More Than Just Points - CardsFTW #152

Plus, Merger & Acquisitions, Gaming Cards, and More

Deserve’s Demise

I rushed last week to include a small note on Intuit’s acquisition of Deserve into the newsletter, but didn’t have a lot of time to think about it more deeply. Many people have sent me thoughts along the lines of “well, this is bad for the industry.” I don’t agree, so I thought I would spend a few paragraphs here explaining why I don’t think it is bad.

Technology companies often suffer from a first-mover disadvantage. As general consumers in the world, we often don’t realize this because we might only have encountered a second-mover company. However, many of today’s largest technology brands are not the original inventors of a business model and those original folks are forgotten. Facebook was not the first social network; Google was not the first search engine; Apple was not the first personal computer maker. Many of these companies make their money from technologies or products invented elsewhere. We don’t talk about Friendster, AltaVista, or VisiCorp today. However, their innovations live on.

When Kalpesh Kapadia founded Deserve in 2013, it was called SelfScore. This 2014 FinovateFall demo showcases what they were up to at the time:

The company described itself as a consumer analytics company in financial services. They did not issue a credit card and were not a credit card platform. By 2019, the company pivoted to offer its Deserve branded cards. While these are no longer in market, you can read about them on SuperMoney.

In May 2019, my Vertical Finance co-founder, Sam Nebrich, attended CardForum and met Kalpesh, who was offering a B2B platform, described as “a complete end-to-end turnkey Credit Card as a Service (CaaS) platform.” Deserve’s first partner was student loan issuer and bank Sallie Mae. Vertical Finance was Deserve’s first API-driven customer, launching the Grand Reserve World Mastercard in mid-2020.

Today, there are a half-dozen technology companies providing credit card capabilities. (Read about them in our annual market report.) It is big news in this industry that Deserve’s people and some assets were acquired by Intuit. Customers are reporting that Deserve will no longer service their programs and they need to find new partners (I can help!) It is a change, but I do not believe that it bodes poorly for the industry. Deserve paved the way for many other companies, who are powering important card programs across fintech, retail, and travel brands.

Category Accelerators Aren’t Enough

I spend a lot of time discussing with my clients and others in the industry how to make rewards earning and spending opportunities that will drive irrational economic behavior by cardholders. People already tend to overvalue points: you might take a survey for 500 points (worth $5) that you wouldn’t take if offered $5 in cash. When you are building a card that has a category-specific earning accelerator (e.g., earn 3x points on all wine and wine-related purchases) you have to get people to also spend in the base category. Otherwise, your card will be used only in specific circumstances and your program profitability will suffer.

When we were building the Grand Reserve card, we had a fairly common structure with top-tier earnings at card partners, 3x in our category of wine (and restaurants), and baseline earnings everywhere else. We saw decent baseline spend (e.g., around 30-40% of total spend) in early days, but much of this appeared to be driven by our signup bonus (earn 50,000 points when you spend $3,000 in the first 90 days).

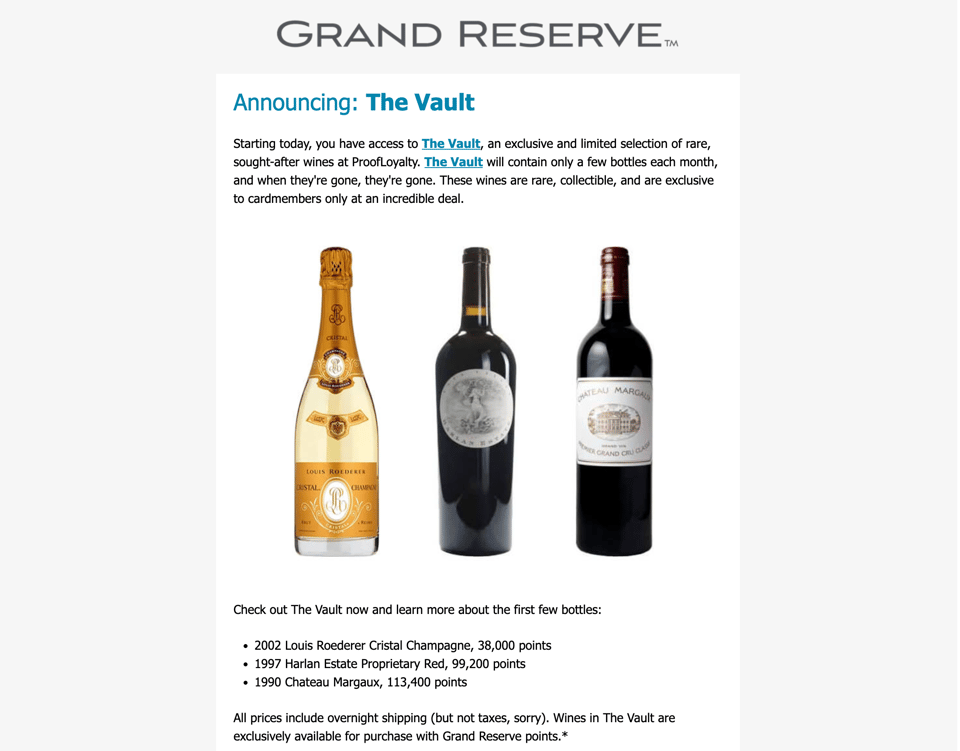

In order to drive more spend we needed to create something truly special for point redemptions. We launched the Vault, which offered ten totally unique and valuable wines each month in our rewards catalog at very good deals. One example was a Harlan Estate bottle valued at $1,200-1,300 dollars, but available for just 100,000 points. Once we created this reward opportunity, cardholders’ spend outside of our accelerated categories jumped to more than 50% (and we saw a ton of activity in our referral program).

The Vault was great because it was a combination of valuable, unique, and aspirational rewards, with a time-and-quantity-limited FOMO factor. The Vault often sold out in hours. One cardholder even accused us of faking the whole thing because people couldn’t get their hands on bottles. (It was not fake! People jumped on it so fast!) Because you never knew what would be in the Vault each month (nor exactly when it would open), but you did know the rewards would cost 50,000 - 150,000 points, each cardholder had a huge incentive to amass points just in case.

The redemption side is half of the story. The earning side also creates opportunities for innovative constructs. We have seen a number of folks on the debit side play around with randomized earning (e.g., Yotta, Long Game). You can imagine random transactions being free, bills being waived for a month, or other options. At scale, a reward such as “one person a day gets all their purchase transactions free” is very affordable for a card program.

The credit card industry is extremely competitive. Challenger brands must think outside the typical guardrails of 3/2/1 card earnings to create truly compelling products.

Gaming Cards

Speaking of gaming cards, First National Bank of Omaha and MGM Casinos launched the new MGM Rewards credit cards this past week. The new the MGM Rewards™ World Elite Mastercard® and the MGM Rewards™ Iconic World Elite Mastercard® join other gaming brand cards like the Unity by Hardrock Mastercard (see CardsFTW #135), the Caesars Rewards Visa Signature Card from Comenity Bank and the Edge Boost Visa Debit Card.

As far as I can tell, the new MGM cards replace a prior MGM Rewards Mastercard with the addition of the higher-end Iconic World Elite card product. I’m not a close follower of these products as I don’t gamble, but like many co-brand products these only make sense to me if you are a huge spender at these particular properties.

One might also argue that some cruise ship cards count for gaming cards too, as there are on-board casinos. Major cruise lines like Royal Carribean, Carnival, Princess, and Norwegian all offer co-brand travel cards as well.

It’s Happening: Discover + Capital One

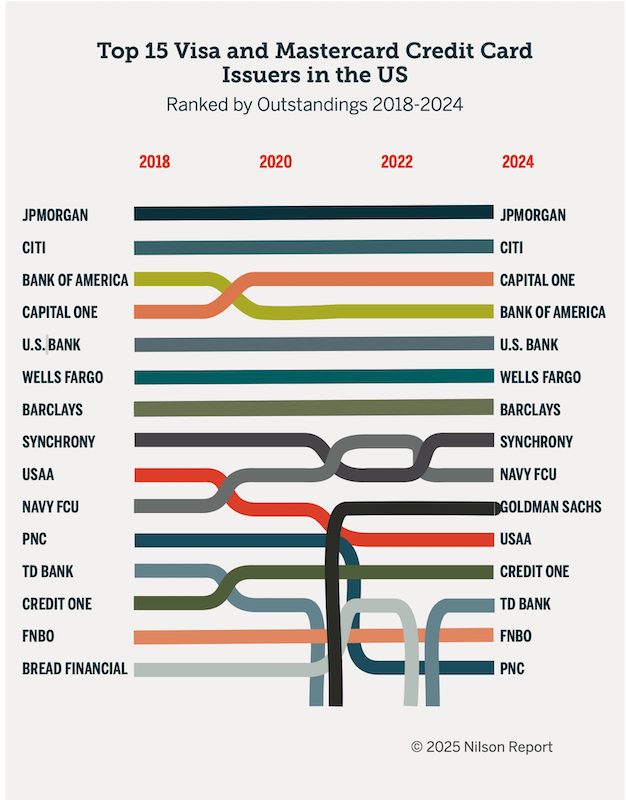

Finally this week, the Federal Reserve gave approval to the acquisition of Discover by Capital One. This deal has long been in the making, and it will be a long time until it closes. This is a truly remarkable deal with the number four and number six issuers joining forces. According to Nilson, in 2024, these two banks were responsible for $821.88 billion in purchase volume. Combined, they will be the third largest card issuer following JP Morgan Chase ($1.3 trillion) and American Express ($1.2 trillion).

It’s the end of an era for Discover, which was founded 40 years ago by Sears, Roebuck and Co. I still carry a Discover card (now known as the “it card,” literally). It was the first credit card I applied for in my own name, in front of the college bookstore just before classes started my freshman year. (A formerly common time to get your first card, now prohibited by regulation!)

I haven’t read the details of any agreements that Capital One made in the deal to ensure competition, but if I were Capital One, I would be excited to take on American Express. With a combined national brand and a 99% coverage merchant network in the U.S., Capital One is poised to create a three-party platform, much like American Express’s.

I expect the Discover brand for cards to be deprecated in favor of Capital One. I’m not sure what the right brand move on the network side is: Discover is both known and dismissed widely at the same time. As a fintech-focused person, I would love to see a new Capital One-owned Discover Network play a bigger role in payments innovation.

I don’t think Capital One will move all of its credit products off of Mastercard or Visa anytime soon. There are plenty of long-term agreements and incentives; plus a travel card on Discover Network to replace something like the Capital One Venture X Mastercard or Visa won’t work as well for international travel. However, moving Capital One’s debit card products to their own network could provide a boost in interchange earnings.

Me, Elsewhere

On the topic of rewards, I spoke with NerdWallet about credit card "coupon books." While this isn't quite the Entertainment Book of yore, these little discounts given throughout the month feel a lot like it. Read more about them here.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.