Credit Cards Are Hard - CardsFTW #184

Plus, New Membership Programs, Virtual Card Numbers, and More

Credit Cards Are Hard

One of my running jokes is that when I first talk to prospects for my fintech advisory practice at Totavi who want to start a credit card, I say, “I recommend you don’t.” It’s counterintuitive that I should discourage people from building credit cards when it's one of the payment products we specialize in helping companies to build. However, I want people to know what they are getting into.

Building a company is really hard. Building a credit card is really, really hard (even for a large corporation). Building both at the same time is exponentially harder. I should know: I started a credit card company in 2019 (Vertical Finance) that didn’t quite make it (although we did launch and sell the company as an acquihire to a larger, later-stage fintech platform). It was a painful process for me, and my second journey through starting a fintech company, which was also centered my second journey through starting a fintech company around a card (Wallaby was originally intended to be a card product, too).

Credit cards are one of the most complex personal financial products ever invented. They require complex processing systems, detailed compliance and oversight from a chartered financial institution, and capital. LOTS of capital.

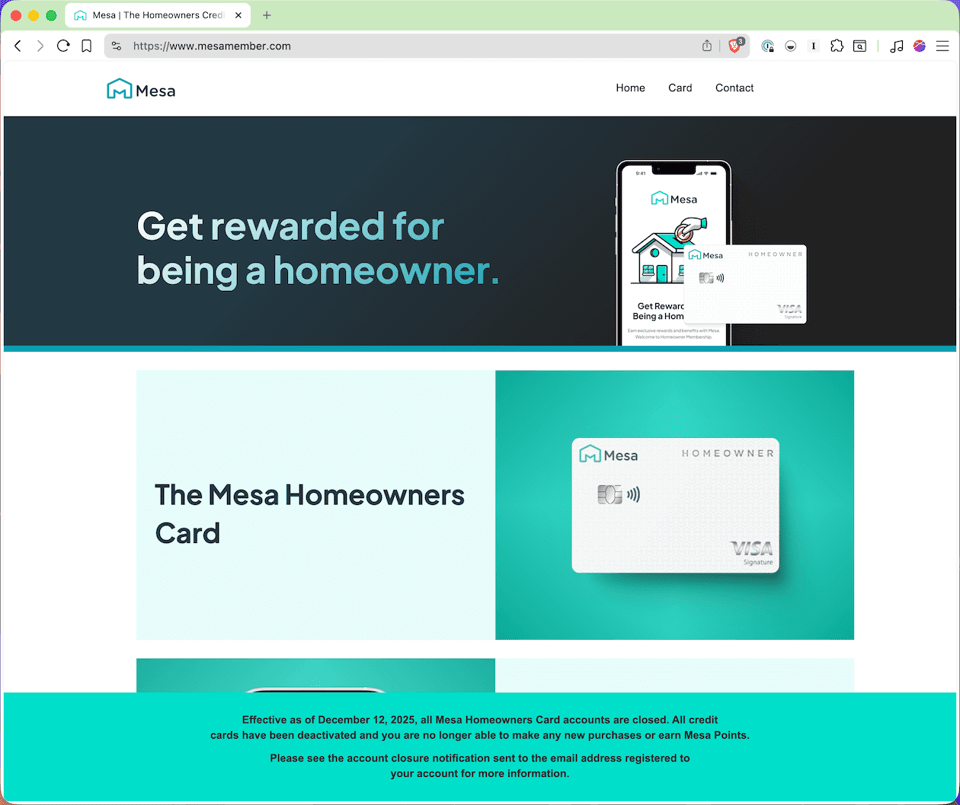

Last Friday, news hit the Internet that fintech start-up Mesa was closing all of its Mesa Homeowners Cards.

Effective as of December 12, 2025, all Mesa Homeowners Card accounts are closed. All credit cards have been deactivated and you are no longer able to make any new purchases or earn Mesa Points. Please see the account closure notification sent to the email address registered to your account for more information.

Mesa is not a client. I do not have any insider information. It is a small industry, so I have met the founders (and briefly worked with one of them in a prior role).

I hope this isn’t the end for Mesa and that something new is on the horizon. Over the past few months, it seemed like things were going well: there was good online discussion about folks acquiring the card, a funding announcement in August, and good news around mortgage and home-related cards. While some might argue that the competition of Bilt entering mortgage points and startup competitor Made Card would be a bad sign, I think that competition shows that an idea has multiple strong adherents who are taking bets and is actually a sign of good things to come.

I’m writing about Mesa not to pile on with the bad news, but because I think the news has caused waves through the startup credit card community. Is this a sign that venture investors will pull back? Is it a sign that consumer credit cards don’t work? No, I don’t think it is.

After all, Vertical Finance was sold in 2021, and look at all the great things that have happened since then with companies like Imprint, Cardless, Bilt, and others. Building in startups is a power-law business: ~50% of all startups should be bets that will fail, in order to take the swings that produce the outlier successes. As a VC (who invested in Wallaby) once said to me, “This idea is crazy and likely won’t work. But, if it does, it will be worth billions.” (Clearly, it didn’t end up being worth billions.)

I remain optimistic about fintech consumer credit cards. There was once an argument that a consumer neobank wouldn’t succeed, but companies like Chime, Current, and others have defied that belief. There will be more pain and more failed enterprises along the way. However, the right team, the right product, and the right timing will produce more winners in the consumer challenger credit card space. It’s hard, not impossible.

Department Stores Love Credit Cards

Speaking of when credit cards are successful, a recent article from the Financial Times highlights how co-brand credit cards can drive profits for retailers. According to the article, Macy’s revenue from credit cards accounts for less than 3% of sales but 62% of operating profit. Macy’s may be an extreme case, with Best Buy generating 26% of profit from credit cards, Victoria’s Secret 17%, and Target 10%.

Macy's situation may also be an example of Macy's not being good at their core business.

Merchant co-branded credit cards generate loyalty, collect data, increase basket sizes, and earn interest income. As consumers face challenges from affordability and inflation, cards that help individuals access the basics, from clothing to everyday essentials, are likely to perform well.

New Membership Programs from SoFi and Current

SoFi announced a new card product: The SoFi Smart Card, a Mastercard One Credential product that offers a single card for both debit and credit. The SoFi Smart Card requires users to be a SoFi Plus Member ($10 per month). The Smart Card includes 5% unlimited cashback at grocery stores, a 4.3% APY on savings balances for six months, and a dynamic credit limit based on the user’s linked SoFi checking and savings account balances.

Over at Current, they announced Current Max, a subscription that, similar to SoFi Plus, includes a variety of benefits. Current Max subscribers can earn up to 6% APY (on balances up to $6,000), 3x rewards points on grocery and restaurant purchases with the Current Build credit builder card product, and access to wellness benefits. Current Max is also $10 per month.

These two products appear to be aimed at very similar users, offering credit building, savings boosts, rewards, and additional benefits for $120 per year. Given the extensive discussion about Gen Z struggling to build credit, I’ll be closely watching the neobanking space to see further developments.

The Return of Discover Virtual Card Numbers

Let’s face it: I’m getting old. I’ve been messing around with credit card technology for about 25 years now (I started early). In the early 2000s, both MBNA (acquired by Bank of America) and Discover offered virtual card number tools that were powered by Macromedia (acquired by Adobe) Flash. You could create one-time use card numbers, recurring spend numbers, and limited numbers to use for e-commerce. At a time when many websites were quite insecure, and PCI standards did not yet exist, the primary goal here was security. Today, companies like Lithic, with their Privacy.com brand, have brands built entirely around virtual card number controls.

At some point, probably at least a decade ago, both banks deprecated this feature as Flash slowly left the web. I don’t think this is new, but a recent marketing email from Discover caught my eye highlighting the ability of cardholders using Discover and Google Chrome or Android to create a virtual card number when checking out with merchants.

I don’t use Google Pay much and I’m not too concerned about card number theft (just get a new card!), but I did think it was interesting to see this old messaging return.

Me, Elsewhere

I’ve been busy! Check out some of my latest appearances.

Fintech Layer Cake Podcast

I appeared for my third annual visit with Lithic’s Reggie Young to discuss credit cards

Thredd Webinar

I joined a panel of leaders from global issuing processor Thredd, loan management system LoanPro, and card program Arro to discuss “Shaping credit for a flexible, contextual world.”

The Fintercept

The Fintercept newsletter included me in a roundup of recaps and predictions for 2026.

Fintech NerdCon

I attended the first-ever Fintech NerdCon in Miami in November. They’ve put all of the panels and keynotes online. You can watch me moderate the panel “Building B2B Payment Rails That Scale,” with the founders of Forward, Moov, and Lithic.

Wade bought his hat at the Miami airport.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.