Credit Card Rates Are Too High - CardsFTW #126

Plus, managing subscriptions is getting to be a big business

Money2020

As Money2020 gets closer, we’ve noticed a slowdown in fintech news. It seems everyone is saving their biggest announcements for the event! We can’t wait to hear about the exciting updates, partnerships, and product launches that will be revealed. It’s always an amazing time to see what’s next in the industry, and we’re sure this year won’t disappoint.

Just like last year, our team will be attending, and we’d love to meet up. If you want to connect, fill out this quick form. We’re also organizing a directory of all the events happening around the conference, so be sure to check it out here. If you’re hosting something, you can add your event using this form.

The Credit Card Rates Are Too High

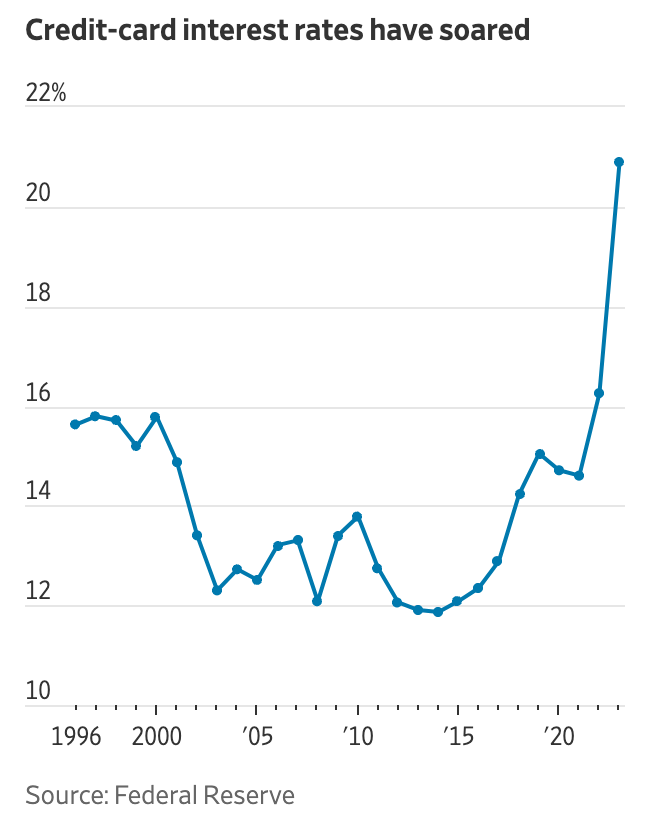

There was a time when most major credit card issuers wouldn’t charge more than 29.99%. You might see an APR higher than this on a subprime card, but certainly not from the larger issuers running mainstream programs. According to The Wall Street Journal, those days are over. Bread Financial and Synchrony, the nation’s largest issuers of retail co-brand credit cards, have removed these soft caps of 29.99%, just in case the CFPB’s proposed $8 late fee cap goes into place (or so they say).

We all know that credit card rates are variable and rise and fall with broader interest rates. However, the average card rate jumped more than the corresponding underlying 5% jump in the federal funds rate, moving from the mid-14.6 % range during the zero-rate pandemic era to more than 20.9% today (a 6.3% jump). A 1-2% variance might not seem like a lot, but on more than a trillion dollars in debt, it certainly adds up.

While mortgage rates are often much more competitive and closely tied to the underlying federal funds rate movement, credit card rates often rise like a rocket and sink like a feather, as seen in this chart:

While the Fed recently cut rates by 0.50%, credit card interest rates have only declined 0.13% to 20.65% as of 10/2/2024 from a recent high on 9/18/2024.

Don’t get me wrong, I know that a home, secured by real property assets, should have a much lower rate than an unsecured revolving credit card loan. However, the rates are just too high. Those eye-popping 34% rates are usurious (in states that are so quaint as to have such laws).

I am hoping, but not expecting, rates to come down a bit more, but I think card issuers will attempt to use this time period as a way to reset expectations on average rates.

Mastercard Acquires Minna Technologies

The other week, in CardsFTW #124, we talked about how networks are using tier-based benefits to stand out in a competitive market, especially around popular services like streaming. Mastercard has taken that strategy a step further by announcing its acquisition of Minna Technologies, a startup that specializes in subscription management. This is another example of how networks are continuing to pursue more value-add benefits evolving beyond transactions.

Minna’s platform lets users track, manage, and even cancel their subscriptions through banking apps, which ties directly into the broader trend we’ve been seeing. With so many consumers juggling multiple subscriptions, there is a growing need for tools that help streamline and optimize these recurring expenses. This acquisition positions Mastercard to offer more value to consumers and their banking partners by making financial management simpler and more effective.

It’s going to be interesting to see how this shapes the competition between networks. Mastercard is clearly betting on the idea that consumers will want more control over their subscriptions, and this could be a smart way to deepen its relationships with cardholders. As more of our spending shifts to recurring payments, subscription management might just become a key feature for networks trying to stand out. We’ll have to watch how others respond, but this could be the start of a larger trend in the space.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.