349 results, and many of them are for credit unions for which I don’t qualify:

It’s not very helpful.

I think it is important that credit card comparison sites disclose their incentives and structures. We know that some are based purely on how much their partners pay, while others have a stronger editorial independence line. We also know that these sites don’t want to put the effort into listing smaller cards because it creates a risk of them having out-of-date data. I suppose the CPFB isn’t going to fine itself if its website is wrong.

I don’t think this tool is going to be a big win, and it is likely not a great use of resources. I don’t see why they didn’t just stick with posting the data set for others to use.

Rewards Circular

The CFPB published a circular on December 18th on the topic of rewards. Nothing ground-breaking here: the CFPB says you shouldn’t use bait-and-switch tactics. OK. Isn’t this all covered by existing UDAAP rules? This circular was released alongside the credit card finder tool, which doesn’t provide much insight at all into how rewards work. Don’t worry, there are plenty of blogs and Reddit forums for this.

This was one post that I particularly enjoyed:

Question Presented: Can credit card issuers violate the law if they or their rewards partners devalue earned rewards or otherwise inhibit consumers from obtaining or redeeming promised rewards?

Response: Yes.

OK, did anyone actually think otherwise? Not sure what we’re trying to say here that’s new.

The Chevron Card, It’s a Gas

Speaking of rewards cards that aren’t usually on sites like Nerdwallet or WalletHub: The Techron Advantage Credit Card from Synchrony. Chevron and leading co-brand issuer Synchrony announced an extension of their 17-year(!) partnership for this card.

People LOVE gas cards because the price of gas is volatile, and 10 cents sounds like a good deal, even when it isn’t anymore. I suppose it depends on where you live; however, at today’s AAA-reported average of $3.064 per gallon, a 10-cent discount is just about 3%. There are other cards with 3% back on gas every day (and at every station), and many rotating quarterly category cards use gas at least one quarter for a 5% discount. I prefer the flexibility, but maybe you love Chevron? I mean, the cars are cute.

Bernie Hates Credit Cards

OK, Senator Bernie Sanders not liking credits isn't exactly news, per se. Well, neither does President-Elect Trump. Sanders wrote on Twitter:

During the recent campaign Donald Trump proposed a 10% cap on credit card interest rates. Great idea. Let’s see if he supports the legislation that I will introduce to do just that.

Capping credit card interest rates sounds like a good idea, but I don't think it really is. Credit cards work today through risk-based pricing, which was popularized by Capital One in the 1990s. As PBS Frontline notes:

By identifying lower-risk individuals in high-risk groups, Capital One was able to market to reliable consumers other companies wouldn't touch, says Meyer. In just six years, Capital One became the sixth-largest credit card issuer in the country. "When others were attacking the market with blunt instruments, Capital One used a scalpel," says Meyer.1

By charging different customers different rates, banks are able to balance risk based on each customer's individual profile. A cap will lock many (if not most) higher-risk customers out of the credit card market, thus forcing them to other loan types that carry higher rates.

My 2025 prediction: This is dead in the water.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.

- Becker, A. (2004). The Battle Over "Share of Wallet". PBS Frontline. ↩︎