Fintech Breaks Into Big Retail - CardsFTW #116

Plus, Credit Cards are Causing Fights, White Gold, and more.

Socks!

I am very excited to announce a project I’ve been working on since last fall: Goldman Socks. Tagline: “I don’t think they can sue me for using my last name.”

I love swag, and I love socks. I especially love swag socks. Today, we are launching Goldman Socks because why not? We have three great designs to share with you for our first print run, including a CardsFTW sock. Use code “jesse” for 10% off. Paid subscribers, check the bottom of the page for your 25% code.

Imprint Launches New Brooks Brothers Card

Fintech card program management platform Imprint announced the launch of its new Brooks Brothers World Mastercard® issued by First Electronic Bank. This is a noteworthy program announcement because it marks a couple of firsts. The new card is the first large existing retail co-brand portfolio to launch on a fintech platform instead of a traditional bank issuer. It is also the first time a fintech has done a significant conversion, bringing an existing program over.

Imprint says the conversion was completed in six months, substantially faster than most portfolio conversions. The card is a good offering for a retail co-brand, featuring 6 points per dollar at Brooks Brothers stores, 4 points at restaurants, groceries, and gas stations, and 1 point everywhere else. The signup bonus, as expected with a no-fee retail card, could be more exciting, offering 20% off your first online Brooks Brothers purchase and a $40 bonus on your first purchase at another retailer.

Points are redeemable in 1,000-point increments at a $0.01 value (e.g., 1,000 points get you $10 in rewards). The card includes free return shipping, a $20 annual birthday reward, a $20 anniversary reward, and all the usual World Mastercard benefits.

In private conversations over the past year, I have advised retailers to consider fintech issuers. Many retail brands are unsatisfied with their deals with traditional co-brand issuers like Synchrony, Bread, or Citi Retail. However, they often need to be made aware of the opportunities with fintech issuers or believe them to be very hard to work with due to a perception of a higher level of technical integration.

While some fintech issuers have an API-heavy focus, which creates flexibility, others, like Imprint, Cardless,* and Brim, provide a more turn-key approach, enabling retailers to have a closer like-to-like comparison to traditional providers. Traditional bank issuers continue to have an advantage in terms of the cost of capital for lending, but they often need faster and more appealing processes and user integrations.

With this win, other retailers who are in the process of looking at new issuers will take a second look. (If this is you, give me a call.) We’re just in the early innings of fintech program management, but now Imprint has a big run on the board.

Fighting Over Points

Last week, Business Insider published a story about how Credit-card rewards are tearing friends apart. Aside from the weird grammar of “credit-card rewards,” they have a valid point. When I first got into the points game in 2004, as a traveling consultant, we felt that only nerdy business traveler types were focused on this.

Over the past decade, the awareness of the benefits and methods for earning credit card points has expanded dramatically. Thanks to sites like NerdWallet and The Points Guy, millions of everyday consumers have leveled up their knowledge of credit card points. Much like last week’s discussion on what your card says about you, knowing the best way to earn and redeem points has become a status symbol, not to mention a way to save money or rack up points.

There is a significant risk to being the one who throws down their Platinum card at dinner–your friends might forget to pay you back. Plus, if one friend throws down their Chase Sapphire Reserve and another their Citi ThankYou Preferred card, you might have a fight on your hands. That’s not savvy or cultured, folks.

Points are great, but let’s be cool: the person who arranges or hosts can offer to pay, but don’t fight people over it (also, don’t ask your server to split it ten ways). I, for one, am a fan of the round-robin method. One person pays each time, and we rotate. That way, you can enjoy the feeling of treating folks (and being treated) without the drama.

Amex Launches an Enhanced White Gold Card

American Express has been crushing it lately with card designs. I am a big fan of the Platinum Art series and the recent Delta plane card. As part of a broader refresh of the American Express Gold card, American Express has added a white gold variant (limited time only!) to its existing Gold and Rose Gold lineup. If I recall correctly, Rose Gold was originally a limited edition, so perhaps White Gold will stay if it is popular enough.

The refresh of the Gold card includes a substantial increase in the annual fee to $325 from $250 (a 30% markup). In addition, the 4x point earning on dining has been capped at $50,000 per year (sounds reasonable, unless, of course, you are paying for all your meals with friends and having them Venmo you back).

Some fun new benefits include $100 in Resy statement credits and a $7 monthly Dunkin’ Donuts statement credit. I think that gets you one coffee and donut power month.

I have upgraded and downgraded once or twice between Platinum and Gold, most recently downgrading at the start of the pandemic and upgrading earlier this year due to a huge bonus offer. One part of the AMEX strategy I don’t understand is why Platinum isn’t simply a better card than Gold. Gold earns 4 points at dining and supermarkets, 3 points on airline travel, 2 points on prepaid hotels booked through Amex, and 1 point everywhere else.

Meanwhile, the Platinum card has a ton of statement credits, 5x on flights and prepaid hotels, but only 1x everywhere else. Where is that 4x on dining or supermarkets? Those accelerated dining and supermarket earnings are available on other credit cards I carry, so my spending goes on them instead of the Platinum card. Combining these categories on one card would be a sure-fire winner and reduce the confusion in choosing between the two products.

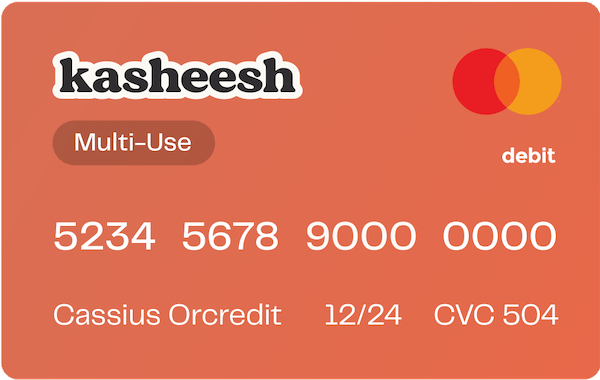

A New Way to Split Pay

Early-stage fintech startup Kasheesh* announced a huge new feature to its split pay product, providing users with a multi-use Kasheesh card (up from just a single use before)! We’ve talked about Kasheesh before, but as a refresher, Kasheesh provides consumers with a way to split any payment onto more than one card in a single transaction.

Users can add any credit, debit, or prepaid card to their Kasheesh account and choose how to split each payment or let the Kasheesh algorithm take over. For many consumers, larger purchases (such as rent, travel, or things like appliances or car repairs) may require using a mixture of funds from their checking account and one or more credit cards. With Kasheesh, users can intelligently manage how that is split up without asking (or depending on) the merchant to accept a split tender.

In the prior iteration of Kasheesh, users created a one-off card for each purchase, which allowed fine control but could be cumbersome. The new Kasheesh multi-use product creates a single card that can be reused online and in the real world via mobile wallets to split any charge. Kasheesh brings the Visa Flexible credential (see below) to any user and issuer today.

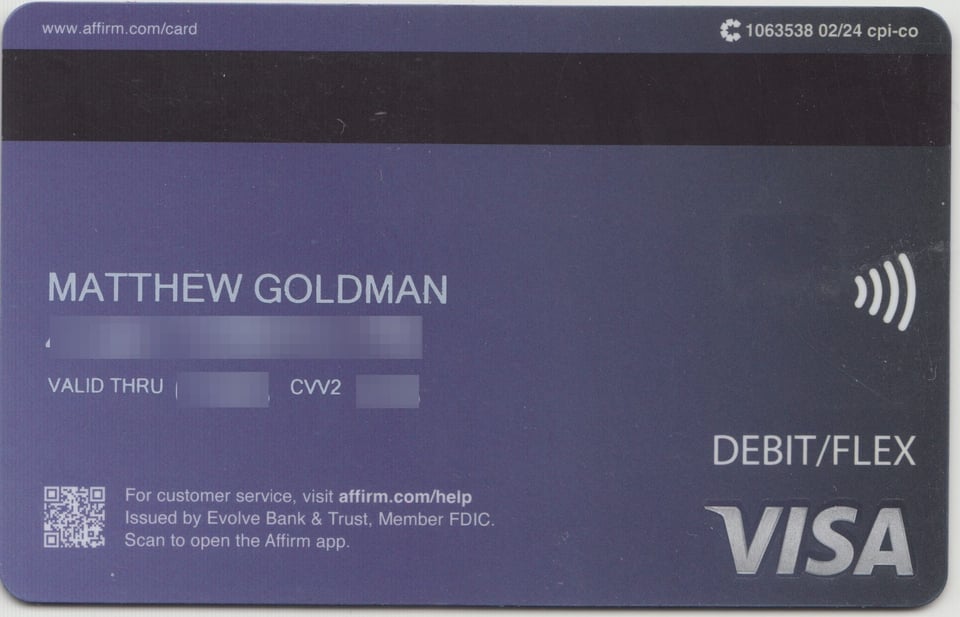

Flexible Credentials Launch

A few weeks back, I covered Visa’s announcement of the Visa Flexible credential, which enables a single issuer to create a combination of debit, credit, rewards, or BNPL products. Last week, Marqeta announced it was the first processor certified to enable this payment type with Affirm. Maybe I got the news early, but I already have an Affirm card with the Visa Flex identifier (received a few weeks ago).

The Visa implementation further solidifies what personal finance folks and the team at Kasheesh (see above) already know: people want flexible ways to pay. Visa Flex is clever, and I hope to see more issuers implement it.

CardsFTW

CardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more.

Interested in reaching our audience? You can sponsor CardsFTW.

*Indicates a company with which Totavi has a financial relationship.