Will it Pay to Paze? - CardsFTW #118

Plus, BMO’s new card, two new secured cards, and a card made of jewelry?

Webinar on Credit Card Rewards with NYPAY

Next week, I will sit on a panel with Michelle Beyo from FINAVATOR, Nick Ewen from The Points Guy, Alex Preece from Tillo, and Nate Bacon from PNC Bank as we discuss the evolving landscape of credit card rewards and loyalty programs. Plus, you can learn whether Nick or I have more credit cards (I bet you can guess).

Join us on August 20th from 6:00 PM to 7:30 PM EDT.

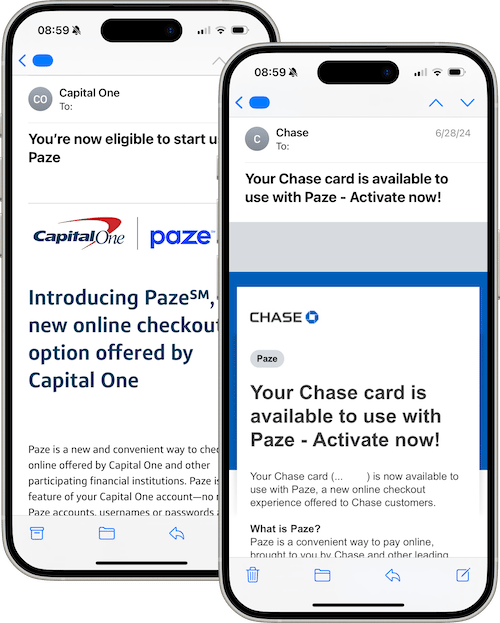

Big Banks Want You to Paze

The rollout of Paze is underway, and consumers from Chase, among others, are receiving emails promising "a new checkout experience!"

Ah yes, just what consumers have been asking for: complicated email messages with FAQs about a new checkout experience.

"What is Paze?" you might ask. Well, Paze is the new kid on the block in the online checkout world from Early Warning Solutions, which operates Zelle. If Zelle is short for Gazelle (you know, quick and nimble), what is Paze short for? Maybe Pheasant (or Pazant?) I get it; it's like "pays" but with a "z". For pizzazz. Clever.

Paze looks and feels like the very successful ShopPay, Stripe Link, Paypal’s FastLane, and Visa Secure Checkout (which is also known as Mastercard Click to Pay). Do we need another online checkout option? Probably not, but here we are.

So, what’s supposed to make Paze stand out? The big selling point is its direct bank integration. Instead of typing in your 16-digit card number, your bank can deliver your card credentials directly to the wallet. That is if your bank is on the Paze bus.

In contrast, other wallets require you to enter the whole wallet first; then, you can save them.

ShopPay is nice because so many stores use it. Once you enter your email or phone number, you are recognized automatically and then prompted for a one-time code. Then, boom, you can pay. You can use any branded card with Visa Checkout, now Click to Pay, but the login process often feels more onerous.

Is Paze really offering something new? I understand that saving a card number is nice, but you can do this on your browser or with tools like 1Password, Google Pay, or Apple Pay.

Frankly, I think there are too many options without meaningful features to differentiate Paze from the offerings already in the market or to pull users from the systems they are already used to (and to which they have already added their cards). It still may be easier simply to type in your sixteen-digit card numbers than to switch to Paze. Banks could choose to participate in a working system and deploy cards more easily (via a login vs. card number), but that probably wouldn't serve their self-serving strategic goals.

The truth is that the networks have tried to build these checkout systems multiple times, but mainstream acceptance has always been a struggle. As much as I’d like to be optimistic about Paze, I don’t have high hopes for It. But who knows? Maybe Paze will surprise us—or maybe it’ll just be another option in an already overcrowded field.

Goldman Socks

Just in case you missed it: We recently launched Goldman Socks: "I don't think they can sue me for using my last name." Show your love of CardsFTW–or, you know, money–with our premium socks. Save 10% with code "CardsFTW"

TD Steps Up Its Secured Card

TD Bank announced new rewards on its TD Cash Secured Credit Card last week. The card carries a low $29 annual fee and now offers a 3-2-1 earning style, just like its unsecured counterpart, the TD Cash Credit Card. Cardholders will earn 3% cashback on a category of their choice, 2% on their second category, and 1% cashback on all other eligible purchases. Customers will also be able to change their categories quarterly.

Wow. Most secured cards don't have rewards; they are pretty weak if they do. New secured card providers Pesto*, Aven, and Yendo offer new ways to secure your card (see CardsFTW #63), while other providers, like Chime, offer cards with dynamic limits based on a linked debit account. While the method of securing the TD Cash Secured card remains traditional, the rewards stand out.

BMO Launches a New Premium Mastercard

Canadian banks that came to the States are on a roll this week. BMO (pronounced "bee-mo" for anyone who missed the million commercials they purchased) announced the launch of its new BMO Premium Rewards Credit Card.

The new card earns 4 points per dollar on gas, electric vehicle charging, groceries, and dining ($2,000 quarterly limit), plus 2 points per dollar for hotels and airfare (again with a $2,000 quarterly limit) and 1 point per $1 spent on all other eligible purchases. In a slight twist, the card earns 10% anniversary points yearly, giving you a total bonus at the end of your year. The card has a $95 annual fee.

It's good for BMO to try to compete with the big cards and move up to a 4-2-1 card. The limits feel a bit low. (BofA's Customized Cash Rewards Card has no annual fee and is 3-2-1 with $2,500 limits, which is 25% more!).

SoFi is launching Two New Invite-Only Cards

SoFi is piloting two new invitation-only credit cards: the SoFi Everyday Cash Rewards Credit Card and the SoFi Essential Credit Card (hat tip to Danny Deal Guru). The SoFi Everyday Cash Rewards Credit Card is a 3-2-1 card earning 3% cashback on dining, 2% on grocery stores, and 1% on everything else. The second card is a credit builder card.

The SoFi Essential Credit Card is a credit builder card for SoFi members interested in improving their credit without the surprise fees.

Bourgeois Bohème–BoBo

One new interesting startup to mention this week is Bourgeois Bohème, also known as BoBo. I'm unsure of the name choice; I hear BoBo means dumb in some Spanish-speaking countries. Anyway, BoBo is a card for the ultra-high-net-worth and even says "Bourgeois" on it. Wow.

In a recent Forbes article, the company's founders noted that “popular features among BoBo's clientele include cross-border transactions for securing family vacations, fueling private boats, and acquiring real estate or luxury assets seamlessly in a single transaction.”

According to the company, "BoBo's ideal customers typically possess investable assets exceeding $30 million (UHNWI) or $1 million (HNWI) and have complex family and household expenses, as well as geographically dispersed assets." That's a bold choice.

We can’t talk about this card without addressing the opulent design. As soon as I saw this release, I thought, “This card better not be just metal”. Well, we’re in luck. Not only do they offer a wide range of wearable payment products (which I am assuming are not real) and cards with a circular EMV chip (which I also assume is not real), but they also may be the first “Jewelry Card”–made with solid gold and other precious stones. Does this card work in a reader? I have no idea, but you definitely don’t want to lose this card.

BoBo’s overt display of wealth can be seen as both a celebration and a critique of the conspicuous consumption that defines much of the luxury market. But there’s something undeniably tacky about BoBo’s approach. Flaunting wealth has always walked a fine line between admiration and derision, and BoBo seems to revel in straddling that line.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.