The Core Processor Market Analysis - CardsFTW #163

Plus, Wawa Gets a Card

2025 Core Processor Market Analysis

I am proud to announce the publishing of the latest in Totavi’s growing research analysis catalog: the 2025 Core Processor Market Analysis, a comprehensive and data-driven examination of the fast-evolving core processor landscape. The report provides a granular look at the functions, trade-offs, and market dynamics behind the processors that power card programs in the U.S., providing an extensive comparison of feature sets such as authorization logic, card type support, settlement methods, modular stack design, tokenization, and real-time ledger integration.

Like our other reports you can purchase this today for $500 as a stand-alone product or subscribe to our market research subscription for $795 per year and get this (and all of our previous reports).

So, What’s in It?

The report includes an extensive side-by-side comparison of processor capabilities: card manufacturing, mobile wallet integration, real-time funding support, international wire compatibility, dispute tooling, KYC flexibility, and more. Readers can quickly compare processor tradeoffs across 40+ discrete criteria.

We evaluated 10 core processors: CoreCard, Episode Six, Galileo, Highnote, i2c, Lithic, Marqeta, Qolo, Stripe, and Zeta. The analysis spans technical architectures, customer segmentation, product capabilities, and go-to-market strategy.

Key Findings and Market Predictions:

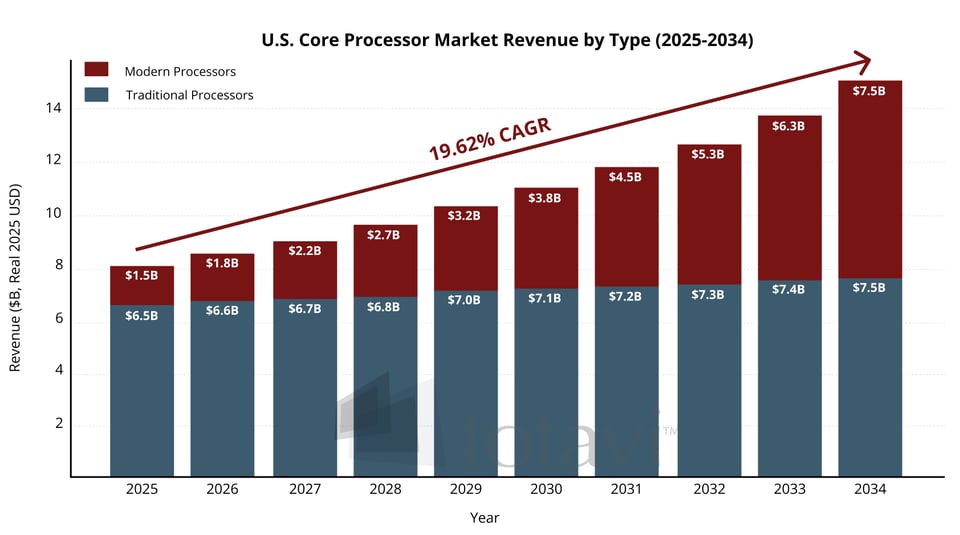

- $15 Billion by 2034: Totavi projects that the U.S. issuer processor market will grow from approximately $8 billion in 2025 to $15 billion by 2034 in real (inflation-adjusted) terms. This represents a 6.5% compound annual growth rate (CAGR) over the next decade.

- Modern Processors to Gain Ground: While traditional providers like Fiserv, FIS, and Jack Henry will grow slowly—from $6.5 billion to $7.5 billion—modern processors including Stripe, Marqeta, and Lithic are projected to grow fivefold from $1.5 billion to $7.5 billion. By 2034, modern and legacy processors are expected to split the market evenly.

- Market Expansion: Growth is driven by increasing card transaction volume, broader adoption of embedded finance, and rising demand for modern developer-first platforms. Non-bank issuers, such as marketplaces, SaaS platforms, and gig economy apps are becoming key contributors to this expansion.

- Segment Evolution: Credit remains the highest-margin segment, generating nearly 50% of revenue despite a smaller transaction share. Debit is growing in both consumer and B2B use cases, while prepaid remains a niche segment tied to government programs and specialized applications.

- Strategic Inflection Points: The report includes operational guidance for companies, including when to work directly with a processor, when to migrate off a program manager, and how to assess build-vs-buy decisions for in-house processing.

Wawa’s New Card

No, this isn’t a sad trombone. For those of you not in their home territory on the U.S. East Coast, Wawa is a convenience store chain headquartered in its namesake, Wawa, Pennsylvania. With more than 1,000 stores, it is the seventh-largest convenience store chain in the U.S. (according to the NACS).

Wawa joined the convenience and fuel-store card list last week with the new Wawa Mastercard, issued by First National Bank of Omaha. Like many gas cards, the Wawa card earns both bonus points at its stores (3x per dollar, inside the store only) and a direct gas discount (5 cents per gallon) on all purchases.

Other convenience store brands with cards include Sheetz Visa (also FNBO), and petroleum brands like Shell (Citibank), BP (Synchrony), ExxonMobile (Citibank), and Chevron/Texaco (Synchrony). My review pegs the fuel savings at 3-7 cents back, putting Wawa in the middle. The internet tells me that Sheetz and Wawa don't really overlap territory in Pennsylvania, so now folks on the East Coast have options for earning rewards points on gas station food. (This is all foreign to me, as I have lived in the Western US my entire life.)

Don’t forget you can also buy gas from places like Costco and Kroger and they also offer their own cards. While those cards don't feature a cool goose, Costco does have a following rivaling that of Wawa and Sheetz.

Me, Elsewhere

I had a good media week! Check me out in:

- Fast Company, talking about Bilt in “Bilt to last? Inside the points-obsessed startup that rewards you for paying rent”; and

- U.S. News & World Report, talking about the changes to the Chase Sapphire Reserve in “Is the Chase Sapphire Reserve Worth its $795 Annual Fee?”

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.