Cards We Don’t Always Talk About - CardsFTW #211

Plus, global co-brand news updates and pay with points

How Do You Maximize Points?

If you’re reading this, you probably know that I have expended a lot of effort into points maximization. You probably do it yourself!

I’ve noticed a big increase in points optimization apps and tools again. I’m writing on the topic and would appreciate it if you could share your thoughts in my super-quick survey (max 6 questions). Thanks!

Disbursement Cards: An Unsung Hero of Money Movement

Totavi just published our 2026 Disbursements Card Market Analysis, and it's some of the best work my team has put out this year. The report covers four segments (insurance claims, disaster and emergency relief, gig payout, and government benefits) and lays out the structural forces pushing each one toward card-based, real-time payouts. If you've been watching push-to-card adoption in claims settlement or the infrastructure gaps in EBT, this is a useful operational view of where things stand and where they're headed.

A few data points from the report I want to share. Government agencies pushed $183.2 billion through prepaid cards across roughly 1,200 programs in 2024, and SNAP alone has seen over $360 million in benefit replacements from fraud between fiscal years 2023 and 2025, which tells you how much modernization work is still ahead. On the gig side, we tracked how platforms like Uber and DoorDash have turned payout cards into a way to build deeper financial relationships with their workforces, a trend I expect to accelerate as the gig economy grows toward a projected 90 million workers by 2028.

We also dug into where the market is heading over the next decade, including a shift from merchant category code restrictions to item-level spending controls and the possibility of gig payout products extending onto stablecoin rails for international workers. It's now available to Totavi Pro subscribers, along with the rest of our research library, which covers program managers, issuer processors, and debit platforms. If you want the full breakdown, you can subscribe at totavi.com/research.

A Global Co-Brand News Update

I normally focus mostly on the U.S. market (just because I’m here and there is too much news to keep track of!), but this week stories from the U.S. and globally caught my eye.

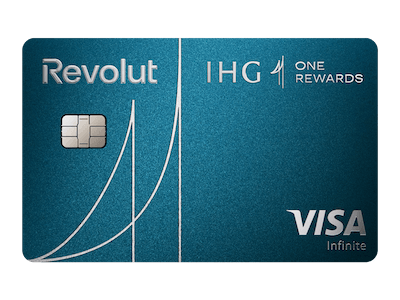

IHG + Revolut Launch Another Rewards Debit Card

There has been a rush of co-branded debit cards lately. Really, so, so, so many! Add two more to the list: IHG One Rewards x Revolut Elite Debit Card and the IHG One Rewards x Revolut Essential Debit Card.

First, I didn’t realize Visa Infinite for debit existed. You learn something new every day.

The top-tier card is £18 per month. You can earn 30,000 IHG One Rewards bonus points with £3,000 in spend in the first 3 months from account opening. With IHG One points worth about 0.45 pence, that’s about £135 in value, which seems pretty good. The Essential card earns just 10,000 IHG points with £1,000 in spend, but has no monthly fee.

Elite cardholders will automatically earn Platinum status and 6x points per pound at IHG hotels internationally (3x in the UK and Europe). There are a ton of spend-based rewards and included Revolut benefits.

Essential cardholders earn automatic Silver status and an additional 1 point per pound at IHG.

Given the interchange challenges in the UK and the general preference for debit cards there, the IHG entry is a strong one, joining Hilton in the UK offering.

What stands out for me is that Revolut is the issuer here. A flag-bearer of the global neobank era, we see Revolut joining traditional bank issuers in the co-brand world. I expect more of this to come.

British Banks and an American Airline

Back on this side of the pond, British issuer Barclays’ US unit announced a long-term extension of its credit card program with Frontier Airlines (an American airline, not the American Airlines).

For the record, I refuse to write “Frontier” in all caps for this card.

There isn’t much beyond the announcement, but an extension of the deal could portend some updates to the card. I, for one, recommend the card not be just green.

{kind=link}

Yep, it’s just green. I’m available for design consulting.

Look, I don’t fly Frontier. I must be too fancy, but the card is a great pull if you’re a Frontier flyer. You get:

- Two free checked bags

- 1 elite status point per dollar

- Gold Status (gives you an upgrade)

A $100 flight voucher when you spend $2,500 per year

CardsWTF: AI Intelligent Computing Card

Meanwhile, over in China, a new AI Intelligent Computing debit card is launching on the China UnionPay network with Ping An Bank and Tencent Cloud. According to a translated article, the card is designed for people who just love talking to AI.

Rewards from this card earn cardholders access to tokens!

I’m always interested in something beyond the traditional points and miles. This was not on my prediction list, though!

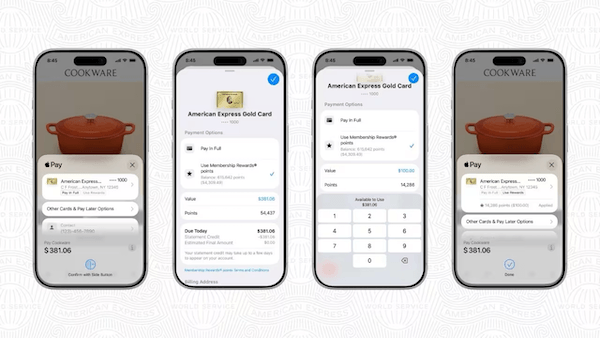

Pay with Points

American Express and Apple announced the availability of pay with points for American Express Membership Rewards points inside the Apple Pay wallet.

Pay with points is a convenient way for users to get value from those hard-earned points. It’s usually a mediocre rewards value, though. When using your Amex points via Apple Pay, they will be worth 0.7 cents per point (same as existing pay with points partner, Amazon.com). This value is more than the worst possible redemption (statement credits at 0.6 cents), but far off maximum values which can exceed two cents per point with transfers and travel redemption.

Pay with points isn’t very common. The major networks have worked to implement some form of it in point-of-sale systems and with Apple before. (Discover has had this capability, but it is going away due to the Capital One merger.) Many large issuers have an integration with Amazon.com. I don’t expect many merchants or merchant platforms to do these integrations, but via a mobile wallet, it could be quite easy.

If a product were ONLY available in points (we did this at Grand Reserve), I think that could be interesting, but I don’t think paying with points does much for people. You could just get a statement credit! Anywhere! Anytime!

Plus, if you are a points maximizer, even a redemption at par (say 1 cent for a 1 cent point) is a bad deal: You’re forgoing the earning of more points. For example, I have the Amazon private label store card from Synchrony. I earn 5% cashback at Amazon. I could redeem those points at Amazon in real time, or, as I do, earn 5% on all purchases and then redeem the points against my statement. If I redeemed them in real time, I would pay full price on that item.

All this reminds me: in case you read this far and are nodding along like, “yes, this is how to maximize points,” please fill out the quick tool survey!

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.