It’s the Little Things - CardsFTW #206

Plus, Premium Card Profitability, a US Consumer Debt Update, and Yendo’s Unsecured Card

See how Lithic delivers reliability

Citi Cancels the Custom Cash Card

In Big Bank Co-Brands - CardsFTW #30 (June 2021!) I covered the launch of the Citi Custom Cash Card. I wrote:

(The card) appears aimed at popular cards like the Chase Freedom and Discover it 5% rotating category cashback cards. […] The new Citi Custom Cash Card features a rewards rate of 5% each billing cycle in the single category where the user spends the most, up to a $500 limit (a $25 bonus). Unfortunately, there are limited eligible categories in the fine print, which I find very disappointing. So limited, I can list them here: restaurants, gas stations, grocery stores, select travel, select transit, select streaming services, drugstores, home improvement stores, fitness clubs, and live entertainment. Cardholders will also have to be wary of the phrase “select.” For example, “select travel” excludes campgrounds, “select transit” excludes bike rentals, and “select streaming” is a specified list that currently excludes things like Discovery+.

Well, the card lasted almost five full years. Citi announced on May 28, 2026, that they are no longer accepting applications for this card. Existing cardholders can continue to use the card.

As a user, I have always liked cards that allow me to select (or that automatically select) top rewards. As an issuer, these seem like sure-fire expensive rewards programs. If I know I can earn 5% in a category on a particular card, I will do my best to max that out. That’s very expensive for an issuer when the rest of the program doesn’t quite stand up to the competition. We’ll be watching to see what Citi brings up next.

Sponsored by Lithic

Most processors connect through middlemen. Lithic connects directly to the network.

High-growth fintechs don't have time for unreliable infrastructure. Lithic delivers 99.99% uptime, high-fidelity transaction data, and direct network connections. No filtered data, no downtime excuses.

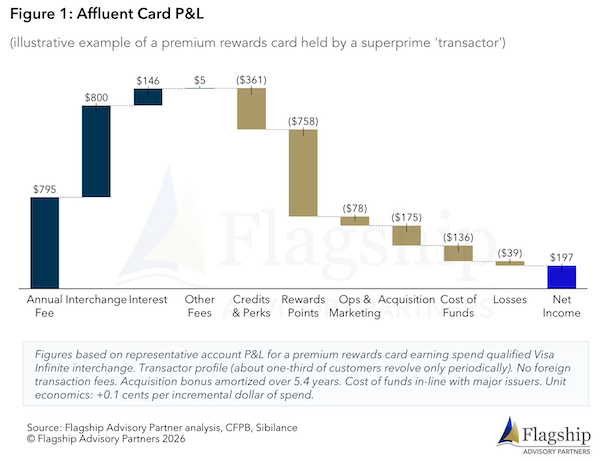

Premium Card Profitability

Speaking of the challenges of managing reward program profitability, my friend Ben Brown (and colleagues) at Flagship Advisory Partners wrote a great piece on The Illusion of Premium Card Profitability. I recommend everyone interested in building cards read it.

Filled with detail and charts, the article shows that you can make money on premium cards, but it is very hard. We have talked at length about why cards like the Robinhood Gold are designed with negative transactional margins (providing up to 3% cashback per dollar on income of closer to 2% per dollar): loyalty and cross-sells. As the paper puts it:

The Robinhood Gold Card is a great example: its 3% unlimited cashback might seem absurd, and we estimate Robinhood has earned no more than $140 per cardholder (mostly interest) before operating expenses over the last twelve months. But Robinhood’s 4M Gold subscribers pay a membership fee of $60 per year, keep 5x more assets under management, and over the last twelve months they have paid Robinhood $656M in margin interest.

What a deal (for Robinhood and their users).

It’s long been described that profitability is the sixth of six reasons to build a co-brand card. Better reasons include:

- increased customer spending

- deepened customer loyalty

- improved customer data

- enhanced brand exposure; and

- competitive advantage

That continues to be true.

Yendo Launches an Unsecured Card

Yendo, which originated the automobile-backed credit card (see Credit Builder Cards - CardsFTW #63), has announced an expansion into unsecured cards for the first time. I’ve been asleep at the wheel, because I also learned that Yendo has a home equity card (which launched six months ago!) and, according to the release, represents 20% of volume.

Like I keep saying, this is the year of home equity-linked cards. The Yendo Unsecured Card launches with unlimited 1.5% cash back on all purchases. Yendo cardholders also have the option to add their asset to their credit card, which can result in credit limits of 500% or more at significantly lower rates.

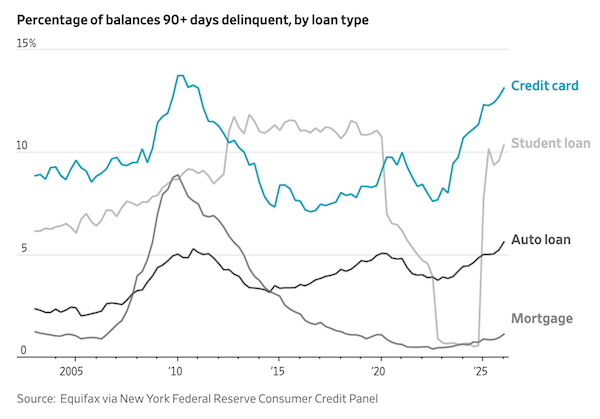

Consumer Debt Continues to Grow

In what feels like a quarterly event, The Wall Street Journal reports that “Americans Are Falling Behind on Their $1.25 Trillion Credit-Card Bill”.

I sense some correlations from this data:

Could it be, in part, that Americans’ tremendous student loan debt is driving folks to the edge? I think so. We know inflation continues to run above the Fed’s target, exacerbated by higher increases in “must-have” categories like fuel and healthcare.

Look, this was a very tough article to read, with reminders of how deep folks can fall into debt. It’s easy for me to sit here and write that rewards are great for people who can pay their bills, but extenuating circumstances can drive people into deep (and expensive) debt.

Some of it is external shocks, but some of it is that people want to spend money. After reading about a man’s journey through credit card debt, it was sad to read:

They have a $1,900 mortgage, and still keep two cards—one for emergencies and one for discretionary expenses, which they try to limit. At one point, the balance reached $11,000, but they have whittled it down to $6,000, Daniel-Hoste said.

Why is there still a card for discretionary expenses? That’s a rough one.

It’s the Small Things: Separate Card Numbers

Last week, in Are Cards and Accounts the Same Thing? - CardsFTW #205, I wrote about the challenging concept of how banks and ledgers think about cards and accounts versus how users consider them.

One feature that American Express has long offered, which I love, is separate card numbers that access a single credit card account. While virtual cards and separate cards have long existed in business cards, they have been rare until the past few years for consumer products. Amex has long offered them so that, if a couple has an Amex account, you can see which person made which purchases on which card. This is helpful for tracking, checking for fraud, and limiting the blast radius of a lost or stolen card number.

While many fintech card processing platforms support this, there has continued to be a limited number of traditional issuers who that do.

This week, I was very pleased to receive new cards from Chase that demonstrated the arrival of this feature! The primary cardholder number didn’t change, but the authorized cardholder was issued a new number to differentiate between users.

It’s a little thing to users. It was likely a hugely complex project for Chase.

I love little product improvements that aren’t obvious. Did a lot of users request this? I doubt it. Most likely, few people knew it was an option (given that many traditional issuers don’t provide it). Someone had to build a business case (I’m sure one could be made on dispute reduction and card issuance costs). In an era when it feels like every card feature is reward-focused, this stood out to me as a nice additional feature that enhances usability for all cardholders.

Good work, Chase.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.